An update to customers, stakeholders, and shareholders on our mission to unleash the potential in every team.

As we head into a new year, still waist-deep in a global pandemic, our hearts go out to our customers, team members, community stakeholders, and shareholders as they keep pressing onward. The strength and tenacity of the Atlassian community inspire us every day. 💪

Despite the pandemic, our journey as a cloud-first company is off to a good start in fiscal 2021. We launched Jira Service Management for IT service management (ITSM) teams, made significant progress on enterprise capabilities in the cloud, and announced a three-year migration path to the cloud for on-premises customers. These are important milestones against two long-standing goals: bringing a world-class cloud experience to customers of all sizes, and delivering continuous innovation that streamlines their most important workflows.

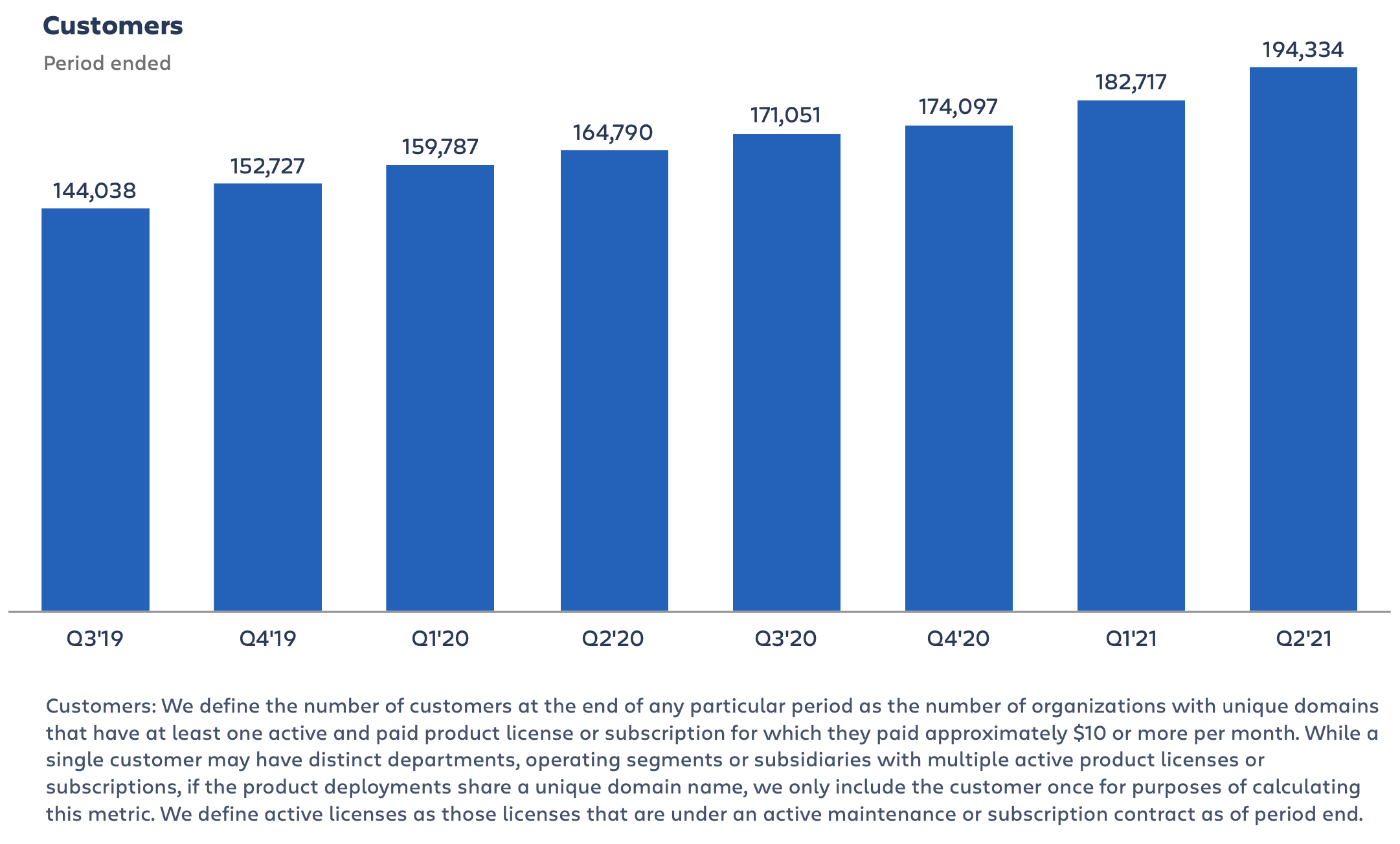

Our business results in Q2 reflect that steady pace of improvement. We generated $501 million in revenue in Q2, an increase of 23% year-over-year, and also achieved year-over-year subscription revenue growth of 36%. During the quarter, we added 11,617 net-new customers of all sizes, bringing our total count to 194,334. We’re proud of these results, yet also acknowledge that we’re still early in a multi-year cloud migration journey that will impact short-term revenue growth. Please see the financial section for more detailed commentary.

As we move forward, we’re excited to power our customers’ success in the cloud whether they started there or just arrived. Take global digital transformation partner ThoughtWorks, for instance. When they went all-in on remote last year, ThoughtWorks standardized on Trello Enterprise to keep their global team of 8,000+ connected as they scale.

Internally, our team continues to adapt and persevere. We’re full steam ahead on hiring and welcomed 467 new Atlassians globally in Q2, mostly in R&D roles. Through practices updated for a remote-first world, we’re delivering innovative work that delights our customers, meeting our most important goals, and maintaining the connections that bring us together not just as colleagues, but as people. ❤️

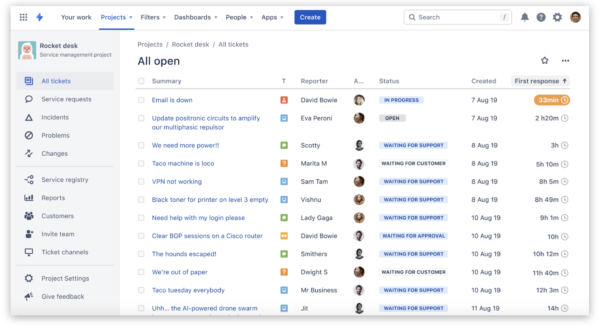

Jira Service Management rocks the house 🎸🤘🏾

The line between ITSM and software development blurs a little more each day as these mission-critical technical disciplines converge. Thanks to our strong relationship with both developers and IT professionals, Atlassian is uniquely positioned to deliver a unified cloud-based collaboration platform that brings these teams together. Our competitors simply can’t match this.

Jira Service Management unleashes technical teams’ potential with a holistic approach to ITSM tooling. Jira Service Management integrates several capabilities into one solution: service desk, incident management, real-time-communications, and configuration and asset management. As with so many Atlassian products, Jira Service Management is the culmination of home-grown and acquired teams joining forces to innovate for customers. With solutions like Jira Service Management offered at accessible prices, Atlassian is helping companies across the Fortune 500,000 transform their ITSM infrastructure and practices.

As we mentioned at our Investor Day in November, serving IT teams more than doubles our addressable opportunity: from 45 million software team members to a total of 100 million technical workers including IT teams. And it’s all made possible by the multi-year investment in our cloud platform, which has unlocked our ability to respond quickly to customers’ needs with new products and integrations.

For proof, look no further than global facilities and workplace services provider ISS Group. They streamlined their change management process by standardizing on Jira Service Management, making it their single source of truth for the 80,000 requests their IT team fields each year. “Atlassian fuels process improvements so it’s easy to mature the process and improve the way ISS is working,” says Marie Bjørke, Head of IT Service Management.

Atlassian fuels process improvements so it’s easy to mature the process and improve the way ISS is working.

– Marie Bjørke, Head of IT Service Management at ISS

All signs point to cloud ⛅️

Customer cloud migrations are progressing in line with our expected timeline, and our cloud platform continues to get better every day. On the enterprise front, Cloud Enterprise for Jira Software, Confluence, and Jira Service Management is now available, with higher initial demand than expected. Cloud Enterprise unlocks a host of benefits for our largest customers:

- Unlimited instances and seamless scaling

- A 99.95% uptime guarantee and premium support services

- Enterprise-grade data management, such as data residency

- Streamlined user management

But you don’t have to be an enterprise to benefit from the power and simplicity of Atlassian’s cloud. “We were behind on updating to the latest server versions,” recalls Marcus Hecht, a member of the IT team at ClearlyRated, a 30-employee B2B business directory. “We realized that we could migrate to Atlassian cloud and not have any downtime. We also coveted a couple of integrations that were only available for cloud. It was a no-brainer.”

