An update to customers, stakeholders, and shareholders on our mission to unleash the potential in every team.

Fellow shareholders,

Atlassian closed out 2022 proud of everything we accomplished in yet another unpredictable year. Despite the current macroeconomic headwinds, the massive opportunities in front of us have not changed, and we’re ready to execute with relentless focus throughout 2023.

Continuing the trend from last quarter, existing customers are expanding their paid seats at a slower pace. We also continue to see solid growth in free editions of our cloud products, but more hesitancy to upgrade to paid editions. While these two macro-induced headwinds became more pronounced in Q2, calendar year 2023 will be all about helping our customers navigate these challenging times, absorbing the downstream impacts on our business, and setting ourselves up for long-term success.

To be clear, our competitive position remains unchanged. As customers seek to work more effectively, and accelerate digital transformation in an uncertain environment, they’re deepening their commitment to Atlassian. Cloud migrations are moving right along, customers are signing longer contracts, and retention remains healthy.

As we said last quarter, we intend to continue playing offense in our three large markets while balancing

our investments against the growth of our business overall. Atlassian’s unique business model, broad customer base, and agile approach to planning allow us to adapt to changes quickly, which is exactly what we’re doing.

We’re rebalancing our talent and resources to put increased focus on our largest growth opportunities: cloud migrations, the IT service management market, and serving enterprise customers. Atlassian is well positioned in these areas with significant momentum that can help us power through the turbulence ahead.

Of course, centering our investments on top growth initiatives also means shifting away from lower-priority endeavors. We’ll continue to manage expenses, invest responsibly for the long term, and be prudent stewards of capital as we respond to macroeconomic conditions.

Over our seven years as a public company, you’ve consistently seen us play the long game while being incredibly capital efficient. That’s a winning strategy and we’re sticking with it.

We have a passionate, versatile team that can adapt when priorities shift and address a multitude of challenges. We have innovative products that satisfy the most crucial use cases for companies large and small. And we have an incredible model that allows us to be patient and disciplined, even amidst a rapidly changing economy, so we can emerge even stronger. ![]()

Increasingly “cloudy” with sustained migration momentum

Atlassian remains focused on building a world-class cloud platform and making sure our customers benefit from everything it has to offer.

Migrations are tracking well, up nearly 2x year-over-year, and we continue to expect migrations to account for approximately 10 points of cloud revenue growth in FY23. We’ve also made it easier for enterprise customers to determine which migration approach is right for them with a dynamic automated form that matches them to the right migration support team based on their answers to a few simple questions.

Additionally, we completed two of our biggest migrations to date in Q2. 🎉 One of Australia’s largest banks migrated 25,000 users to Jira Software Cloud’s Enterprise edition, and a major UK-based bank moved a total of 30,000 user seats from Data Center editions of Jira Software and Confluence to our cloud platform. Working with mega-migrators like these resulted in tooling improvements and lessons learned that are already proving valuable for migrations of all sizes.

On the R&D side, our investment in “build once, run everywhere” platform capabilities and commitment to developer productivity allow our teams to roll out a steady stream of features and enhancements that make Atlassian’s cloud ever more accessible (and attractive) to customers.

In the case of the UK-based bank, the ability to archive Jira issues and support for multiple identity providers in Atlassian Guard unblocked their move to the cloud. And the launch of data residency in Germany in Q2 is unlocking cloud for more of our customers in regulated industries. Financial firms like Finoa and Giesecke+Devrient GmbH, as well as other security-conscious enterprise vendors like Celonis and Software AG migrated to our cloud products recently, backed by the growing list of compliance certifications and data residency options our platform has achieved.

In Germany, we have to be both innovative and compliant with strict regulatory standards. With Atlassian Cloud, we can do both…Creating multiple instances without any additional costs allows you to segregate data for security reasons.

– Tim Brutscher, Enterprise IT Architect at Software AG

To further incentivize migration and upgrades to higher editions, we launched new automation capabilities in Confluence Cloud’s Premium and Enterprise editions. Now admins can keep spaces organized by automatically archiving inactive content and any user can automate page creation for recurring team practices like monthly business reviews or retrospectives. With the average cloud customer already running over 650 automated operations each day, we know customers will get a lot of value out of this new feature and the Confluence Automation Template Library.

And it’s not just Confluence. We’re investing in automation capabilities that extend across – and even beyond – our platform. Jira Software users can connect with Bitbucket, GitHub, GitLab, and LaunchDarkly to automatically create development branches and feature flags. And thanks to a new integration with Amazon Web Services (AWS), ITOps teams can automate manual tasks like notifying stakeholders of an incident or restarting a server if it stops running. 🤖 The result is that customers can spend more time where it matters. That’s some pretty good ROI.

but wait! There’s more.

In addition to data residency in Germany and automation capabilities in Confluence, we shipped platform enhancements in Q2 that unlock migration for hundreds of thousands of seats, as well as product features that will delight customers in the cloud.

- Early access program for migrating nested groups

- Audit logs for Jira and Confluence permission changes

- Uptime SLA of 99.9% for Bitbucket Cloud Premium

- Self-serve organization deletion for admins

- HIPAA compliance for Jira Service Management

- New dashboards for request, change, and incident management, as well as Opsgenie alerts and insight objects

- Custom reporting for Jira Service Management

- Incoming call routing for Jira Service Management and Opsgenie

- Improved support for post-incident reviews

- Change calendar support for scheduling product freezes and maintenance windows

- MacOS builds for Bitbucket Pipelines

- DevOps toolchain visualization in Jira Software

- Support to link Atlassian Analytics dashboards with release versions in Jira Software’s release hub

- Enhanced support for parallel sprints in Jira Software

- External guest collaboration support in Confluence

- Bulk actions for admins of Trello Enterprise

Market deep-dive: IT service management 🤿

As companies move through digital transformation and grapple with aging systems that can’t keep up with the demands of the modern world, IT has gone from being a cost center to a strategic partner for the entire business. Recent CIO surveys and our own conversations with customers reveal that cybersecurity and incident management, plus automated workflows and reporting, top their list of priorities. This, as IT teams continue to forge closer relationships and tighter alignment with sales, HR, finance, and other teams across the business. All of which is exactly what Jira Service Management and our other ITSM products are designed for.

