From the CEO

From the CEO

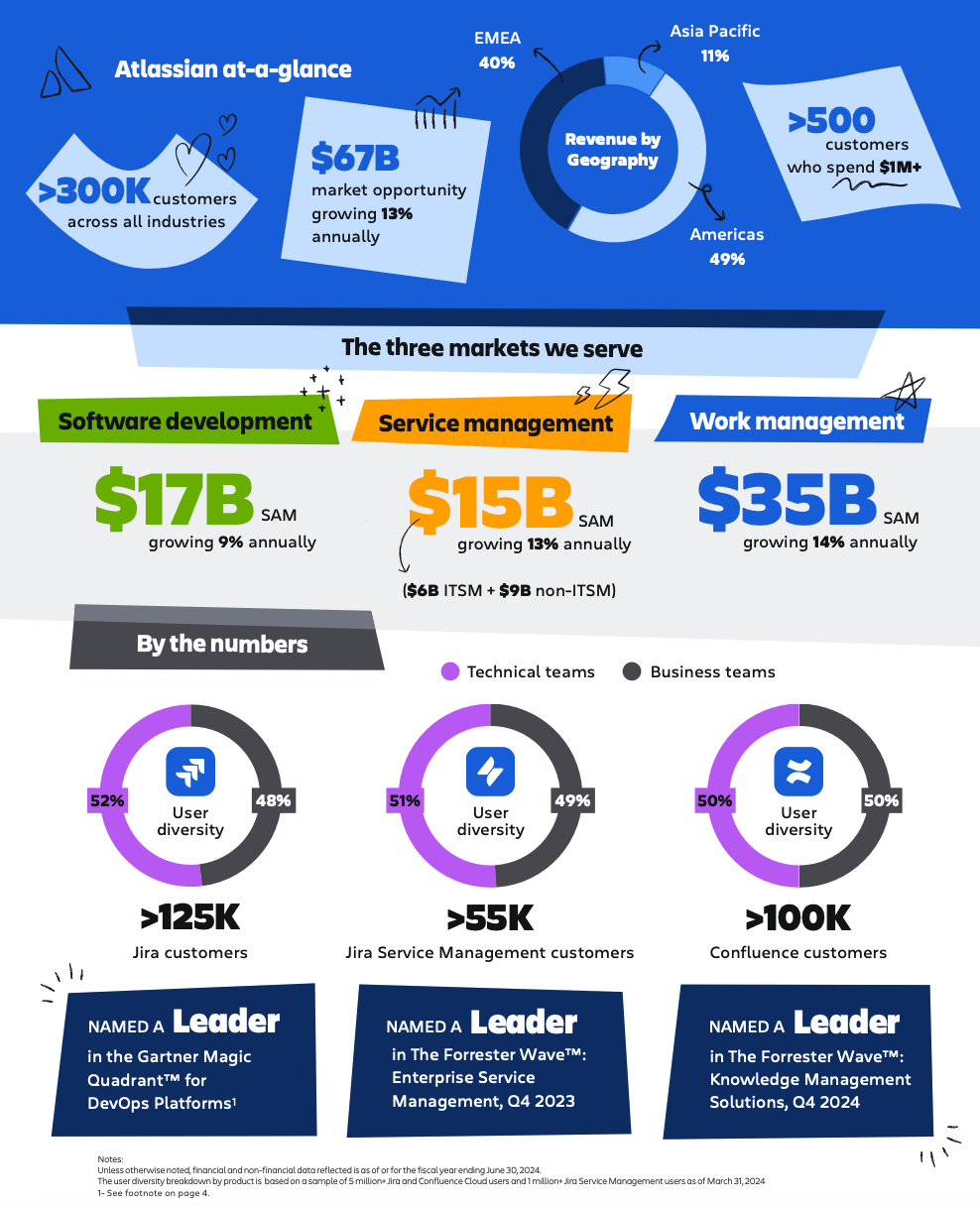

We closed out Q2 with a real sense of momentum across Atlassian. Our long-term strategy, investments, and hard work are paying off. We’ve built a world-class platform that serves over 300,000 customers, driving work forward for teams of 10 to 100,000+ people within the largest enterprises across the globe.

This strong foundation allows us to quickly deliver innovative new products and unique capabilities to our customers’ software, IT, and business teams. Customers are recognizing this value, and committing further to the Atlassian platform. They’re bringing our solutions to more teams across their organizations and adopting more of our offerings to solve their collaboration challenges. We’ve now scaled past $5 billion in annual run-rate revenue, powered by subscription revenue which grew 30% year-over-year in Q2.

I continue to meet with scores of CIOs and CEOs each month, and in every conversation I have, the Atlassian System of Work is resonating. They live and breathe the problems we seek to address: to bridge the gap between technology and business teams. Our customers see technology as their biggest source of differentiation in the current competitive landscape. They all want the same thing: a platform that helps all teams collaborate across the organizations on the problems, challenges and opportunities they face. Atlassian is uniquely positioned to deliver this because of the breadth of our offering, our pace of innovation, and the recognition of our product leadership across markets.