Making the jump to cloud was a no-brainer.

– Marcus Hecht, IT engineer at ClearlyRated

95% of new customers choose cloud because of all the work we’ve put in to build a scalable cloud-native platform. Our updated editor is a great example of how our cloud platform allows us to deliver a consistent user experience across products. Customers told us they wanted a simpler, faster editor. So we rebuilt it from scratch with portability in mind. After launching the new editor inside Confluence in early FY20, we introduced it in Jira Software, Jira Service Desk, Statuspage, and Bitbucket in short order. More than a million people now use this editor every day.

And there’s more to come. Our cloud roadmap includes features for customers of all sizes that can be implemented across multiple products. This “build once, run anywhere” approach accelerates our development cycle and lies at the heart of our competitive advantage.

Building for the long-term through continuous innovation 💡

Teams may be physically separated, but Atlassian remains committed to bringing them together in the virtual world through products that take the “work” out of cross-functional teamwork. Teams at Canva, an online design platform and long-time customer, recently told us what a difference Atlassian products make. According to one infrastructure engineer, “Work becomes a lot more visible when it’s all in one place. It makes collaboration a whole lot easier and facilitates transparency.” We couldn’t agree more.

As we venture into a new calendar year, our focus remains squarely on building a world-class cloud experience for customers of all sizes. With 1000+ daily deployments that add up to massive customer value over time, our teams continue to deliver a steady drumbeat of improvements and innovations. Right now, our R&D teams are making our cloud products more performant and easier to use. They’re also continuing to enhance migration tooling for Jira Software, Confluence, Bitbucket, and Jira Service Management to make switching to cloud even easier. All of this work strengthens our position within our total addressable markets and allows any team at any company to manage mission-critical work.

Similar to the approach we take with our products, we strive for continuous improvement on the sustainability front. As we detailed in our FY20 Sustainability Report, we achieved our goal of operating on 100% renewable energy five years ahead of schedule, and we’ve committed to achieving net-zero emissions by 2050 in line with the Paris Agreement. We also continue to improve diversity across the company in order to become a more innovative, representative, and equitable organization.

Customers like ThoughtWorks, ISS Group, ClearlyRated, Canva, and thousands of others relied on Atlassian products to help them through an exceptionally challenging year. And for that, we are deeply grateful. It’s our honor and privilege to lock arms with current and future customers as we move through the next year and toward a more familiar version of “normal.”

Here’s to making consistent progress on our journey, and to unleashing the potential of every team.

– Scott and Mike

The Bottom Line

- The Q2 launch of Jira Service Management (JSM) represents a holistic solution for teams in IT service management (ITSM). By serving IT teams, we more than double our addressable opportunity in the technical teams market from 45 million to 100 million users.

- We’re focused on continuous improvement in cloud products for small business and enterprise customers alike. Our cloud platform allows us to develop features, like our editor, in one product and leverage them across many others.

- Continuous innovation guides our approach to customer value as well as sustainability and social impact. Our FY20 Sustainability Report highlights achieving 100% operations fueled by renewable energy, with more improvements in the works.

Customer highlights

Having the right tools matter, especially in this era of remote work. Customers tell us they rely on Atlassian to power their most important work like R&D, product launches, information security, and HR operations. Our products remove barriers, streamline mission-critical workflows, and foster human connections across the organization in a way that our competitors’ products don’t.

That’s why we’re winning with teams at over 194,000 organizations – an increase of 11,617 net new customers in Q2. Atlassian’s strong customer acquisition game reflects consistent progress at the top of the funnel as well as steady improvement in our customers’ cloud experience. And while this metric can see variability from quarter to quarter, what’s most important is that we continue taking steps to help the entire Fortune 500,000 unlock their teams’ potential.

We’re proud to say that this growth is powered by the most efficient go-to-market (GTM) model in the industry, and we’re always experimenting with ways to make it more effective. While our products themselves do the heavy lifting on customer acquisition, we believe part of our job is to make teams more effective by sharing best practices around teamwork and leadership. Making our products and content available for free with no strings attached is a critical part of our customer value proposition.

Top-of-funnel content isn’t just a marketing tactic, it’s an investment. Unlike ads or one-off sponsorships (which we do as well), an article or video pays dividends for years as it engages users at consumer scale through social media and SEO. This is a key factor in driving our word-of-mouth flywheel and keeping our GTM expenditures at approximately 15% of revenue.

For example, our award-winning blog, Work Life accounted for 1.7 million first-time visits to an Atlassian web property in 2020 – a huge win for brand awareness that proves the power of this approach. Another recent win is our five-star rated podcast Teamistry, listened to by small business and enterprise users alike. These examples and more keep customers coming back and make a positive first impression on people who find their way to us through SEO.

Farther down the sales funnel, we’re delivering virtual events that engage a far larger audience than would be possible in person. In 2020, between Summit (now branded as “Team”), Team Tour, and our Atlassian Community events, we connected with well over 10,000 customer organizations and over 35,000 end-users. Now we’re looking ahead to Team 2021 coming April 28th & 29th, which will focus on engaging teams at consumer scale, as well as our beloved hardcore product geeks. We hope to “see” you there!

With effective and efficient top-of-funnel tactics like free content and free trials – not to mention events that turn consumers into fans – we are marching steadily towards serving the Fortune 500,000.

– Cameron

The Bottom Line

- Net new customers grew by 11,617 to 194,334 in Q2, driven by cloud products and an improved cloud customer experience.

- High-quality consumer-scale content and events reach millions of users, and support our efficient GTM and frictionless customer acquisition flywheel. Join us in April and see how we engage customers at Team 2021.