Jira Service Management steals the competition’s thunder 🌩️ 🤘

The ITSM market is one of Atlassian’s biggest areas of opportunity, with Jira Service Management leading the way as our fastest-growing product at scale.

- We’re the only vendor that brings software and IT teams together on the same platform.

- Developers have trusted us for over two decades, expediting expansion into IT and ops teams at companies of all sizes and in every industry.

- We have a consistent track record of investment delivering amazing customer value, including a handful of smart tuck-in acquisitions and a metric ton of home-grown innovations.

- Unlike competitors with interminable sales cycles and roll-out processes, teams can get up and running with Jira Service Management in as little as a day.

Between the superior time-to-value for customers, the steady drumbeat of improvements, and a price point that’s accessible to companies of all sizes, we are not surprised and believe this is why the industry is taking note. Atlassian was named a Leader for the first time in the 2022 Gartner® Magic Quadrant™ for IT Service Management Platforms1. This comes on the heels of being named a Leader in The Forrester Wave™: Enterprise Service Management, Q4 2021.

Not only that, but according to the Gartner 2022 report, A Buyer’s Guide to ITSM Platforms, “eight out of 10 IT organizations overspend on their IT service management (ITSM) platform subscriptions by half of the contract value because they purchase functions that do not get fully used2”. So we’ve introduced attractive incentives for customers who switch from their hulking ITSM monoliths to Jira Service Management.

Our “End Bad Service Management Now” campaign offers large companies compelling pricing incentives for their first year when they make the switch from a legacy vendor, and smaller companies can get up to 10 agents for free for 12 months. These moves, as we’ve done throughout our history, demonstrate our willingness to make bold, short-term trade-offs in the service of long-term payoffs.

Companies like PostNord, Saint Gobain, and Engie, massive enterprises going through intense digital and cultural transformations, have already switched over. Engie had been using a large-scale legacy solution but found it difficult to configure and use (not to mention the share of their budget it ate up). Since the switch, they’ve cut licensing costs by 67% and are saving roughly 200 hours of their IT team’s time each month. 🙌🏽 And from an end user’s perspective, the transition literally happened overnight: Engie’s admins turned off the old system one evening and turned on Jira Service Management the next day.

It was like lowering a curtain and raising it back up again.

– Jose Luis Lizárraga Castro, IT Support Engineer at Engie Mexico

Today, teams at over 45,000 companies use Jira Service Management, and we’re just getting started.

Ready and able to meet the challenges ahead

With Q3 underway, we will execute on the decisions we’ve made so far and continue to rebalance our investments as the situation calls for. We’ve played offense amid uncertainty more than once in our 20 years as a company, and we’re confident that our trademark vigilance and discipline will guide us through successfully once again.

As always, we’re incredibly grateful to the Atlassian team for staying focused on delivering great products, and to our customers and partners for their passion in building a vibrant community around us. Our teams are focused and fired up. We’ve positioned ourselves for success in a challenging environment, and we’re ready to get after it. (As we say in Australia, “we’re not here to #@!% spiders.” 🇦🇺)

Here’s to the road ahead, and to unleashing the potential of every team.

– Mike and Scott

the bottom line

- The macro-induced headwinds around seat expansion within existing customers and free-to-paid conversion became more pronounced this quarter, particularly with SMB customers. Atlassian is responding by rebalancing our investments to focus more on our biggest growth opportunities: cloud migrations, the ITSM market, and serving enterprise customers.

- Cloud migrations and the release of new features continue trucking along. We’re seeing customers commit deeper to Atlassian despite the uncertain economic backdrop.

- Jira Service Management is a rising star in the ITSM space, surpassing 45,000 customers in total, earning Atlassian recent recognition by industry experts.

- Our teams are executing with urgency and dedication. We have the right experience, the right talent, and the right strategies for long-term success. We’re ready for what lies ahead.

Customer highlight reel 📽️

As mentioned above, we continue to see headwinds impacting new customer conversion. We added 4,004 net new customers in Q2, bringing our total customer count to 253,177. I’m encouraged by the number of people coming to our sites and signing up for Free editions of our products, which continues to grow at healthy rates. The number of monthly active users also continues to perform well, underscoring the mission-critical role our products play for our customers.

The “High Velocity” ITSM event we hosted in London was a big highlight of my December. We spent the day with hundreds of customers and prospects from across industries, plus thousands of virtual attendees, discussing service management practices and digital transformation.

I had the privilege of hosting a live Q&A with two of our enterprise customers, Edenred and Arvato Systems, where we discussed their adoption of Jira Service Management and the incredible benefits they’ve experienced to date. We also saw a great response to our new “End Bad Service Management Now” campaign with many of our largest enterprise customers asking how Atlassian can help them modernize their ITSM offerings and save money in the process.

And the customer event train keeps on rolling! Next week, on February 9th, we head to Berlin for our agile/DevOps-focused event, “Unleash.” Along with meeting as many of our European customers as possible, I’ll be doing a fireside chat with Atlassian’s Chief Trust Officer, Adrian Ludwig, focused on coping with emerging cybersecurity threats, both from a technical and customer relations perspective. 🔐

If you happen to be in the area, I’d love to set up a time to meet on or around the 9th. Otherwise, you can register for the live stream here and experience the event virtually. I look forward to speaking with you soon, either at the event, on our earnings call this afternoon, or whenever we cross paths.