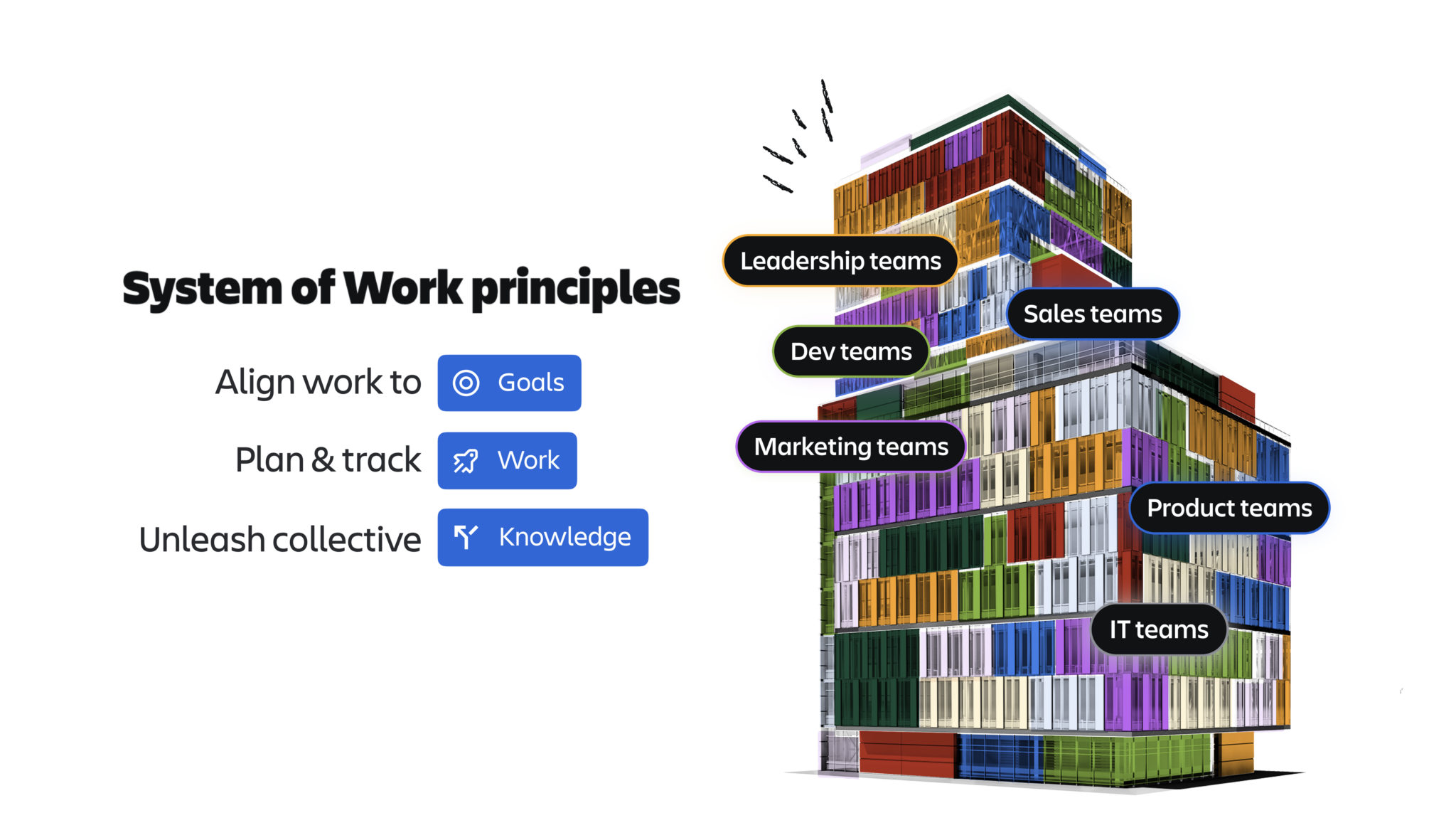

Our System of Work is a philosophy of how technology-driven organizations should work, connecting technology and business teams to accelerate progress and maximize team impact.

Our powerful platform, paired with our R&D muscle, allows us to innovate at scale to deliver increased value for thousands of enterprises and expand our addressable opportunities. The rapid evolution of AI means those software vendors without a unified platform will fall behind. Flashy marketing is no longer enough. To be a true technology partner, it requires the investment, the talent and capability, the infrastructure and the data to help customers break down knowledge silos across teams and tools. It’s not only helping customers keep their car on the track but also making sure those in the driver’s seat feel confident to get to a podium finish time on every lap.

There’s much more to do, but I’m incredibly bullish about our ability to capitalize on this momentum and increasing customer demand. And with Brian Duffy, our new Chief Revenue Officer, joining the team, we’ll continue to evolve our go-to-market approach in how we sell to and support our largest customers. Within our walls, there is a real sense of excitement. We’re leaning even harder into our top priorities: the System of Work, Enterprise, and AI. The opportunity is ours for the taking. We aren’t taking our foot off the gas—quite the opposite.

This momentum only makes us hungry for more.

Atlassian + Udemy

Udemy, an education technology company, is accelerating collaboration across its technology and business teams with the power of the Atlassian Cloud and System of Work, saving them an estimated 2,400 hours of meeting times each year.

“Using Atlassian is paying dividends with time and clarity…Before we had to attend a bunch of meetings, Slack many people, or read through several channels. Now you can go into Atlassian as your one-stop shop and find whatever you need.”

– Shawn Kresal Senior Director, Technical Program Management and Chief of Staff, CTO, Udemy

“Having a central place for everyone to get information, draft content, and get feedback has been invaluable. We can interact with our product teams through Jira, but even if you don’t have access, you can still see what you need with Jira filters and dashboards that pull through to Confluence. That’s been huge for improving visibility and driving accountability.”

– Genefa Murphy, PhD, Chief Marketing Officer, Udemy

Products Supercharging our System of Work

Products Supercharging our System of Work

Our investment in building a world-class platform allows us to ship innovation at the velocity and quality we do today. The Atlassian platform, combined with our continual product investment and opinionated System of Work, differentiates us as a strategic partner. Jira and Confluence continue to deliver durable growth, fueled by their ability to serve all teams and provide the teamwork foundation so they can plan and track work, align on goals, and unleash knowledge consistently. And we continue to broaden the offerings in the Atlassian portfolio to solve the unique challenges facing different teams.

The strength of our entire portfolio of products is demonstrated by accolades across every sandpit we play in:

For software teams:

- Atlassian has been named a Leader in the Gartner® Magic Quadrant™ for DevOps Platforms1 two years in a row.

For IT teams:

- Atlassian was named a Leader with the highest possible score in the strategy category in The Forrester Wave™: Enterprise Service Management, Q4 2023.

- Atlassian was named a Leader in the IDC MarketScape: Worldwide IT Service Management Software 2024 Vendor Assessment. The report noted, “In 2023, growth for Jira Service Management was well over the average for the IT service management market, according to IDC data.”

Today, over 40% of Fortune 500 companies are Jira Service Management customers, but we still have tons of runway within the walls of these organizations.

Now for business teams, we’re proud to note:

- Atlassian has been named a Leader in The Forrester Wave™: Knowledge Management Solutions, Q4 2024 – the first Wave in this market.