Financial highlights

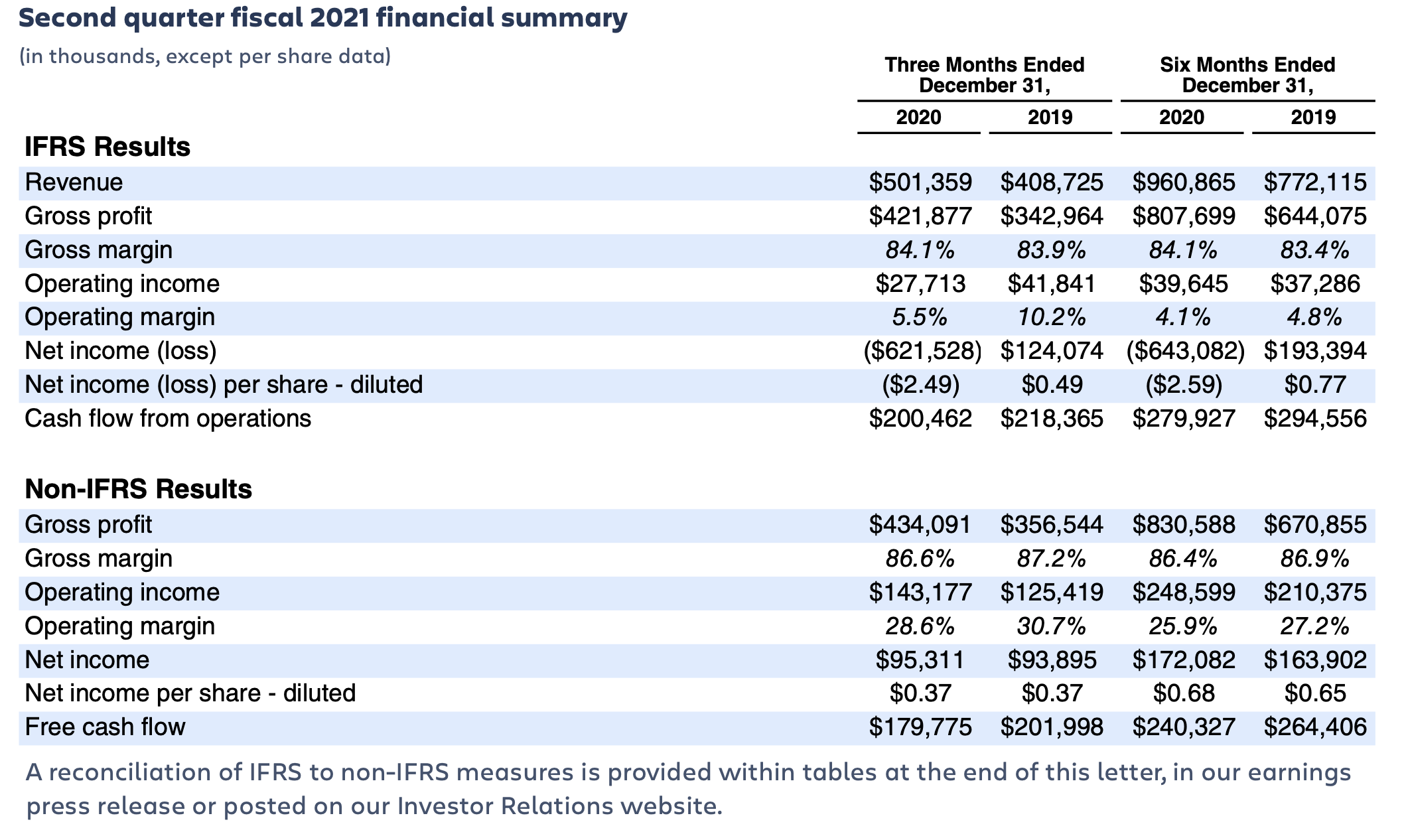

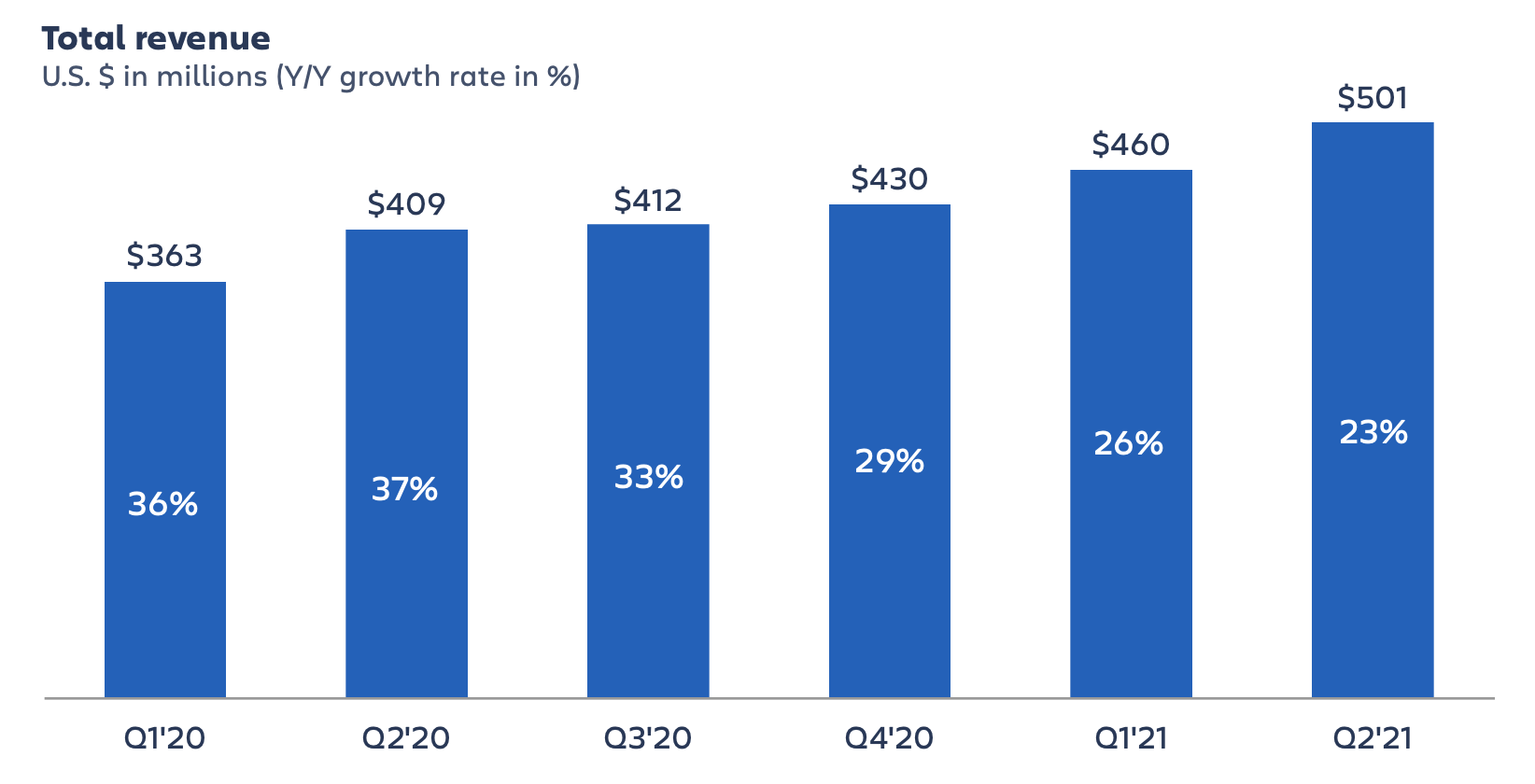

We realized strong financial performance in Q2’21. We achieved our first $500 million revenue quarter as we executed on our short-term objectives while continuing to make steady progress towards our long-term goals. Our cloud portfolio showed strength and we were pleased with the number of new customer additions and the continued trend of improved customer retention.

Highlights include:

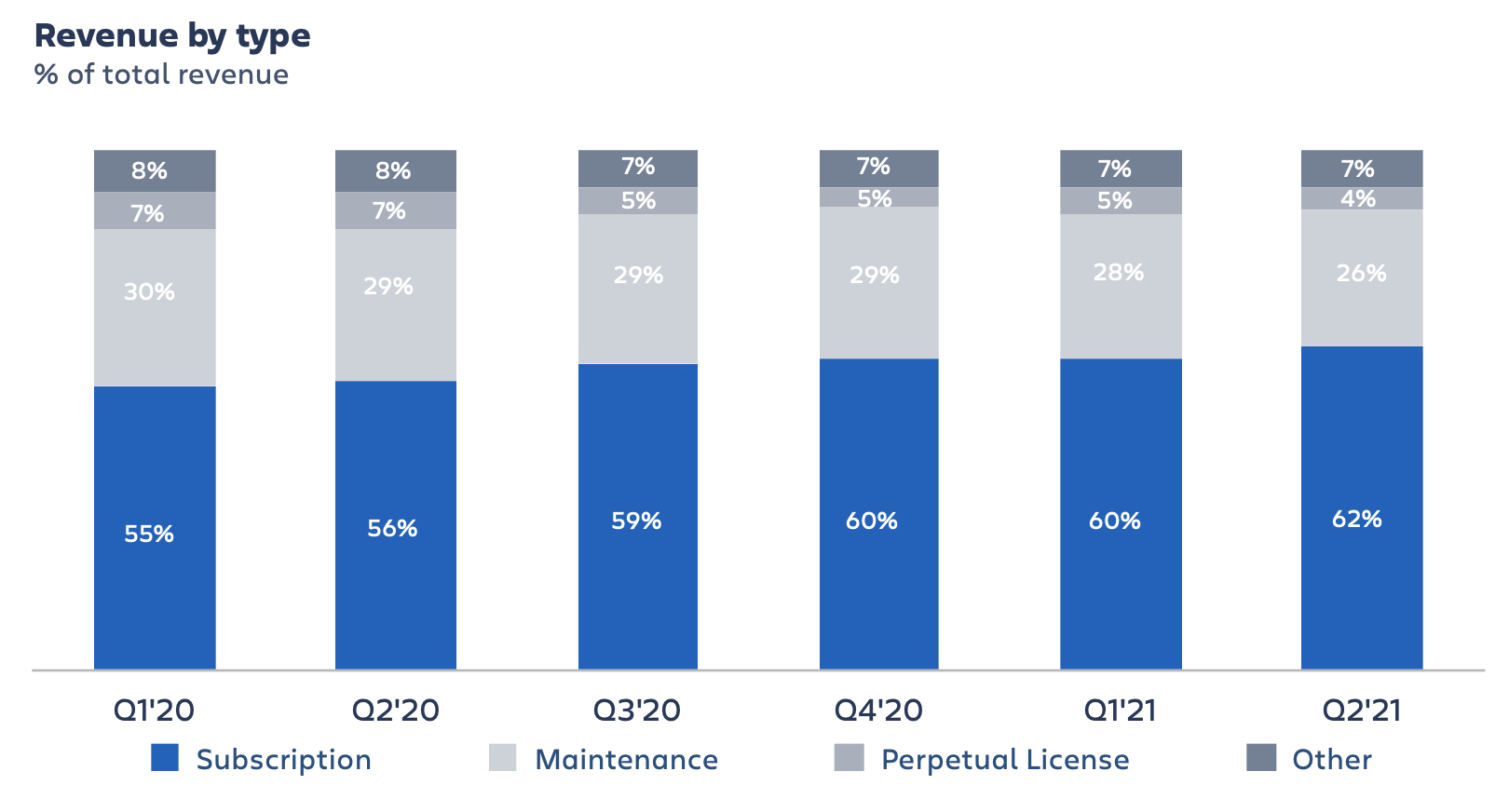

- For Q2’21, subscription revenue grew 36% year-over-year, driven by our cloud products as well as our data center offerings. Subscription revenue continues to be the primary driver of total revenue growth.