– Cameron

Financial highlights 📈

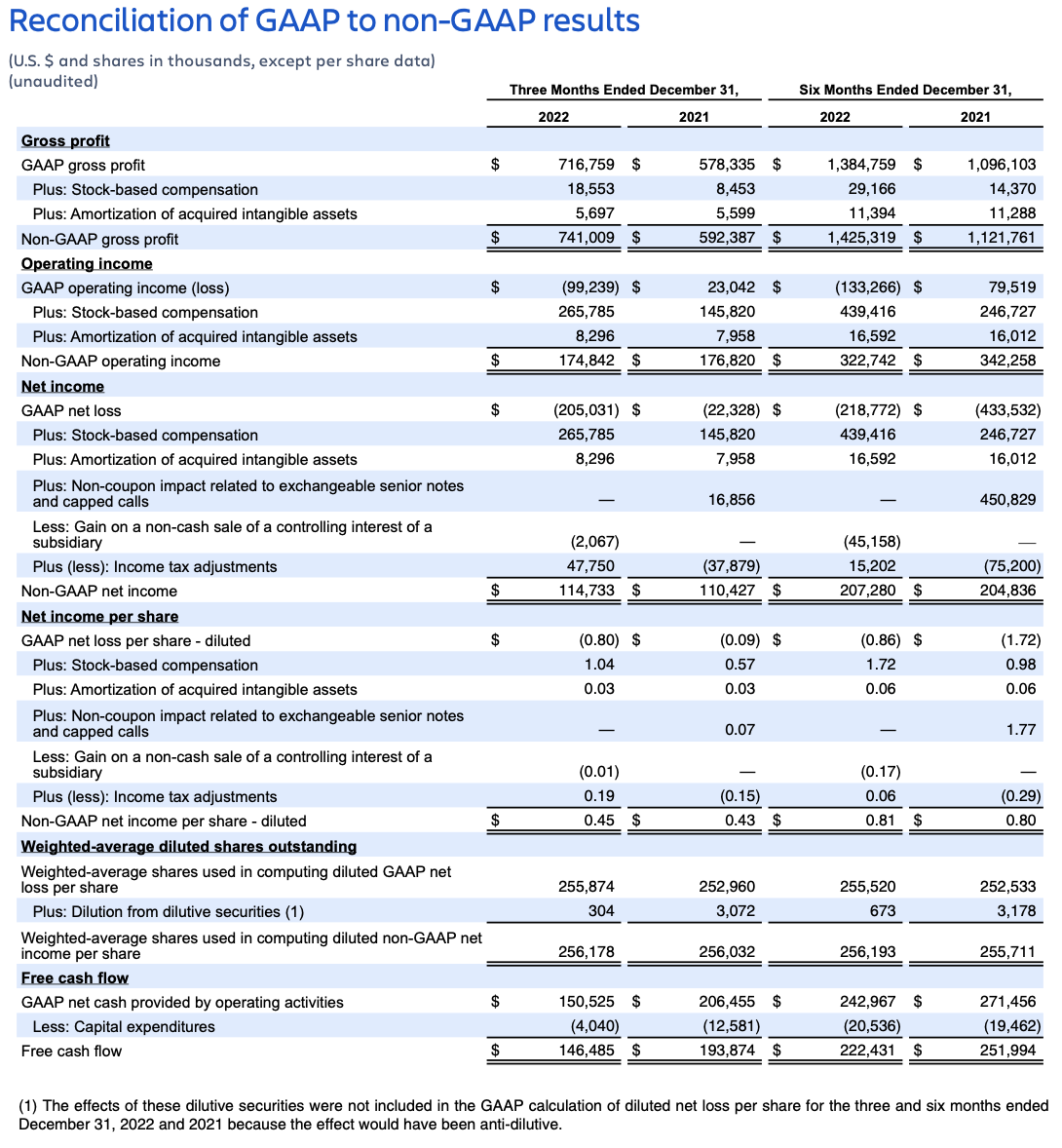

A reconciliation of GAAP to non-GAAP measures is provided within the tables at the end of this letter as well as in our earnings press release, and on our Investor Relations website.

Second quarter fiscal year 2023 highlights

We delivered solid financial results in Q2 with steady execution in a challenging and uncertain macroeconomic environment resulting in revenue, gross profit, and operating income exceeding our expectations.

Strong revenue growth from Data Center and Marketplace offerings offset weaker-than-expected results in cloud, which continues to be impacted by macro headwinds, particularly in the SMB customer base. We continue to be responsive to these changes by managing costs while investing against the long-term opportunity in our three large markets and related strategic priorities.

We are managing the company for the long term and are well-positioned to successfully navigate the near-term macroeconomic turbulence and emerge a stronger company.

Highlights for Q2’23 include:

All growth comparisons below relate to the corresponding period of last year, unless otherwise noted.