- Atlassian has been named a Leader in the 2024 Gartner Magic Quadrant™ for Marketing Work Management Platforms2.

Atlassian’s model is fundamentally differentiated by our investment in R&D, which delivers the best products at incredibly competitive prices to our customers. This means we invest more of our money into the areas that directly benefit customers. These accolades show that 24 years on, we are still building world-class products as a result of this investment. We launched Jira Product Discovery to general availability in Q4’23 – and today, it’s growing more than 150% year-over-year and amassed over 14,000 customers. This quarter, we added a Premium edition for customers who need advanced capabilities.

This quarter also marks one year since Loom joined Atlassian, with customers recording over 88 million videos in 2024, reducing the need for an estimated 200+ million meetings. Thirty-eight million of these videos used Loom AI to boost their team collaboration. Features like auto-generated titles and summaries and the ability to remove filler words and silences help our customers communicate asynchronously better than ever before. Today, Loom is more deeply connected across the Atlassian platform, as integrations with Jira and Confluence are supercharging customer productivity by doubling the number of hours saved on tasks related to onboarding and getting up to speed.

There are countless use cases for Loom. For example, we know that when Loom is used as a tool by go-to-market teams, sales win rates are 20% higher than without it. With Loom, sales teams can better reach decision-makers, answer buyer questions, and share proposals faster with async video.

ATLASSIAN + REMOTE

“I use Loom to explain sales strategies and products to partners through video. It’s great for quick internal communications, upskilling, and clarifying complex processes to customers.”

– Fiona Mackie, Sr Solutions Consultant

“Async work is how high-performing teams get more done with fewer interruptions, higher efficiency, and greater reliability,”

– Marcelo Lebre, President and Co-Founder

And for distributed teams, Loom is a game-changer. It allows teams to communicate in more human ways while saving hours of meeting time. Remote, a global HR platform company, estimates it has saved over 20,000 hours of meetings in the last two years, with over 1.3 million minutes of Looms watched across 1,500 employees in over 75 countries.

Excelling in the Enterprise

Excelling in the Enterprise

The biggest enterprises in the world are turning to Atlassian to help them address their collaboration challenges. The common thread across these conversations is that customers want a deeper relationship, and they view Atlassian as a trusted and strategic partner to help accelerate their growth. We know the appetite is there. We see an $18 billion annual revenue opportunity just within our existing customer base of over 300,000, with $14 billion in our existing enterprise base alone.

Enterprises are recognizing the incredible innovation and differentiated value across the Atlassian platform, which, combined with strong sales execution, led to some massive customer wins in Q2. One of the world’s largest technology companies, a major telecommunications company, and one of the largest global banks all committed to the Atlassian Cloud to bridge the gap between their technology and business teams. And customers, like one of the largest U.S. automotive companies, one of the world’s leading online travel platforms, and a large government-owned bank embraced the Atlassian System of Work by consolidating from other vendors and expanding their Atlassian footprint by adopting multiple new cloud products.

In Q2, we closed a record number of deals greater than $1 million in annual contract value. The progress we are making in the enterprise customer segment underscores the massive opportunities that lay ahead as we strengthen our go-to-market motion for an enterprise audience. While 85% of the Fortune 500 are Atlassian customers, they represent merely 10% of our total business. To capture this enterprise opportunity and scale to $10 billion in revenue and beyond, we will look to up-level brand investment to capture more mindshare with C-level decision-makers. This includes entering into more partnerships to drive brand awareness and reinforce Atlassian as the teamwork company.

We’re also doing more to support our largest enterprises on their journey to the cloud. You’ll see us continue to expand strategic partnerships, like with Amazon Web Services (AWS), to streamline complex migrations. And to unlock the enterprise opportunity, we need to meet the requirements of the largest and most complex customers.

Today, we’re able to help customers with tens and even hundreds of thousands of employees break down silos and collaborate more effectively, with Confluence Cloud now supporting up to 150,000 users on a single site – a 3x increase in scale. Large enterprises can now bring more of their teams onto one Confluence site and use it as a single source of truth for seamless, centralized knowledge sharing and company-wide collaboration.

We are also one step closer to achieving FedRAMP® Moderate Authority to Operate after successfully completing the required third-party security assessment and formal review with our sponsoring agency. This demonstrates that our offering meets the agency’s extensive FedRAMP Moderate security, compliance, and usability requirements. As part of the next and final step in the process, we await the FedRAMP Program Management Office (PMO)’s review of the security assessment materials and update of our marketplace listing to “Authorized.”

The progress we’re making sets us up in good stead to support more of the world’s largest enterprises. We need to make even bigger strides to get where we want to be, but we’re ready to put in the hard yards.

AI & the Future of Teamwork

AI & the Future of Teamwork

Since we launched Rovo into General Availability last quarter, more customers are realizing the value of our powerful AI capabilities and see them as big reasons to adopt our cloud offerings. Rovo, combined with our 50+ and growing Atlassian Intelligence capabilities infused throughout our products, is driving over 1 million monthly active users (MAU) of AI across our platform, and the number of AI interactions has increased over 25x year-over-year. We are seeing an increasing number of customers adopt higher-value editions of our cloud products to take advantage of AI, which – along with analytics and automation – is driving sales of our Premium and Enterprise editions up over 40% year-over-year.

This is a signal that our thoughtful approach to AI is paying off. We’ve been able to ship incredible AI innovation into the hands of our customers quickly due to our major competitive differentiators:

- Our 20+ years of data supporting our Teamwork Graph means customers can access their first and third-party data of how their teams plan and track work, set goals, and unleash knowledge. The investments we’ve made in building a world-class platform underpin this, and in the AI era, it’s paying off in spades.

- Our R&D engine means we can build and ship fast. We aren’t just marketing AI; we’re delivering real features and benefits that thousands of customers are using today. The AI landscape calls for the ability to innovate quickly to meet changing needs, something we believe we’re in the best position to do.

ℹ Our AI strategy has been built on a belief in multiple models from day one. We believe the industry will go through a verdant explosion of new, cheaper, smaller foundation models. As such, our R&D investment is directed towards building our AI gateway to rapidly test, deploy, and productionize multiple models from multiple providers.