- Better than expected server activity as customers purchased additional license capacity ahead of new license sales ending in Q3’21. Demand was primarily driven by partners in EMEA and APAC.

- Effective execution against our ambitious hiring plans to close out CY2020. We added 467 net new Atlassians in Q2’21, with the majority in R&D. We will continue to invest purposefully in 2H fiscal 2021 as we position Atlassian to drive durable growth and win in our large addressable markets.

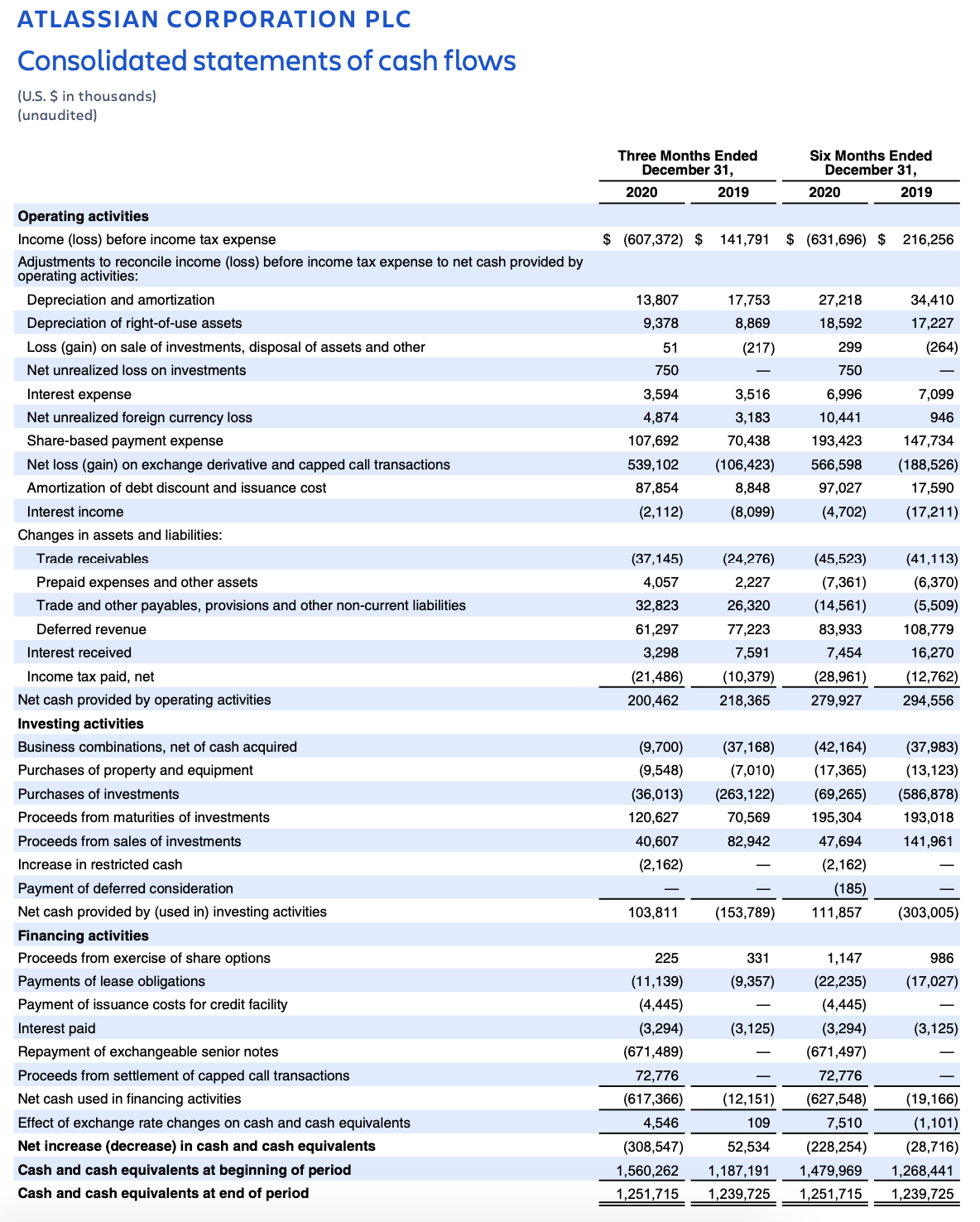

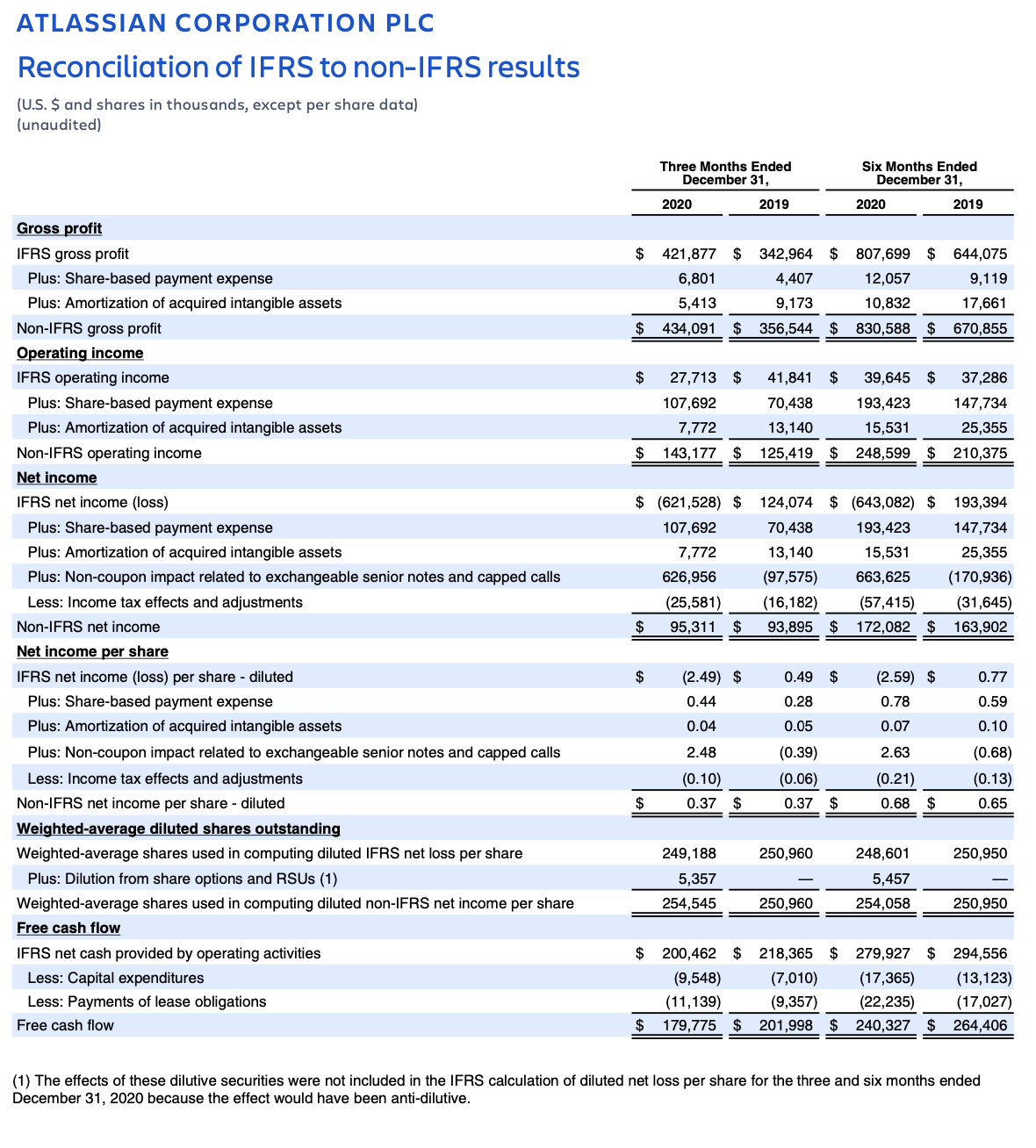

- Strong free cash flow generation of $179.8 million, representing a 36% free cash flow margin.