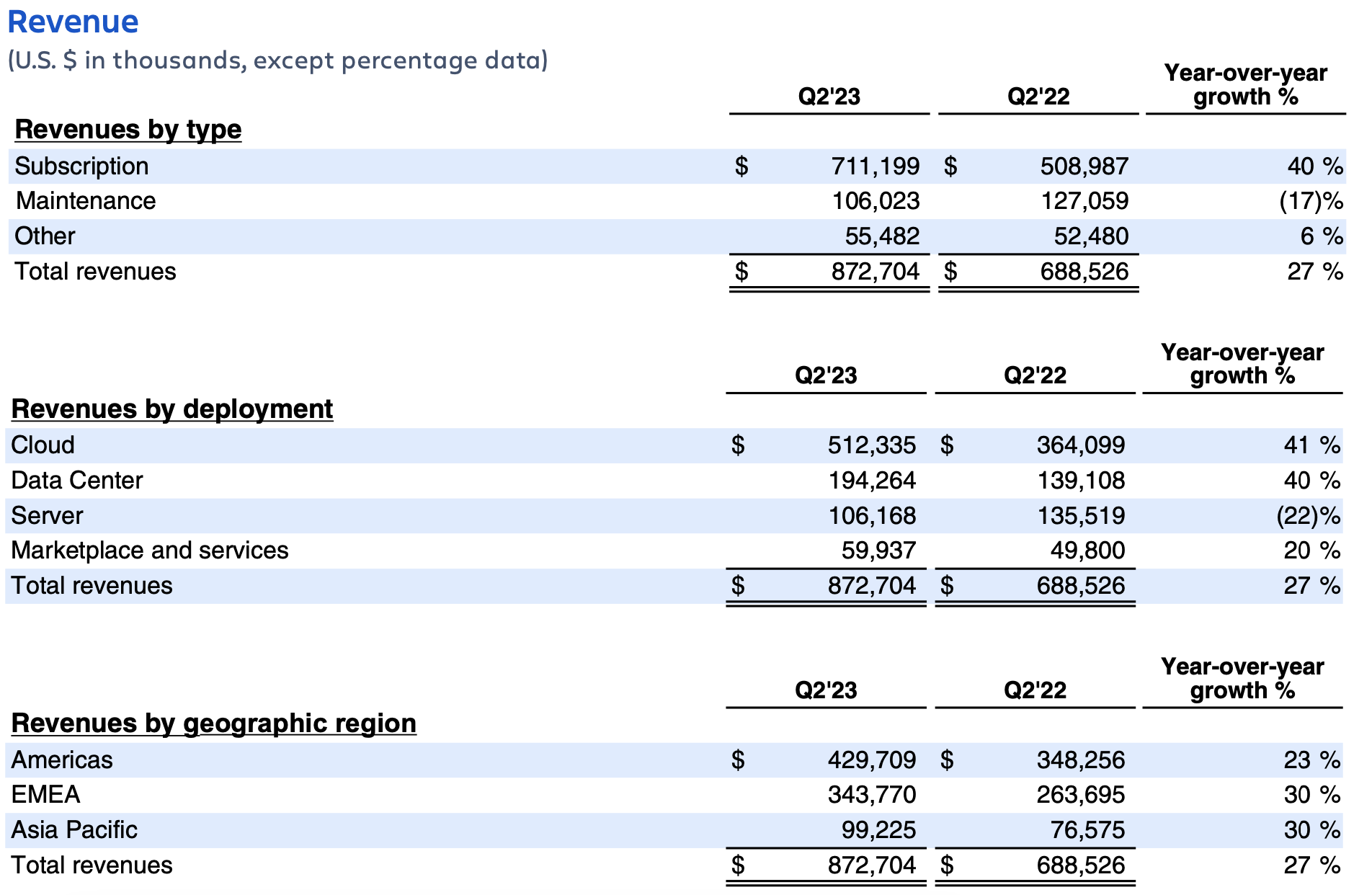

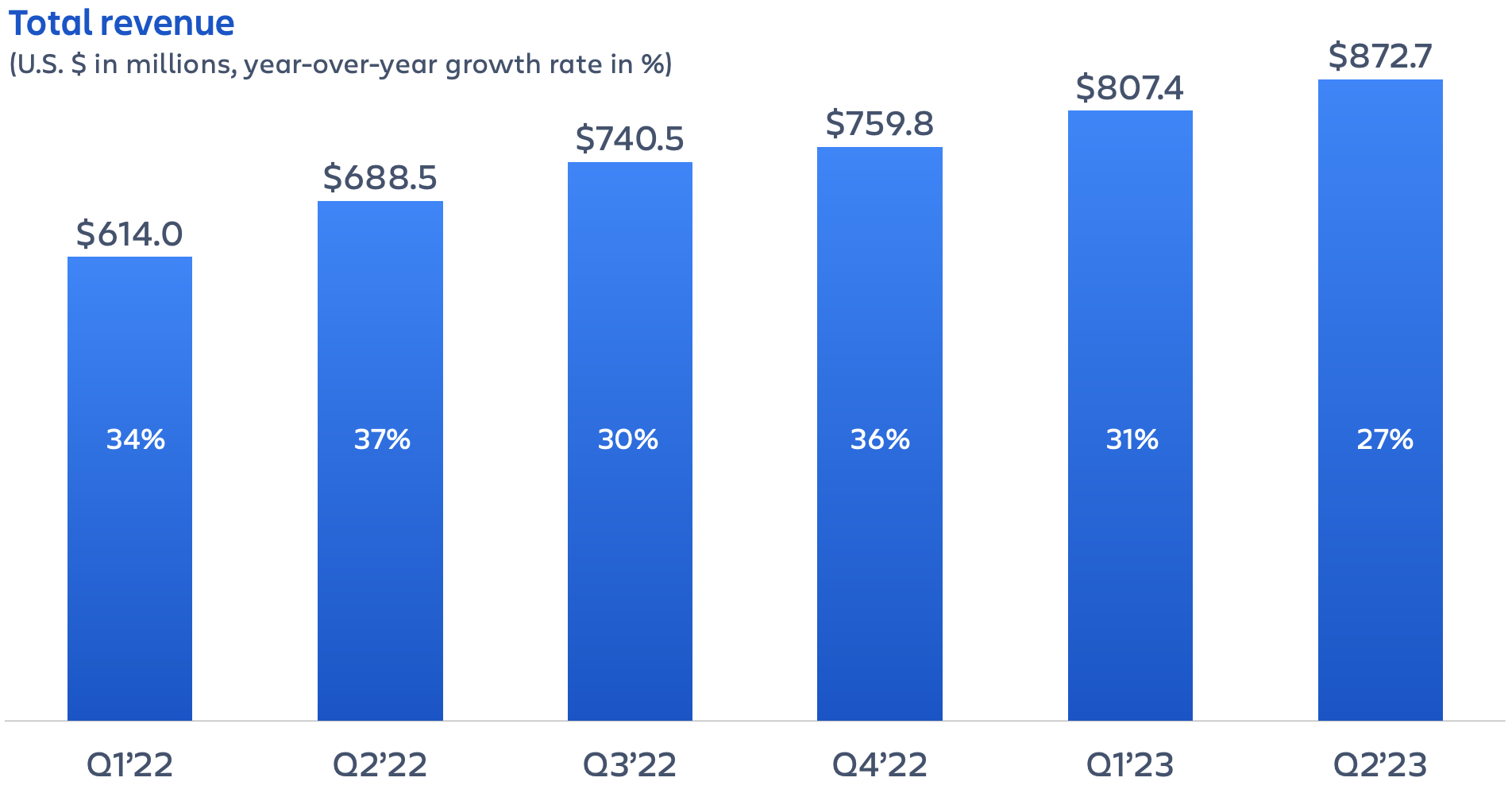

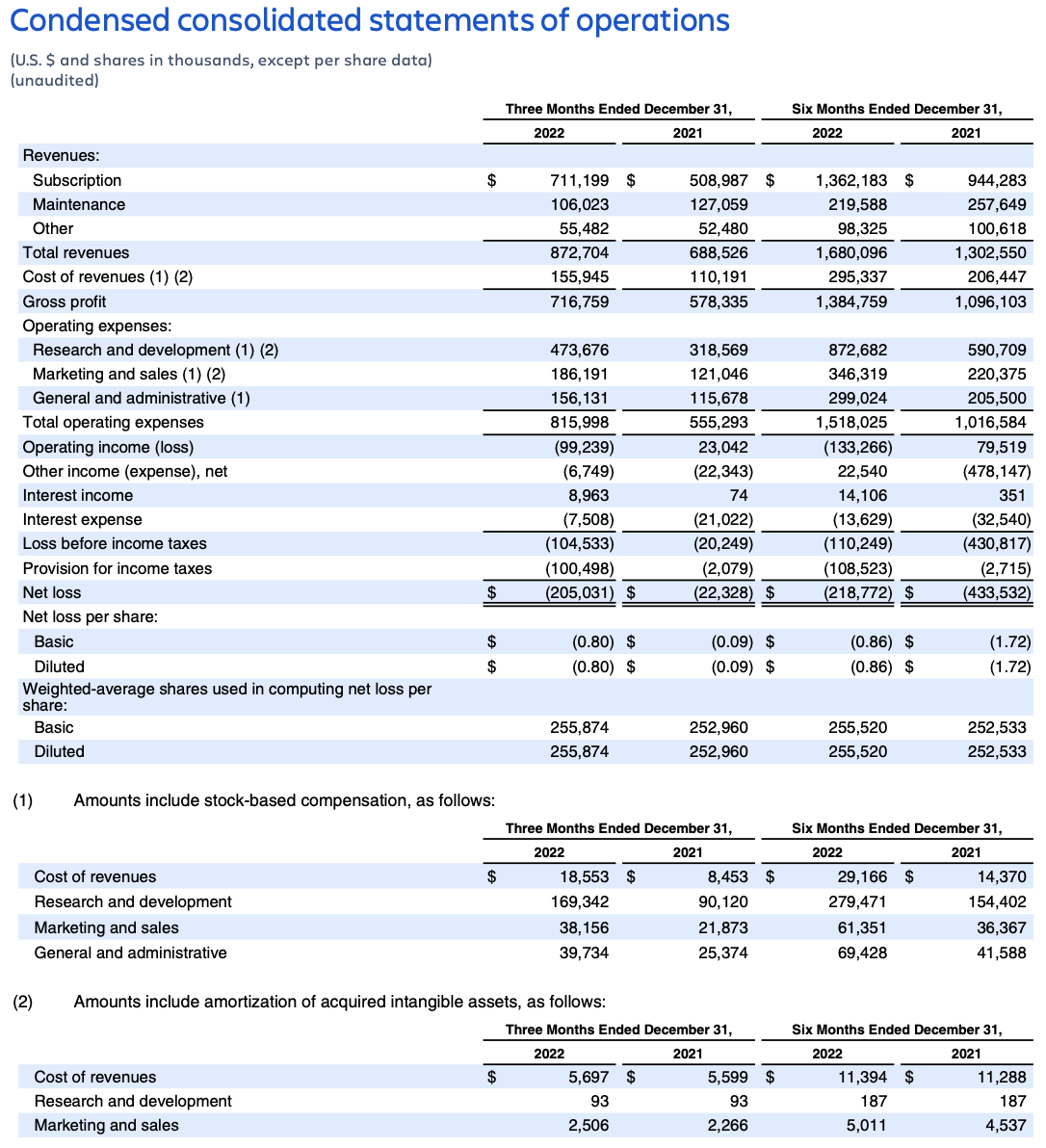

- Revenue of $873 million increased 27%, driven by growth in our Cloud and Data Center offerings.

- GAAP gross margin of 82% decreased 2 percentage points. Non-GAAP gross margin of 85% decreased 1 percentage point, driven by business mix shift to the cloud.

- GAAP operating expenses of $816 million increased 47%. Non-GAAP operating expenses of $566 million increased 36%, driven by growth in R&D and sales and marketing investments across our target markets and strategic priorities.

- GAAP operating loss was $99 million. GAAP operating margin of (11%) decreased 15 percentage points. Non-GAAP operating income of $175 million decreased 1% and non-GAAP operating margin of 20% decreased 6 percentage points.

Lastly, we are pleased to announce the initiation of a share repurchase program of up to $1 billion. This program underscores our confidence in our business, conviction in our significant long-term opportunities, and view that our shares are undervalued. Our scale, balance sheet, and unique business model which generates consistent free cash flow allow us to opportunistically return capital to shareholders while also investing for durable long-term growth.

Revenue growth in the quarter was driven by subscription revenue, which grew 40%. Despite ongoing macroeconomic uncertainty, customers continued to choose Atlassian products to help their teams organize, discuss, and complete their work, illustrating the mission-critical role our products play in their success.