This strategic approach allows us to swiftly realize the benefits of improvements in performance and costs of foundational models. In turn, we pass these benefits to our customers through results that are higher quality, faster, and lower cost. Recent developments have shown this strategy is paying off.

For Atlassian, AI capabilities are the cream that layers on top of an already strong platform and incredibly loyal and growing customer base. AI is helping to grow our top-of-funnel with the lure of exciting AI innovations being shipped at a regular clip. Air France-KLM migrated to cloud to take advantage of our latest innovations, including AI:

ATLASSIAN + AIR FRANCE-KLM

“Migrating to Atlassian cloud was best for our community. We had a vision of supporting users with the most up-to-date versions, features and functionalities only available on cloud, like AI.”

– Jordy Essed, DevNet Team Product Owner, Air France-KLM

By migrating to cloud, Air France-KLM has realized $600K of annual savings, and eliminated 48 hours of downtime a month thanks to continuous cloud updates versus running backups on Data Center. As IT invested in creating a system of work to connect Air France-KLM’s teams, more employees have adopted Atlassian tools. Over 20 technical and business teams, from Flight Operations to HR, now collaborate on the Atlassian cloud platform, with teams gaining back an estimated 2,500 hours each day.

ATLASSIAN + AIR FRANCE-KLM

“Other teams often come to us, asking to upgrade to Atlassian cloud because they see how it could improve their life and deliver a better experience. Now, we have more non-developer users on Atlassian than developers.”

– Nathan Wattimena, Scrum Master – RTE Next Generation Data Center, Air France-KLM

TBC Bank is another customer that has seen major value since implementing Atlassian Intelligence:

ATLASSIAN + TBC BANK

“Overall, we estimate that TBC Bank has boosted our efficiency by about 25% with Atlassian Intelligence, enabling our teams to focus more on high-impact work, better allocate resources, and accelerate project delivery.”

– Nika Melikidze, SDLC Automation Expert, TBC Bank

“Atlassian Intelligence has helped TBC Bank save time, improve accuracy and consistency across our processes, and increase efficiency as we manage IT governance and compliance.” – Giorgi Tsitskishvili, IT Governance Lead, TBC Bank

We see AI capabilities as core to our offerings, helping teams in every corner of an organization push work forward. We’ll have more to share as we approach our flagship customer event, Team ‘25. For now, we’re stoked with the progress we’re seeing.

Next Phase of Growth

Next Phase of Growth

It would be remiss to close out this shareholder letter without mentioning another accolade that’s going straight to the pool room. We’re chuffed to be named #1 on Fortune’s “The Future 50” list, which recognizes companies best positioned to grow in an ever-changing environment. Adapting, thriving, and growing have been our mindset since day one, and this recognition is a testament to our people-first culture of flexibility, collaboration, and innovation.

We’re looking ahead to our next phase of growth and are already playing offense to capture the huge market opportunity in front of us.

There’s still much to do, but we’re fueled up for the road ahead. We continue to be hungry. It’s a good place to be.

– Mike

Financial Highlights

Second quarter fiscal year 2025 financial summary

(U.S. $ in thousands, except per share data and percentages)

Second quarter fiscal year 2025 highlights

We closed out the first half of our fiscal year with steady progress and good momentum across our strategic priorities of Enterprise, AI, and System of Work.

Strong enterprise execution from our sales teams and partners combined with disciplined cost management drove revenue, gross profit, and operating income ahead of our expectations. We delivered healthy revenue growth across all deployments, customer segments, and markets while continuing to invest in our ability to deliver differentiated customer value and durable long-term growth.

As we look to the second half of the year, our focus remains on our execution in helping customers solve their most complex collaboration challenges by expanding our capabilities to serve enterprise customers, shipping innovative AI products and features, and delivering solutions that bridge the gap between technical and business teams.

Highlights for Q2’25 include:

All growth comparisons below relate to the corresponding period of last year, unless otherwise noted.