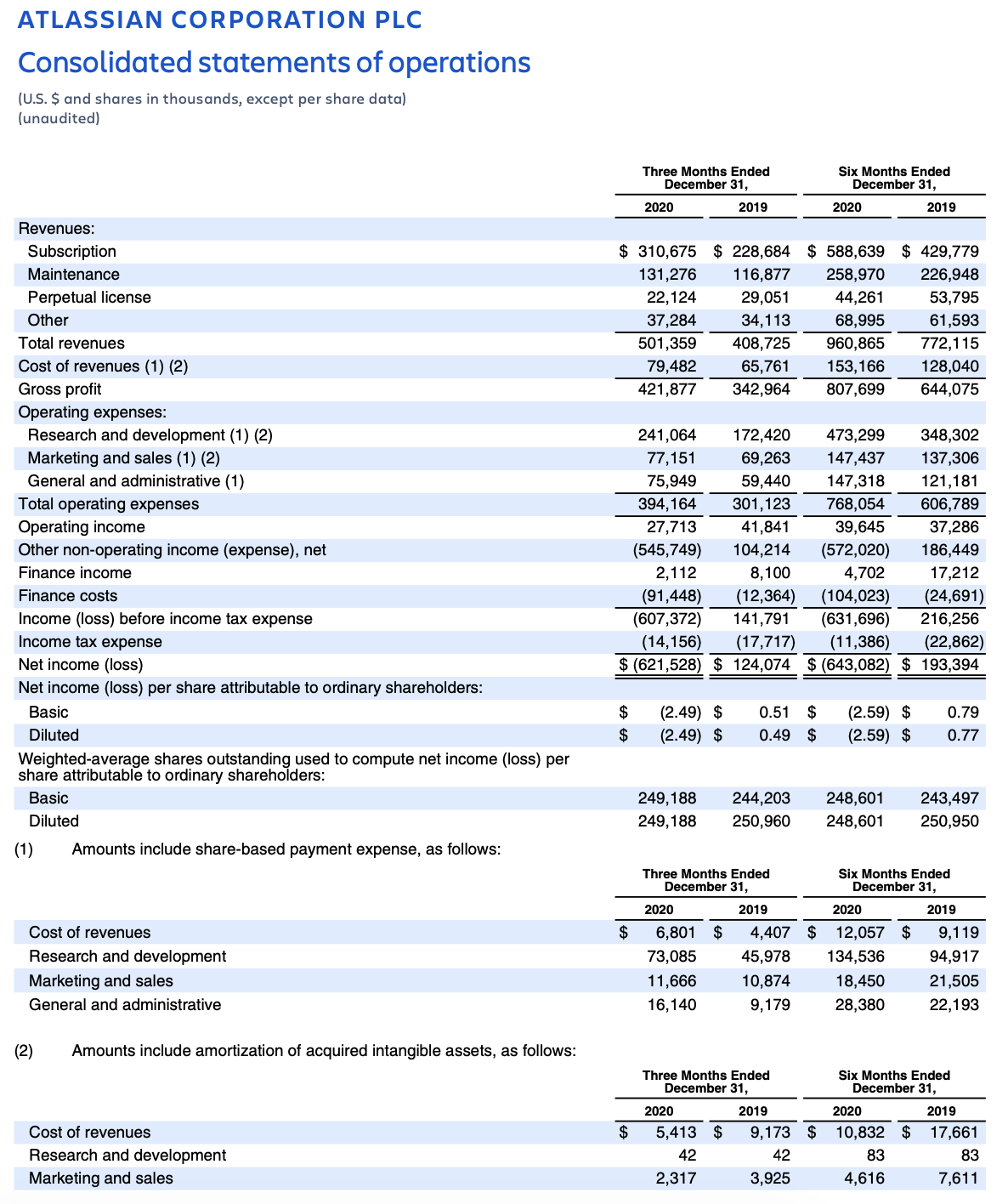

Revenue

Total revenue for Q2’21 was $501.4 million, up 23% year-over-year. Revenue by line item in Q2’21:

- Subscription revenue was $310.7 million, up 36% year-over-year.

- Maintenance revenue was $131.3 million, up 12% year-over-year.

- Perpetual license revenue was $22.1 million, down 24% year-over-year.

- Other revenue was $37.3 million, up 9% year-over-year.

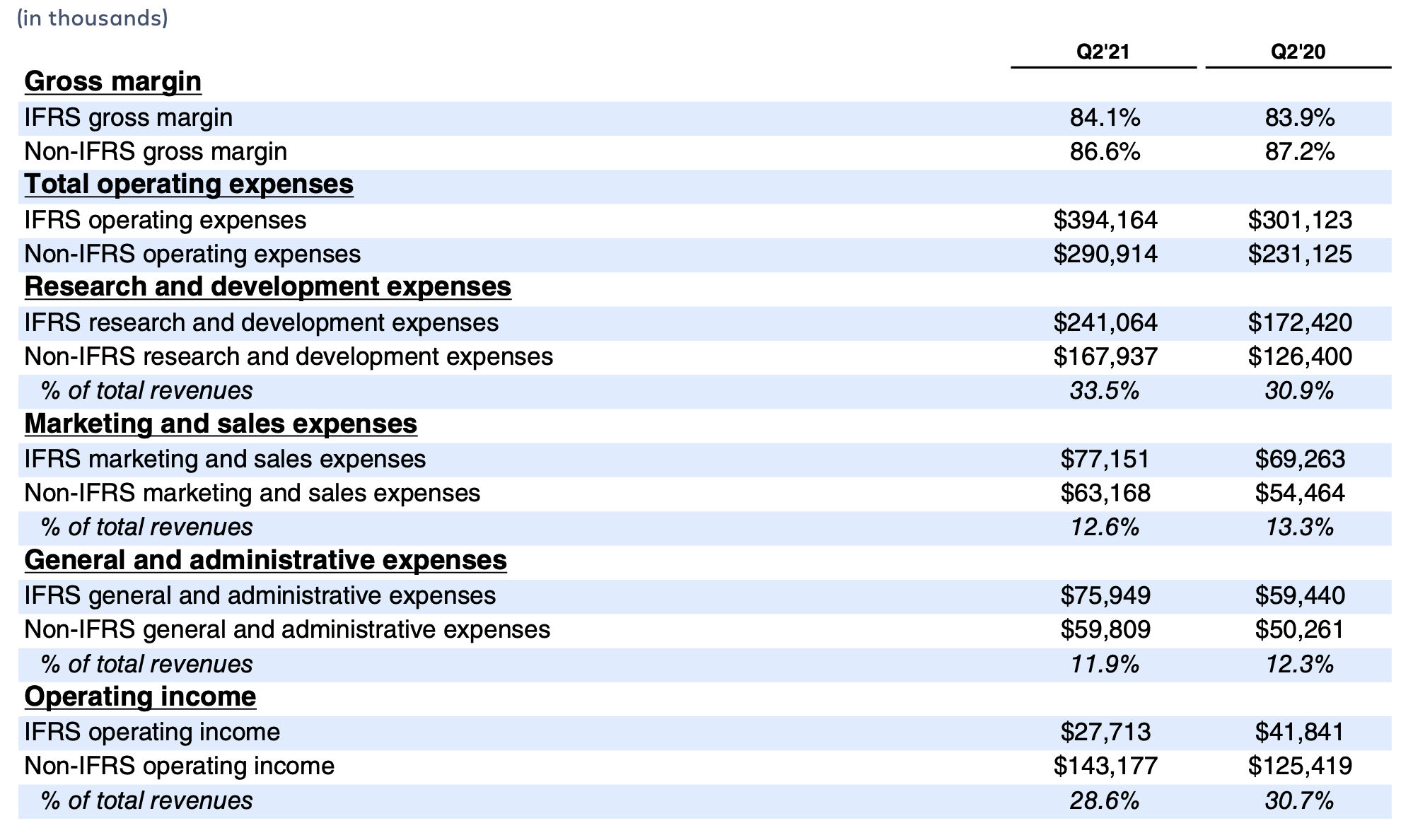

Margins and operating expenses

Headcount

Total employee headcount was 5,752 at the end of Q2’21, an increase of 467 employees since the end of Q1’21. The majority of the increase was in R&D.

Net income

IFRS net loss was $621.5 million, or ($2.49) per diluted share, for Q2’21 compared with an IFRS net income of $124.1 million, or $0.49 per diluted share, for Q2’20.