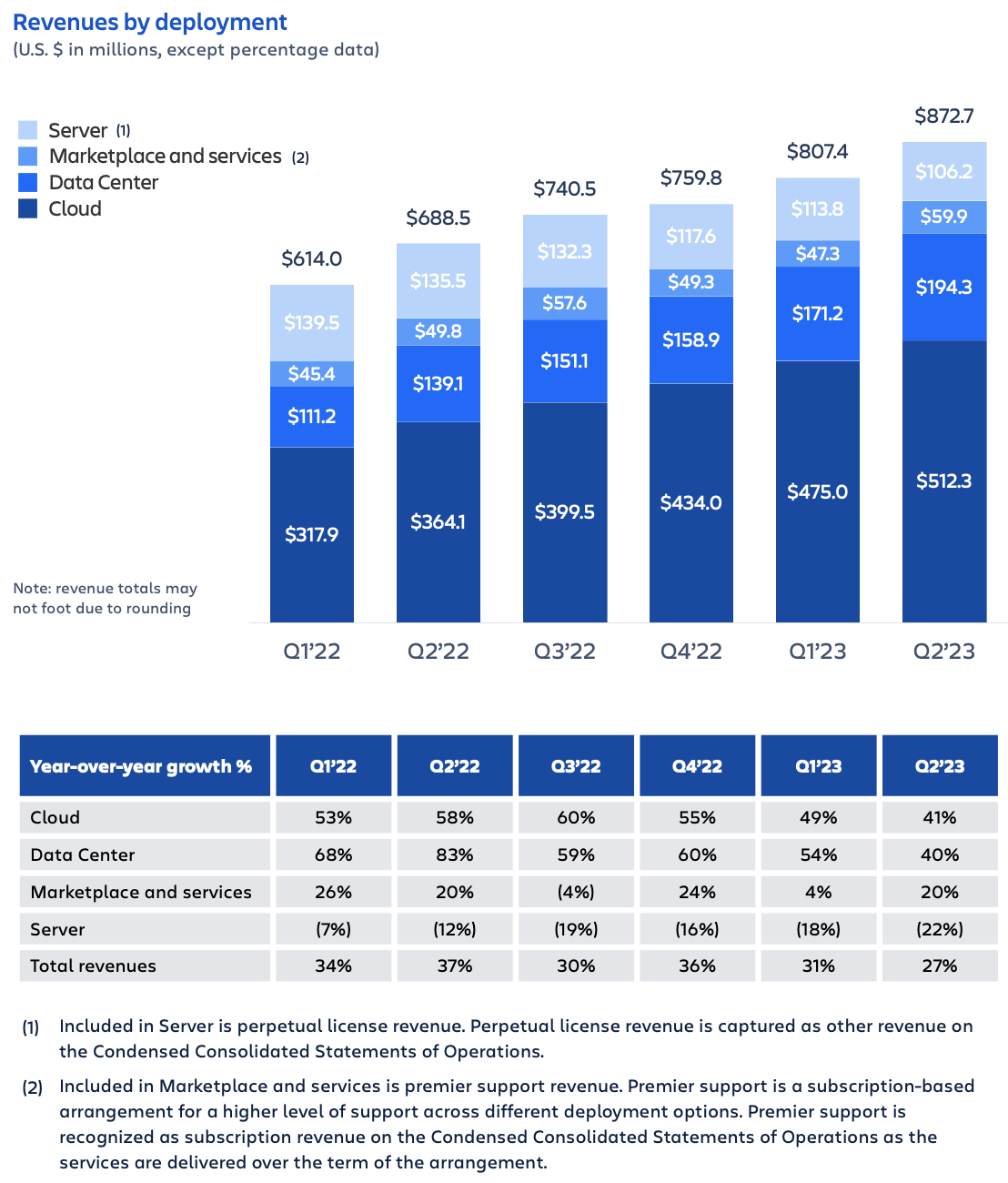

Cloud revenue growth of 41% continued to be impacted by the challenging macroeconomic conditions in the form of moderating growth in 1) paid seat expansion from existing customers and 2) free to paid conversion rates. These headwinds were consistently observed across geographies, industries, and products – and were particularly pronounced in December and in our SMB customer base. Beyond these two areas, we were pleased with the performance in other cloud drivers including monthly active users, seat migrations, dollar-based churn, and upsell to Premium or Enterprise editions, all of which continued to perform in line with our expectations and underscore the value our cloud products deliver to customers and their continued desire to move to our cloud.

Data Center revenue growth of 40% was driven by strong performance of renewals, seat expansion from existing customers, and migrations from Server.

Revenue growth rates across geographic regions were consistent with the exception of the Americas, which grew 23% due to a tough prior year comparable. As a reminder, in Q2’22, the Americas benefited from particularly strong Data Center sales, a portion of which is recognized up-front in the period the subscription begins.