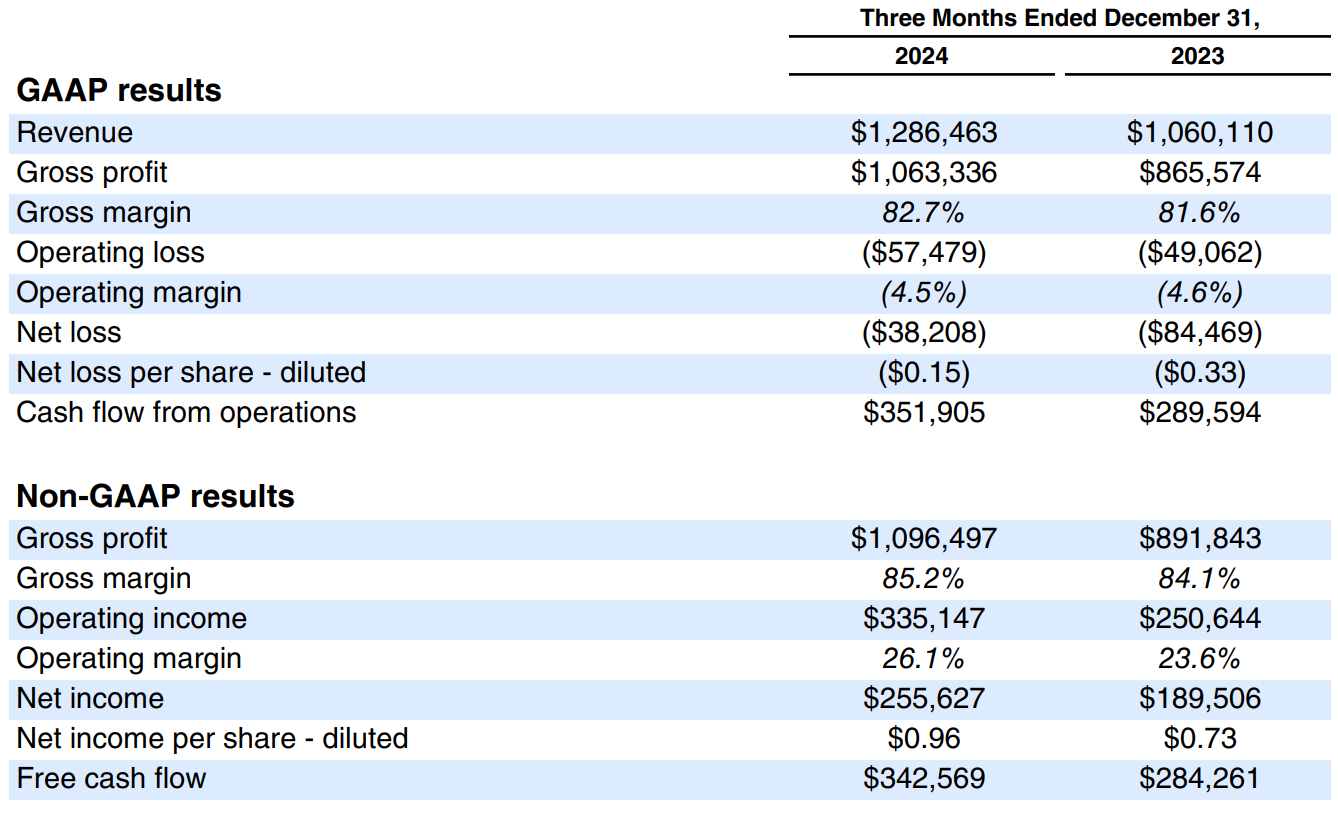

- Revenue of $1.3 billion increased 21%, driven by growth in our Cloud and Data Center offerings, partially offset by the cessation of Server maintenance revenue following its end-of-support (EoS) in Q3’24.