IFRS net loss for Q2’21 included a charge of $539.1 million recorded in “other non-operating income (expense), net,” compared with a gain of $106.4 million in Q2’20 relating to our exchangeable senior notes and related capped calls. Of this amount, a loss of $440.4 million is related to marking to fair value the exchange feature of these notes and related capped calls, that remain outstanding as of quarter end, and a net loss of $98.7 million is related to the net impact of repurchasing a portion of the notes and unwinding of the related capped calls during this quarter. Further, we took an $87.3 million charge related to accelerated amortization of the unamortized notes discount and issuance costs.

Non-IFRS net income was $95.3 million, or $0.37 per diluted share, for Q2’21 compared with non-IFRS net income of $93.9 million, or $0.37 per diluted share, for Q2’20.

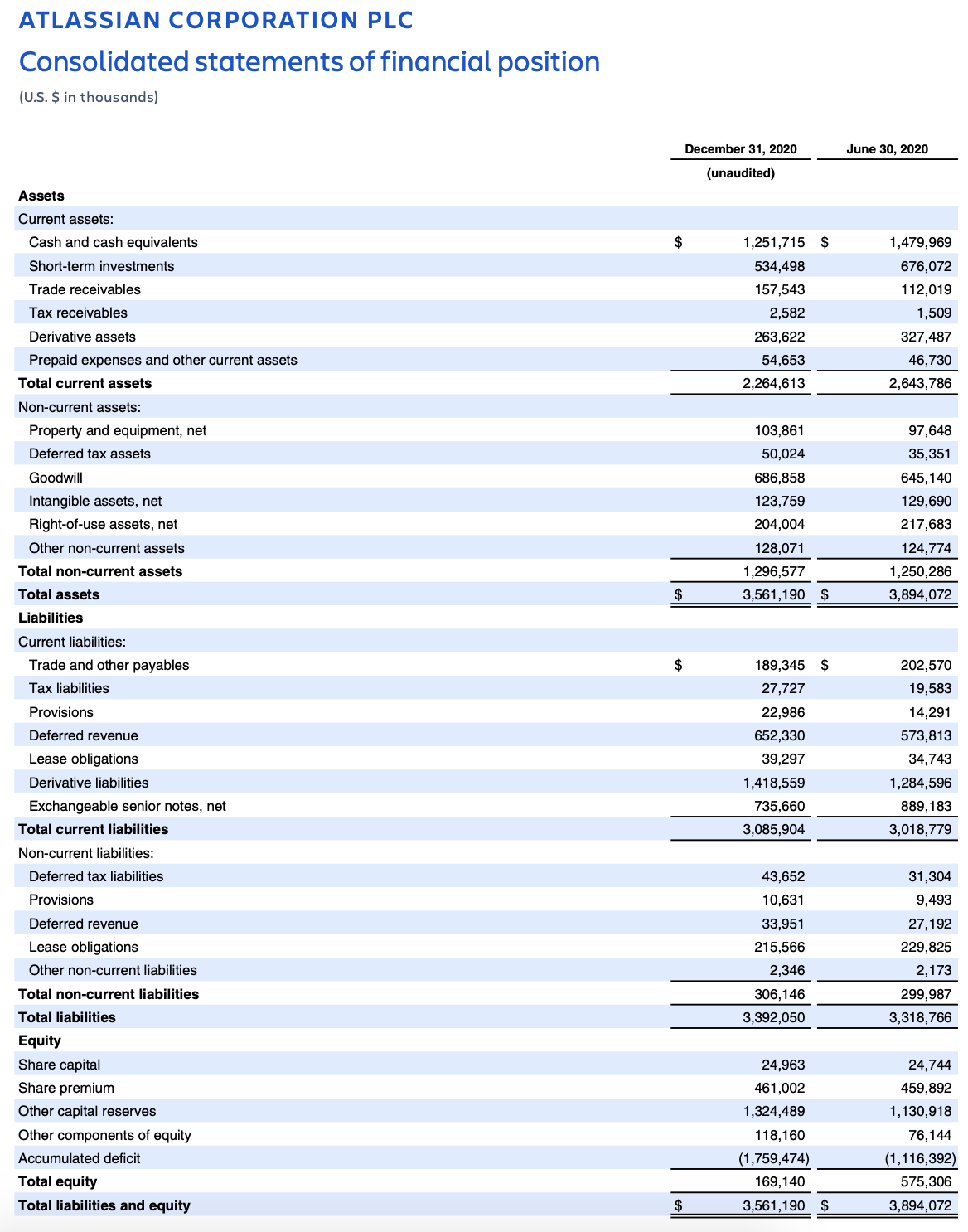

Balance sheet

We finished Q2’21 with $1.8 billion in cash, cash equivalents, and short-term investments.

During Q2’21, we used $671.5 million in cash to repurchase a portion of our outstanding notes in privately negotiated transactions and received $72.8 million in cash from the unwinding of the related capped calls. The net impact resulted in cash outflows of $598.7 million which is reflected in cash used in financing activities on our statement of cash flows.

Free cash flow

Cash flow from operations for Q2’21 was $200.5 million, while capital expenditures totaled $9.5 million and payments of lease obligations totaled $11.1 million, resulting in free cash flow of $179.8 million. The free cash flow margin for Q2’21, defined as free cash flow as a percentage of revenue, was 35.9%.