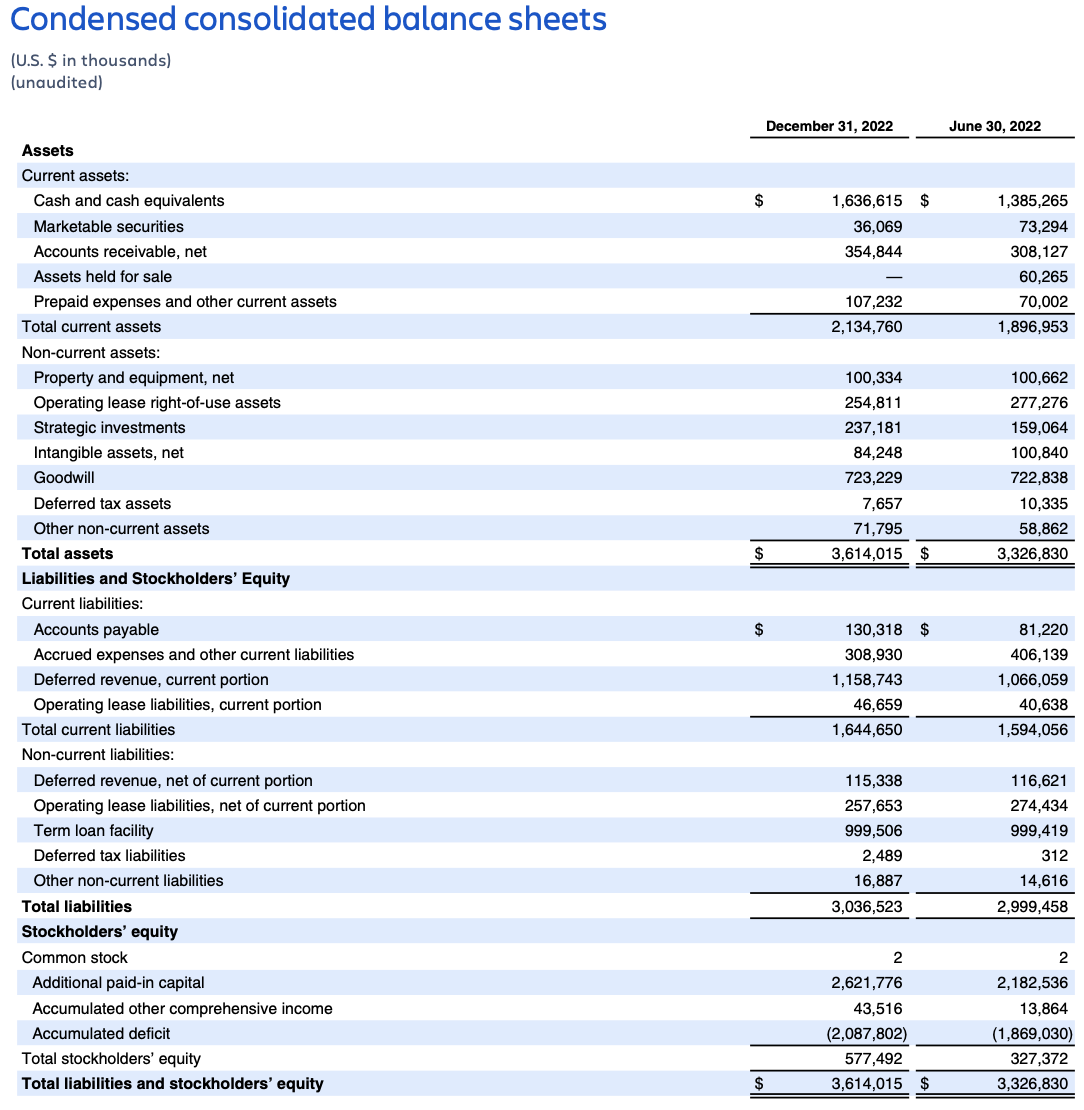

Lastly, deferred revenue increased 31% year-over-year to $1.3 billion driven by growth in annual Cloud subscriptions and multi-year billings, which highlight customer commitment to our platform.

GAAP net loss includes a non-recurring income tax charge of $83 million for Q2’23 for uncertain tax provisions related to transfer pricing. This charge increased GAAP net loss per diluted share by $0.32 in Q2’23.