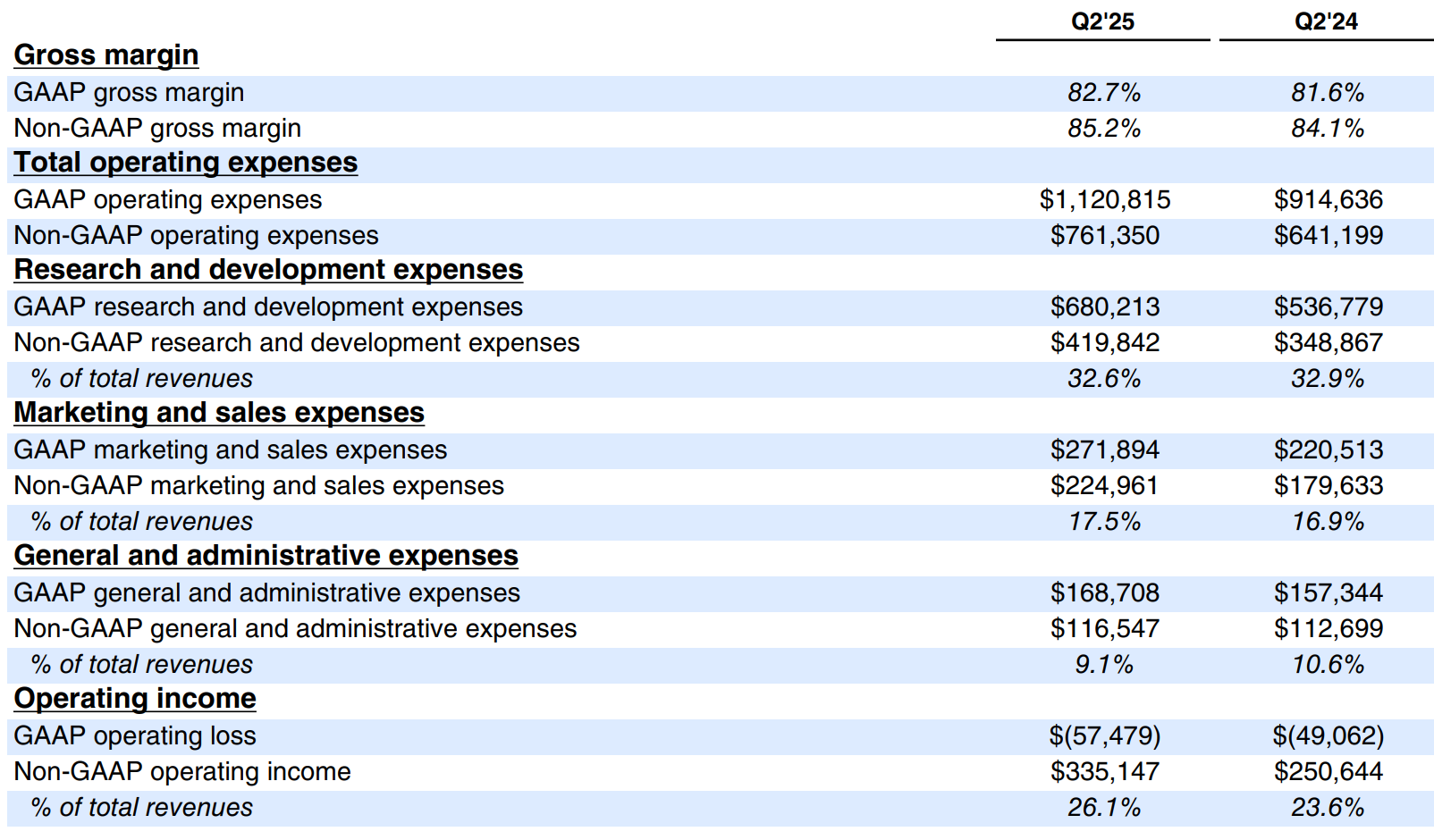

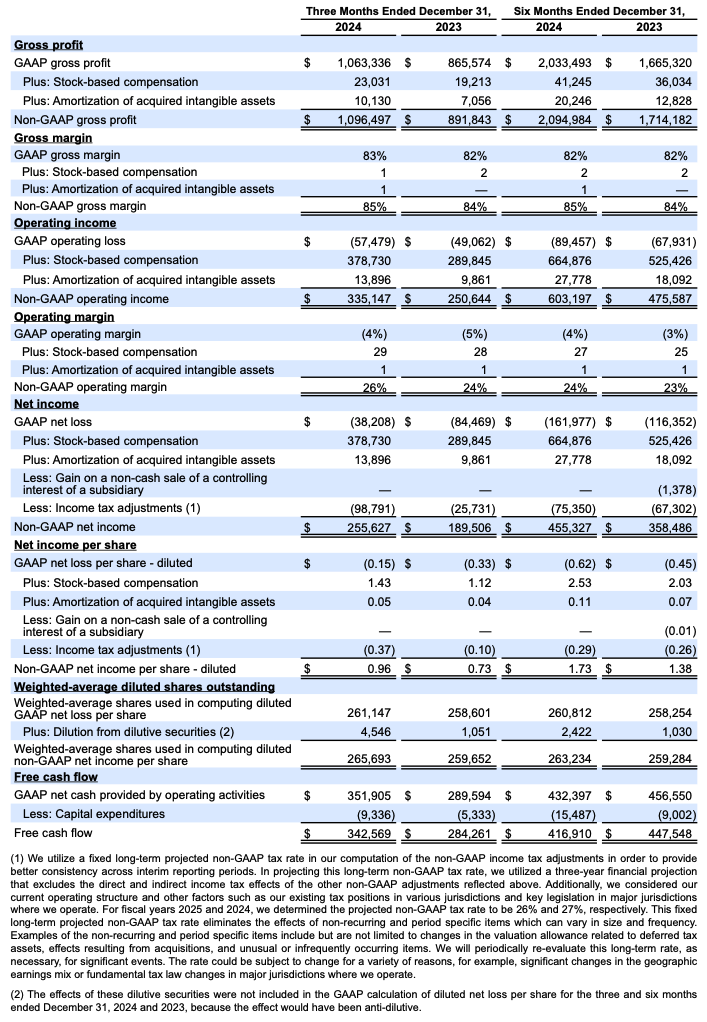

- GAAP gross margin of 83% and non-GAAP gross margin of 85% increased one percentage point driven by higher Cloud gross margin.

- GAAP operating loss was $57 million, and GAAP operating margin of (4%) was flat. Non-GAAP operating income was $335 million and non-GAAP operating margin of 26% increased two percentage points driven by greater operating leverage and the increase in gross margin.

- Operating cash flow of $352 million increased 22% driven primarily by growth in collections. Free cash flow of $343 million increased 21%.

Revenue

(U.S. $ in thousands, except percentage data)

Revenue growth in Q2 was driven by subscription revenue, which grew 30%.

Cloud revenue growth of 30% was driven by paid seat expansion within existing customers, migrations, cross-sell of additional products, and higher average revenue per user (ARPU). Overall, trends in the quarter were consistent with Q1’25. Paid seat expansion and migrations exceeded our expectations, while cross-sell, adoption of higher-value editions, top-of-funnel performance, and customer retention were in line to slightly ahead of our expectations.

Data Center revenue growth of 32% was driven by price increases, seat expansion in existing customers, and the benefit from prior-year Server migrations, partially offset by continued migrations to Cloud. Stronger-than-expected renewals and large, multi-year deals drove the outperformance to our expectations.

Marketplace and other revenue growth of 23% was driven by continued momentum in third-party app purchasing related to the Cloud and Data Center billings in the quarter.

Lastly, deferred revenue increased 33% year-over-year to $2.2 billion driven by continued growth in annual and multi-year agreements, including a record number of deals greater than $1 million in annual contract value.

Margins, operating expenses, and operating income (loss)

(U.S. $ in thousands, except percentage data)

GAAP operating expenses increased 23% year-over-year driven by higher employment costs, including stock-based compensation expenses. Headcount at the end of Q2’25 was 12,750, an increase of 249 from the prior quarter, primarily driven by hiring in sales as we continue to evolve the way we sell to and support our largest enterprise customers.

Non-GAAP operating expenses increased 19% year-over-year and were lower-than-expected driven primarily by timing of discretionary spending, lower employment expenses, and favorable foreign exchange rate movement within the quarter.

GAAP operating margin of (4%) and non-GAAP operating margin of 26% exceeded our expectations driven by better-than-expected operating leverage and gross margin.

Net income (loss)

(U.S. $ in thousands, except per share data)

Free Cash Flow

(U.S. $ in thousands, except percentage data)