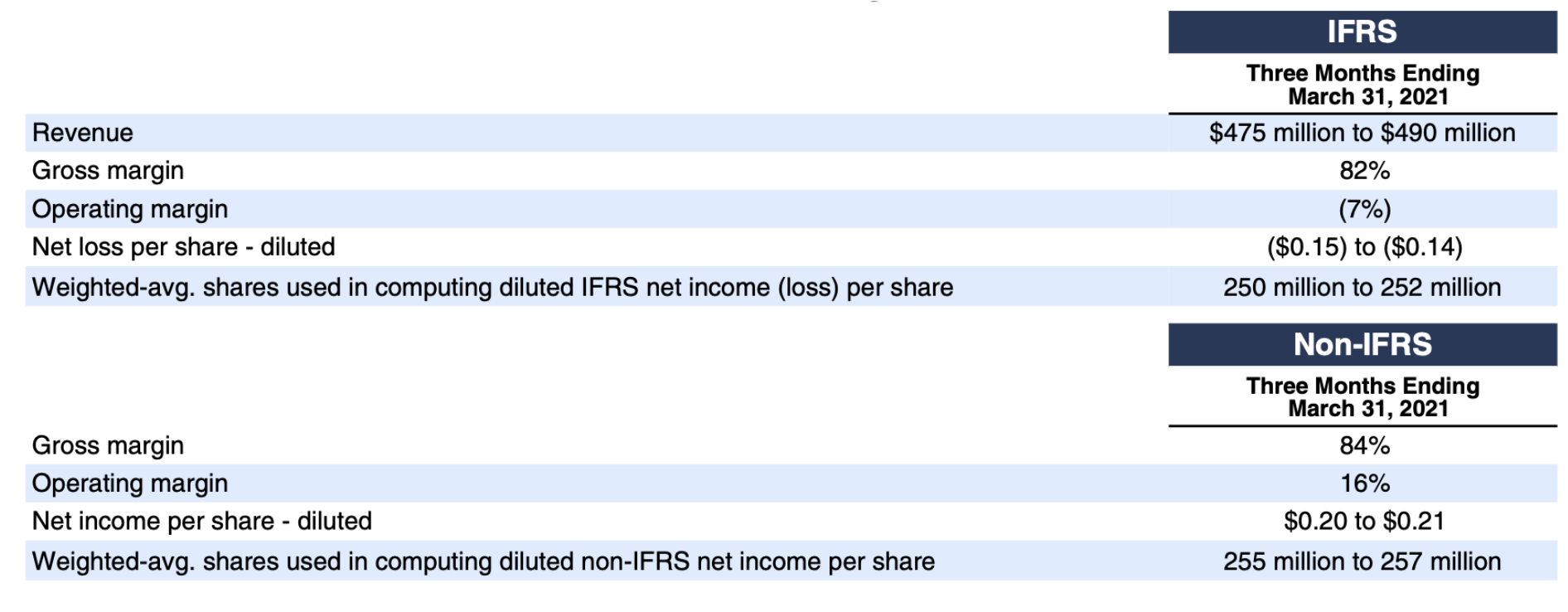

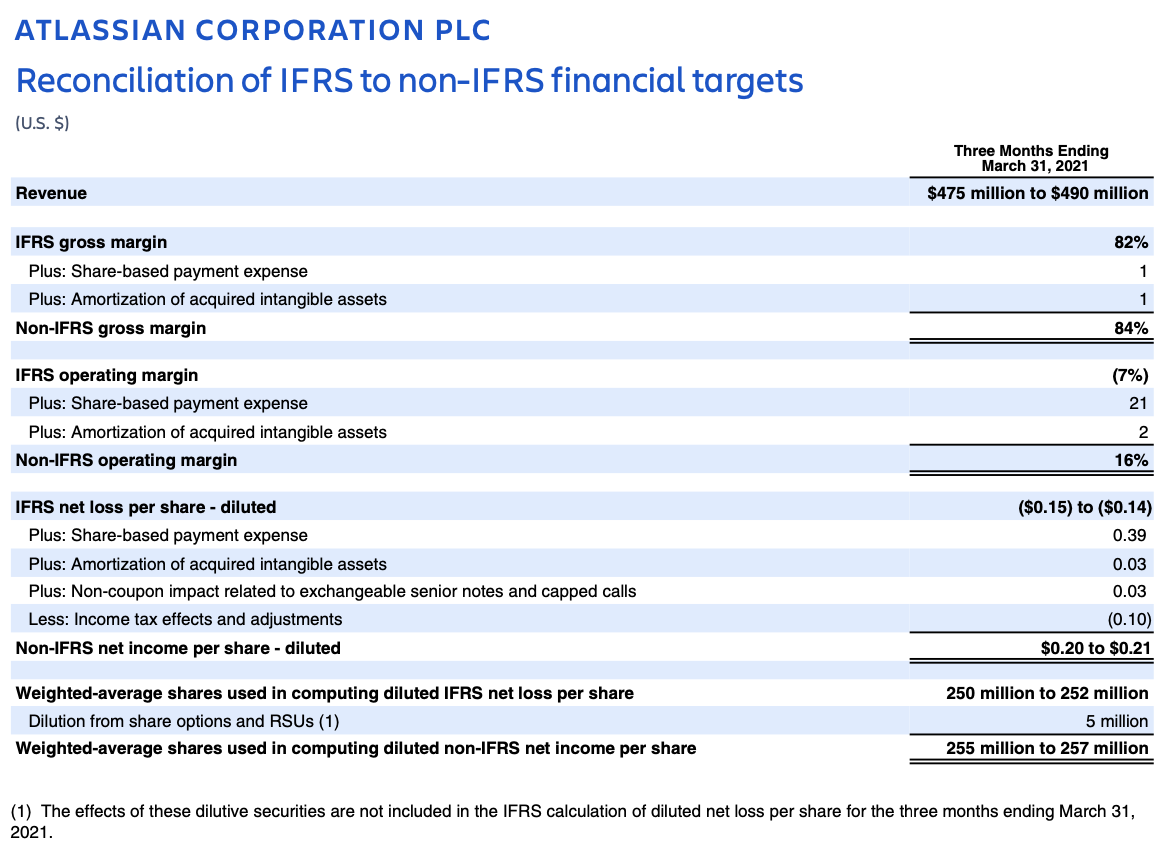

Financial targets

Third-quarter and fiscal 2021 outlook

Revenue

As we move into our first full quarter of server-to-subscription migration after our server product ‘end-of-life’ announcement, we expect greater variability in our revenue growth, consistent with comments at Investor Day and prior forward-looking commentary.

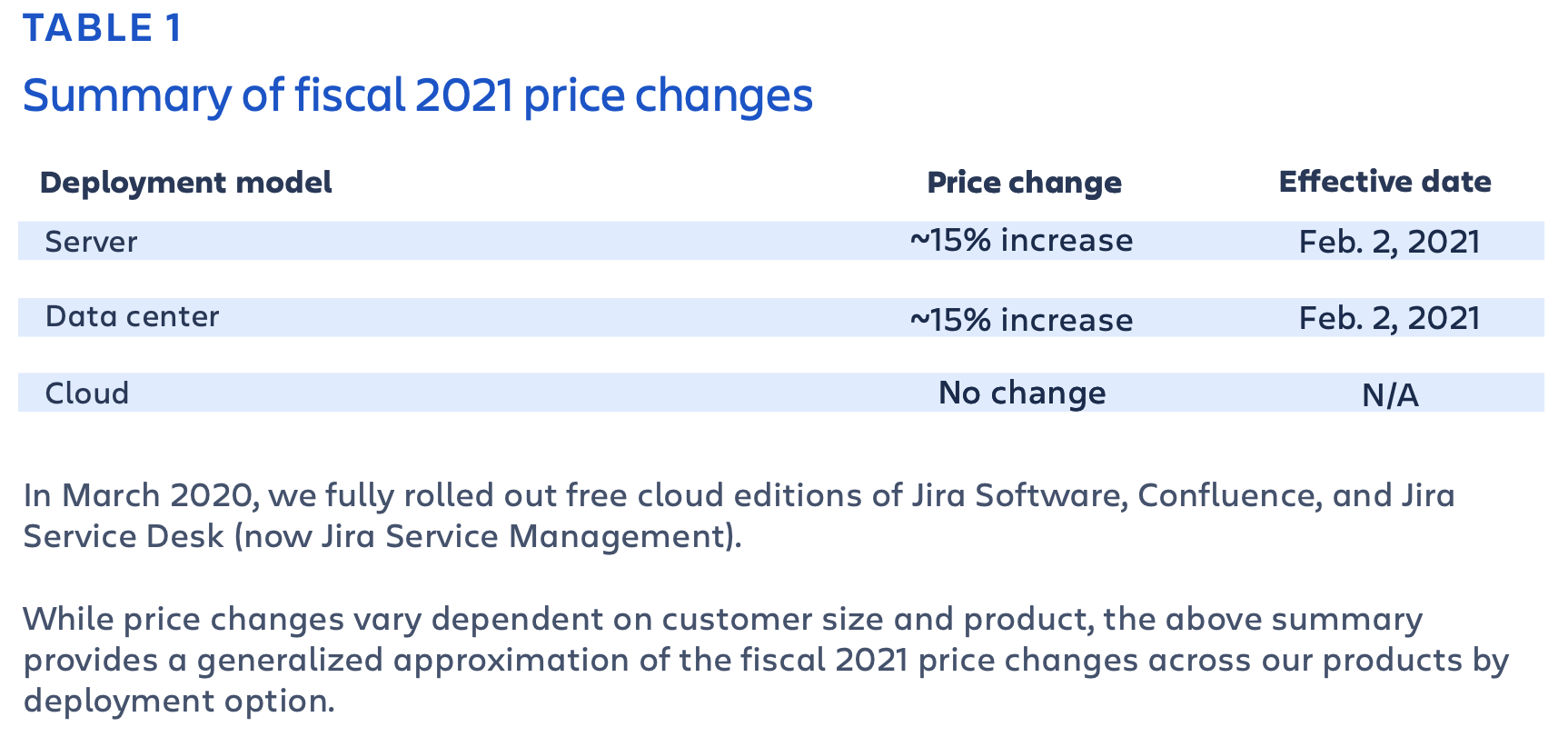

- In Q3, we continue to expect the overall server revenue growth rate to decline from Q2. That said, with the end of new server license sales and on-premises price changes effective February 2, 2021, we expect some server customers will purchase additional licenses and early renew their maintenance contracts. We did observe a modest amount of early renewal activity in Q2.

- We have included below, the same tables describing our price increases and end-of-life timelines included in our Q1’21 shareholder letter for reference.

In addition, we expect to see the following trends for the remainder of fiscal 2021:

- Subscription revenue will be the primary driver of growth. We expect to achieve subscription revenue growth in the mid-30%s consistent with the mid-term fiscal 2021 and fiscal 2022 targets articulated at Investor Day.

- While the initial leading indicators are encouraging, migrations will have only a modest impact on fiscal 2021 revenue. We continue to expect this revenue driver to build steadily over time. As shared at Investor Day, we expect half of our server customers will migrate in fiscal 2023 and beyond. It’s important to note our assumption that medium and large-sized customers, which have a greater impact on revenue, will take more time to migrate than smaller customers. Of this cohort, we estimate that approximately two-thirds will migrate after fiscal 2022.