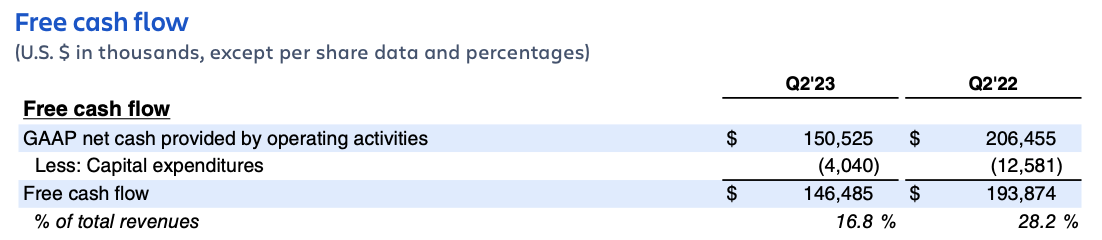

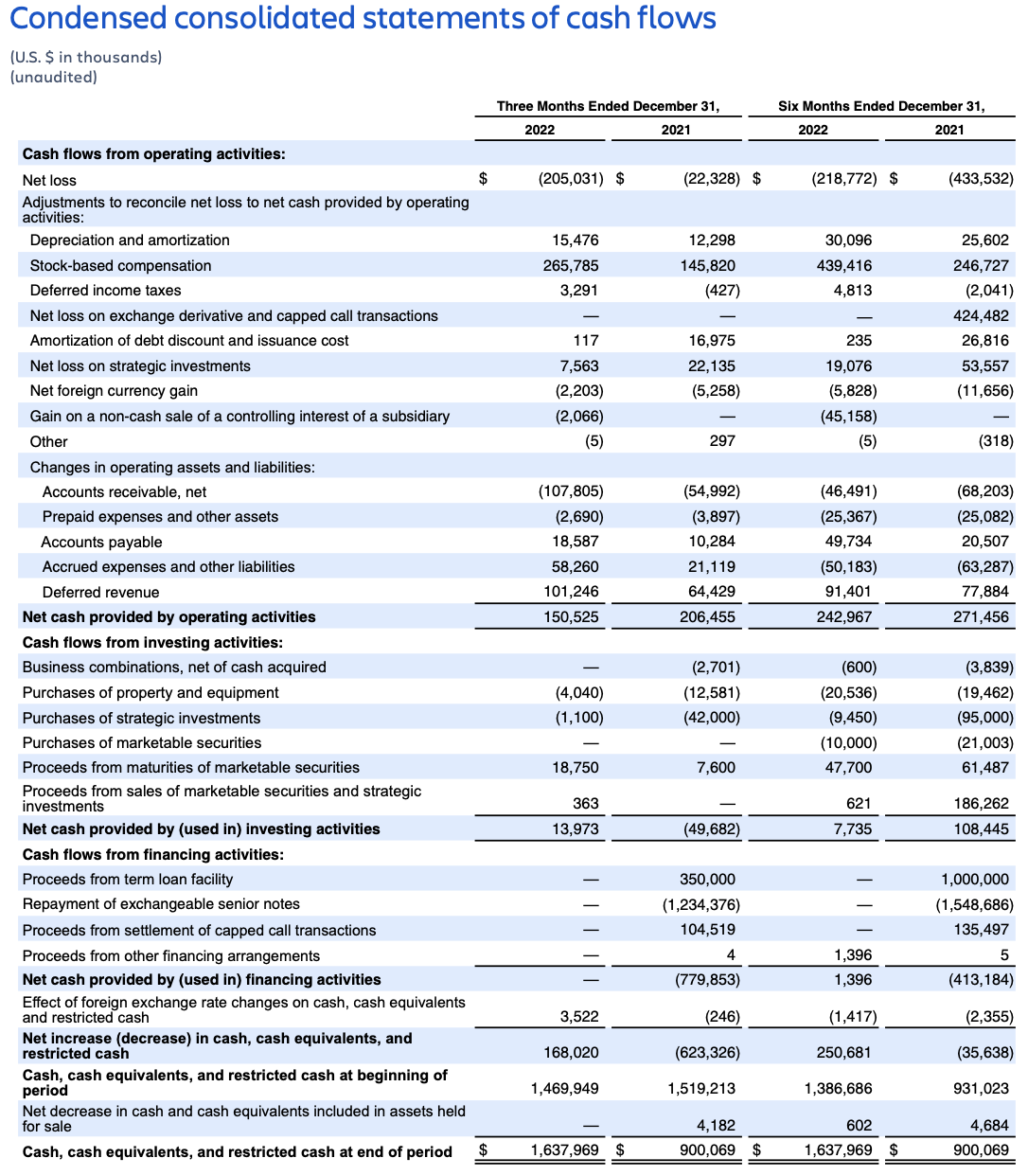

Free cash flow in Q2’23 includes a discrete tax payment of $57 million related to transfer pricing. Excluding this payment, free cash flow would have increased 5% year-over-year to $203 million, and free cash flow margin would have been 23%.

Financial targets

Fiscal 2023 outlook

Total revenue

For FY23, we expect total company revenue growth of approximately 25% year-over-year. This guidance assumes the macroeconomic environment continues to worsen in H2. Further detail provided below:

Subscription revenue – Cloud

We expect FY23 Cloud revenue growth of 35-40% year-over-year, with an increasing macro impact on both paid seat expansion within existing customers and new customer conversions. We continue to expect approximately 10 points of Cloud revenue growth to be driven by migrations. While we have yet to see significant impact in areas like churn or upsell to Premium and Enterprise editions of our products, the lower end of our range contemplates some macro impact in these areas.

Subscription revenue – Data Center

While we continue to see healthy demand for our Data Center products driven by stronger-than-expected renewals and seat expansion from existing customers, we expect Data Center revenue growth rates to moderate in H2.

Subscription revenue – maintenance

In line with our announced Server end-of-life, we expect maintenance revenue to continue to contract over the course of FY23 to approximately $85 million in Q4’23. As a reminder, we will no longer provide maintenance and support for our Server offerings beginning February 2024.

Other revenue

We expect FY23 Other revenue to be approximately flat compared to FY22. The majority of Other revenue is comprised of Marketplace revenue, which we expect to grow in the mid-teens % year-over-year in FY23. Marketplace revenue will be impacted by the ongoing mix shift of third-party app sales from Server and Data Center to Cloud, which has a lower take rate to incentivize cloud app development. We look to drive sales of third-party cloud apps at a rate that exceeds those of our own products. As a reminder, revenue on the sale of third-party Marketplace apps is recognized in the period the product is purchased, which adds quarter-to-quarter volatility in Marketplace growth rates. As a reminder, perpetual license revenue, which is reflected in Other revenue, will be $0 in FY23 and totaled approximately $30 million in FY22.

Operating margin

We expect FY23 GAAP operating margin will be approximately (11%) and non-GAAP operating margin will be approximately 17%. Despite the uncertainties in the macroeconomic environment, we continue to have strong conviction in the long-term opportunities in front of us and will continue to play offense. In terms of costs, we will invest to drive long-term growth in the business while being responsive to macroeconomic changes. We continue to expect operating expense growth to decelerate in H2 as we follow through on our previously announced plans from last quarter to reduce discretionary non-headcount related spending and moderate the pace of headcount growth.

Share count

In FY23, we expect less than 2% year-over-year increase in diluted share count.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward looking, including risks and uncertainties related to statements about our products, customers, Cloud migrations, macroeconomic environment, anticipated growth, outlook, technology, share repurchase program, and other key strategic areas, and our financial targets such as revenue and GAAP and non-GAAP financial measures including gross margin and operating margin.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the “SEC”) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 20-F and 10-Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at: https:// investors.atlassian.com.

ABOUT NON-GAAP FINANCIAL MEASURES

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit, non-GAAP operating income, non-GAAP net income, non-GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled non-GAAP measures used by other companies, provide supplemental information regarding our operating performance on a non-GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

Non-GAAP gross profit. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets. Non-GAAP operating income. Excludes expenses related to stock-based compensation and amortization of acquired intangible assets.

Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, non-coupon impact related to exchangeable senior notes and capped calls, gain on a non-cash sale of a controlling interest of a subsidiary and the related income tax effects on these items, and a non-recurring income tax adjustment.

Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our agile & DevOps, IT service management and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 250,000 companies of all sizes worldwide – including NASA, Kiva, Deutsche Bank, and Salesforce – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira Software, Confluence, Jira Service Management, Trello, Bitbucket, and Jira Align at https://atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com Media contact: M-C Maple, press@atlassian.com

1Gartner, Magic Quadrant for IT Service Management Platforms, Rich Doheny, Chris Matchett, Siddharth Shetty, 31 October 2022.

2Gartner, A Buyer’s Guide to ITSM Platforms, Chris Matchett, Rich Doheny, 4 August 2022.

Gartner Disclaimer

Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner research organization and should not be construed as statements of fact. Gartner disclaims all warranties, express or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

Gartner Peer Insights Customers’ Choice constitute the subjective opinions of individual end-user reviews, ratings, and data applied against a documented methodology; they neither represent the views of, nor constitute an endorsement by, Gartner or its affiliates.

GARTNER and MAGIC QUADRANT are a registered trademark and service mark, and PEER INSIGHTS is a trademark and service mark, of Gartner, Inc. and/or its affiliates in the U.S. and internationally and are used herein with permission. All rights reserved.