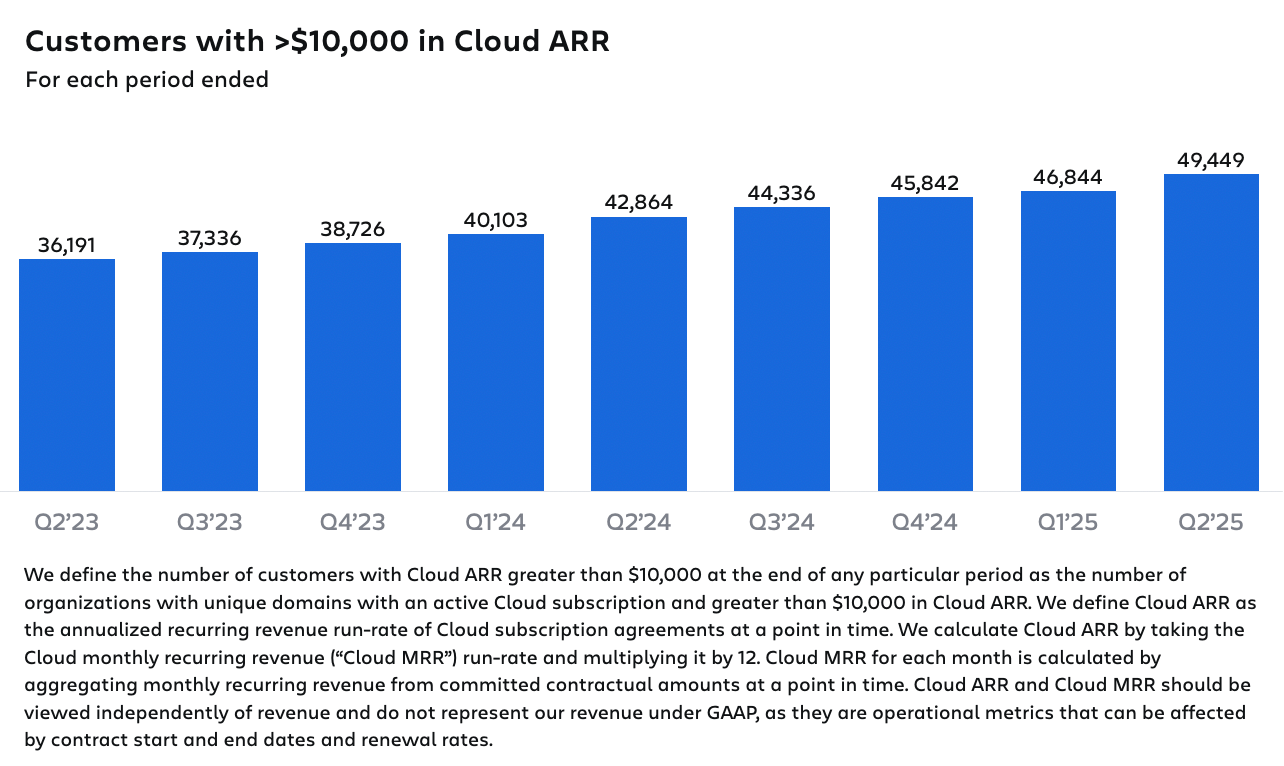

Customers with >$10,000 in Cloud ARR

We ended Q2’25 with 49,449 customers with greater than $10,000 in Cloud annualized recurring revenue (Cloud ARR), an increase of 15% year-over-year. We continue to increase scalability across our cloud platform as we delivered support for up to 150,000 users on a single site in Confluence and added support for 100,000 users on a single site in Jira to our public cloud roadmap. Additionally, we have entered the final stage in the process of achieving FedRAMP Moderate, which is another big step in unlocking the Atlassian cloud for many of our largest, most complex customers.

Financial targets (U.S. $)

Q3’25

FY25

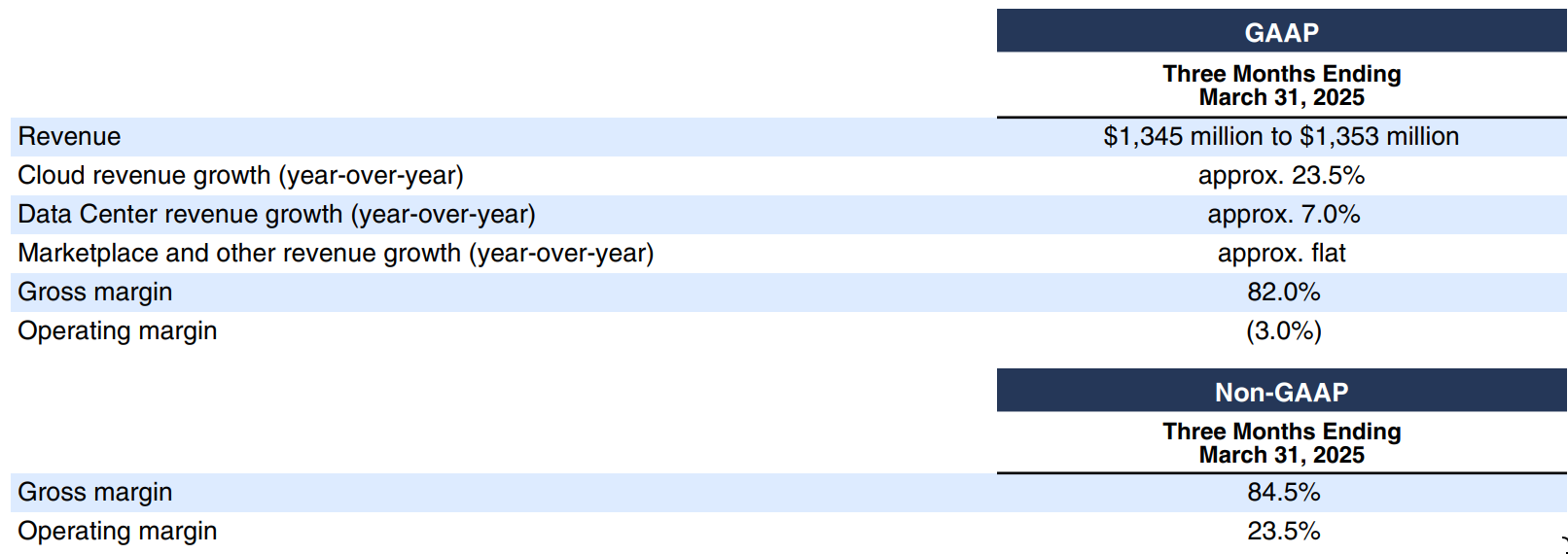

FY25 Outlook

Total Revenue

Given our strong billings and revenue performance in Q2, we have increased our FY25 total company revenue growth outlook to be in the range of 18.5% to 19.0%. In setting our outlook we continue to take what we believe is a prudent and risk-adjusted approach based on two primary factors.

First, given uncertainty in the macroeconomic environment, our guidance contemplates macro-related factors that negatively impact key revenue growth drivers such as paid seat expansion, cross-sell, upsell, and customer retention.

Second, our outlook continues to allow for execution risk and potential business disruption in the ongoing evolution of our enterprise go-to-market motion.

Additionally, as a reminder, we will be lapping the impacts of Server EoS that benefited revenue in FY24. These dynamics create challenging year-on-year comparisons in FY25 in three primary areas:

- event-driven Data Center and Marketplace outperformance in Q3’24

- the roll-off of FY24 Server migration benefits in both Data Center and Cloud

- the cessation of Server maintenance revenue

Further detail and expected trends are provided below:

Cloud revenue

With our strong performance in Q2, we have increased our outlook for Cloud revenue growth to approximately 26.5% year-over-year in FY25.

We continue to maintain a conservative and risk-adjusted approach to our Cloud guidance for the second half of the year due to the factors described above.