As detailed last quarter, revenue growth will slow through the remainder of fiscal 2021. We continue to expect revenue growth to be impacted in fiscal 2022 before improving. The following factors will impact revenue growth in the short-term:

- Contracting server business – Our server business is slowing as new customers land in cloud products, and existing server customers expand at a slower rate as they prepare for their cloud migration journey. This will result in further declines in both license and maintenance revenue growth. In Q4’21, we expect to recognize less perpetual license revenue as we will no longer offer new server licenses. Note that server customers will still have the ability to upgrade their existing server licenses through February 2, 2022. Overall, we expect to see modest perpetual license revenue through Q3’22.

- Enterprise loyalty discounts applied to migrating customers – At enterprise-level user tiers, we are offering loyalty discounts to server customers to incentivize migration.

- Pricing – Price changes will have less impact on fiscal 2021 revenue growth relative to fiscal 2020, consistent with prior commentary. In particular, this driver impacts the growth rate of our cloud revenue.

- COVID-19 – While we are pleased with how churn has consistently improved since Q4’20, churn has a multi-quarter impact largely on our cloud revenue due to the loss of those customers’ subscription dollars.

- Marketplace – Marketplace revenue, which is reflected in ‘Other revenue,’ will be impacted by the overall contraction of the server business, as well as temporarily lower take rates on the sales of cloud apps through the Atlassian Marketplace to incentivize further cloud app development. This also remains consistent with prior commentary.

- Free editions – Consistent with our strategy, free editions of Jira Software, Confluence, and Jira Service Management have significantly increased the volume at the top of our GTM funnel. Until very recently, teams using free editions have, on average, taken more time to convert into paying customers than was the case with our historic starter license-driven funnel. We are growing increasingly confident in the economics of our free editions strategy and expect the cumulative revenue headwind to continue to decrease and then turn positive over time.

Profitability

In 2H fiscal 2021, we will maintain our approach of “looking through” short-term growth fluctuations and investing to drive long-term durable growth. We continue to have ambitious hiring plans, with a focus on R&D roles, and we maintain the expectation that we will generate lower operating and free cash flow margins in fiscal 2021 vs. fiscal 2020.

We continue to expect the following trends in fiscal 2021:

- Gross margin is expected to decline in 2H vs. 1H due to the business mix shift from server to cloud. This impact will be primarily driven by additional personnel costs to support cloud migrations and our cloud customer base, as well as increased hosting costs for cloud enterprise customers.

- Operating margin is expected to decline in 2H as server revenues contract and we continue to invest heavily in cloud R&D. We will continue investing in our cloud platform, supporting microservices, improving our migration tools, developing new products, and driving product improvements. Additionally, the commencement of the new calendar year brings the annual reset of employer payroll taxes.

- Free cash flow is expected to be impacted by a greater amount than operating margins as a result of our business mix shift to the cloud. Maintenance contracts for our server products are only offered on annual terms, while we offer subscriptions for our cloud products on annual or monthly terms. Approximately 75% of our cloud customers currently utilize monthly billing. In the short term, the shift to the cloud, and the likely related shift in billing term, will create a larger headwind for free cash flow than the impact we see on revenue. Over the long term, as more enterprise customers migrate to the cloud, we expect this headwind to subside.

- Free cash flow will also be impacted negatively by approximately $45 million in fiscal 2021 vs. fiscal 2020 due to higher cash taxes of approximately $25 million and lower interest income of approximately $20 million.

In closing, we continue to invest towards realizing our long-term goals: to serve our customers’ mission-critical workflows as a cloud-first company and to deliver technical and non-technical teams world-class innovation in massive markets. Q2 was a solid quarter on this multi-year journey, and we look forward to the road ahead.

– James

The Bottom Line

- We achieved strong financial results in Q2’21: our first $500 million revenue quarter with 23% year-over-year growth, subscription growth (driven by cloud) of 36% year-over-year, and non-IFRS operating margin of 29% and 36% free cash flow margin.

- We continue to expect variability in revenue growth given the multi-year migration of customers from server to cloud. Subscription revenue will continue to be the primary driver of overall growth, with a target for mid-30% year-over-year growth in fiscal 2021 and fiscal 2022. At the same time, we anticipate overall revenue growth will decline during the remainder of fiscal 2021 and will be impacted in fiscal 2022 before improving.

- We continue to invest to drive durable long-term growth and will maintain ambitious hiring goals for fiscal 2021. This will impact our profitability which we expect to decline in 2H fiscal 2021 in comparison with 1H fiscal 2021.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements, within the meaning of the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. All statements other than statements of historical fact could be deemed forward looking, including risks and uncertainties related to statements about our products, customers, anticipated growth, strategy, go-to-market model, acquisitions, environmental goals, outlook, effects of the COVID-19 pandemic, technology and other key strategic areas, and our financial targets such as revenue, share count, and IFRS and non-IFRS financial measures including gross margin, operating margin, net income (loss) per diluted share and free cash flow.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission from time to time, including the section titled “Risk Factors” in our most recent Forms 20-F and 6-K (reporting our quarterly results). These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

ABOUT NON-IFRS FINANCIAL MEASURES

Our reported results and financial targets include certain non-IFRS financial measures, including non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow. Management believes that the use of these non-IFRS financial measures provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of our results of operations, and also facilitates comparisons with peer companies, many of which use similar non-IFRS or non-GAAP financial measures to supplement their IFRS or GAAP results. Non-IFRS results are presented for supplemental informational purposes only to aid in understanding our results of operations. The non-IFRS results should not be considered a substitute for financial information presented in accordance with IFRS, and may be different from non-IFRS or non- GAAP measures used by other companies.

Our non-IFRS financial measures include:

- Non-IFRS gross profit. Excludes expenses related to share-based compensation and amortization of acquired intangible assets.

- Non-IFRS operating income. Excludes expenses related to share-based compensation and amortization of acquired intangible assets.

- Non-IFRS net income and non-IFRS net income per diluted share. Excludes expenses related to share-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and discrete tax impact resulting from a non-recurring transaction.

- Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment and payments of lease obligations.

Our non-IFRS financial measures reflect adjustments based on the items below:

- Share-based compensation.

- Amortization of acquired intangible assets.

- Non-coupon impact related to exchangeable senior notes and capped calls:

- Amortization of notes discount and issuance costs.

- Mark to fair value of the exchangeable senior notes exchange feature.

- Mark to fair value of the related capped call transactions.

- Net loss on settlements of exchangeable senior notes and capped call transactions.

- The related income tax effects on these items, and discrete tax impact resulting from a non-recurring transaction.

- Purchases of property and equipment and payments of lease obligations.

We exclude expenses related to share-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and discrete tax impact resulting from a non-recurring transaction from certain of our non-IFRS financial measures as we believe this helps investors understand our operational performance. In addition, share-based compensation expense can be difficult to predict and varies from period to period and company to company due to differing valuation methodologies, subjective assumptions, and the variety of equity instruments, as well as changes in stock price. Management believes that providing non-IFRS financial measures that exclude share-based compensation expense, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, the related income tax effects on these items, and discrete tax impact resulting from a non-recurring transaction allow for more meaningful comparisons between our results of operations from period to period.

Management considers free cash flow to be a liquidity measure that provides useful information to management and investors about the amount of cash generated by our business that can be used for strategic opportunities, including investing in our business, making strategic acquisitions, and strengthening our statement of financial position.

Management uses non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow:

- As measures of operating performance, because these financial measures do not include the impact of items not directly resulting from our core operations.

- For planning purposes, including the preparation of our annual operating budget.

- To allocate resources to enhance the financial performance of our business.

- To evaluate the effectiveness of our business strategies.

- In communications with our Board of Directors and investors concerning our financial performance.

The tables in this shareholder letter titled “Reconciliation of IFRS to non-IFRS Results” and “Reconciliation of IFRS to non-IFRS financial targets” provide reconciliations of non-IFRS financial measures to the most recent directly comparable financial measures calculated and presented in accordance with IFRS.

We understand that although non-IFRS gross profit, non-IFRS operating income, non-IFRS net income, non-IFRS net income per diluted share, and free cash flow are frequently used by investors and securities analysts in their evaluation of companies, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results of operations as reported under IFRS.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our team collaboration and productivity software helps teams organize, discuss and complete shared work. Teams at more than 194,000 customers, across large and small organizations – including Redfin, NASA, Verizon, and Dropbox – use Atlassian’s project tracking, content creation, and sharing, and service management products to work better together and deliver quality results on time. Learn more about our products including Jira Software, Confluence, Jira Service Management, Trello, Bitbucket, and Jira Align at https://atlassian.com.

Investor relations contact: Martin Lam & Matt Sonefeldt, IR@atlassian.com

Media contact: Jake Standish, press@atlassian.com