Also, while we executed well on Data Center to Cloud migrations in the first half of the year, we continue to expect migrations to drive a mid-single-digit contribution to Cloud revenue growth for the full year. Our view remains that Data Center customers will migrate over a multi-year period as we strengthen our enterprise-grade Cloud platform, deliver differentiated value like AI, and evolve our enterprise go-to-market sales motion. We also expect customers to increasingly adopt hybrid deployment strategies, allowing them to migrate users to the cloud over time.

In terms of seasonality, we expect Cloud revenue growth rates to decelerate in the second half of the year as we lap the impact of the Loom acquisition and the Server EoS-driven purchasing described above.

Data Center revenue

We expect Data Center revenue growth of approximately 21.5% year-over-year in FY25 driven by price increases, seat expansion within existing customers, and cross-sell of additional products.

We expect growth to decelerate in the second half of the year, with Q3 facing the most challenging prior year comparison, as we lap the event-driven purchasing from Server EoS in FY24 and drive migrations to the cloud.

Marketplace and other revenue

We expect Marketplace and other revenue to grow approximately 8.5% year-over-year in FY25. The deceleration in growth from FY24 is driven primarily by the challenging prior-year comparison related to the event-driven purchasing from Server EoS, as well as continued sales mix shift to Cloud apps, which currently have a lower take-rate relative to Data Center apps to incentivize Cloud app development.

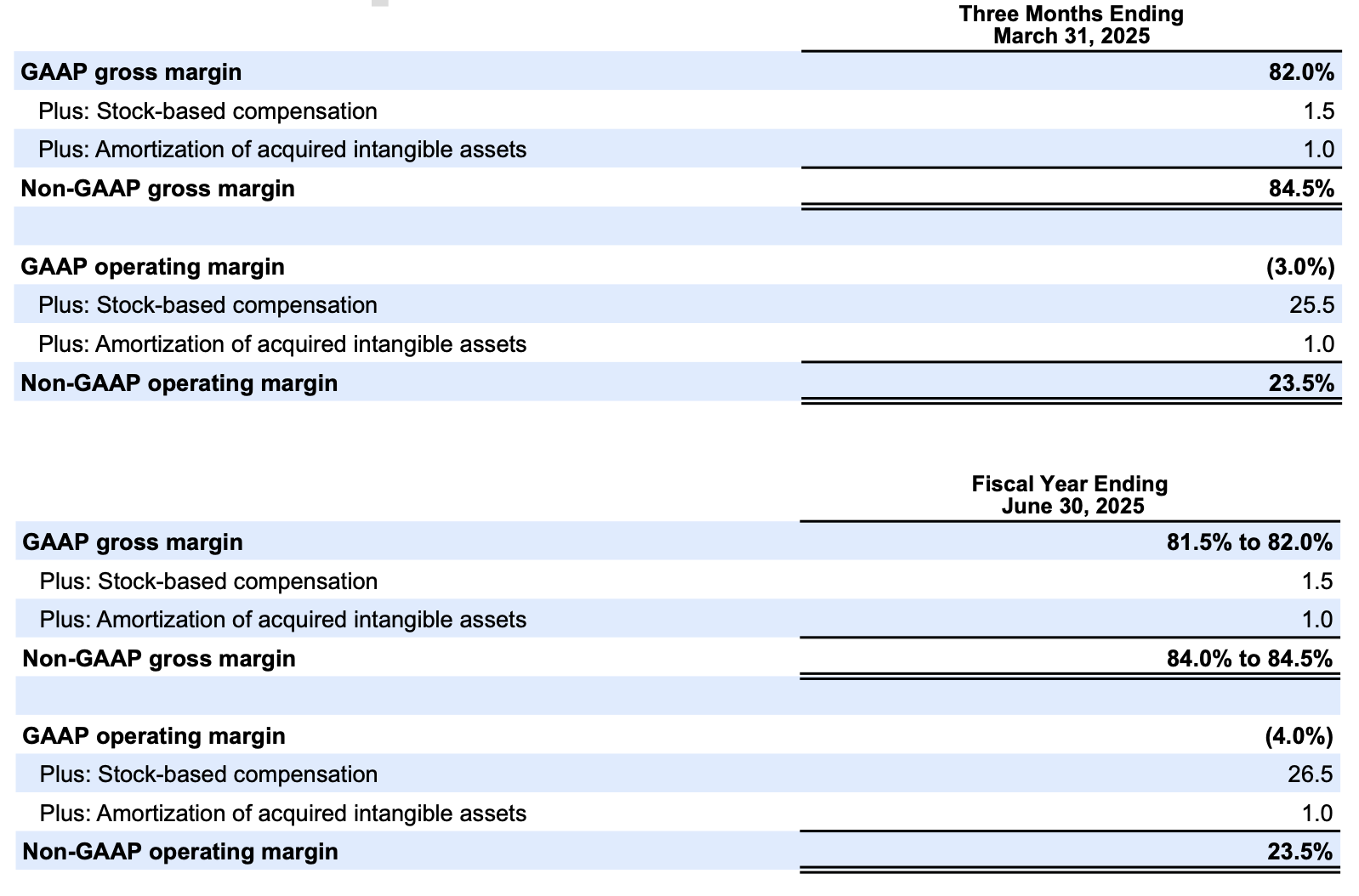

Gross margin

We expect GAAP gross margin to be in the range of 81.5% to 82.0% and non-GAAP gross margin to be in the range of 84.0% to 84.5% in FY25. Our guidance assumes improvements in cloud gross margin will offset the negative impact of revenue mix shift to cloud.

Operating margin

We expect GAAP operating margin to be approximately (4.0%) and non-GAAP operating margin to be approximately 23.5% in FY25.

Operating expense growth for the year will be driven by our continued investments in R&D and sales and marketing to support our strategic priorities of Enterprise, AI, and System of Work, partially offset by continued efficiency in G&A as we scale. Our guidance for the second half of the year reflects two dynamics. First, the timing of discretionary spending that shifted from Q2 into the second half of the year. Second, with the strong performance and momentum we have in the enterprise customer segment, we are slightly increasing investment in that area to further strengthen our market position and accelerate the value we deliver to these customers.

With the updated guidance for both revenue and expenses, we now expect full-year operating margins in FY25 to be slightly higher than FY24.

SHARECOUNT

We expect diluted share count to increase by approximately 2% in FY25.

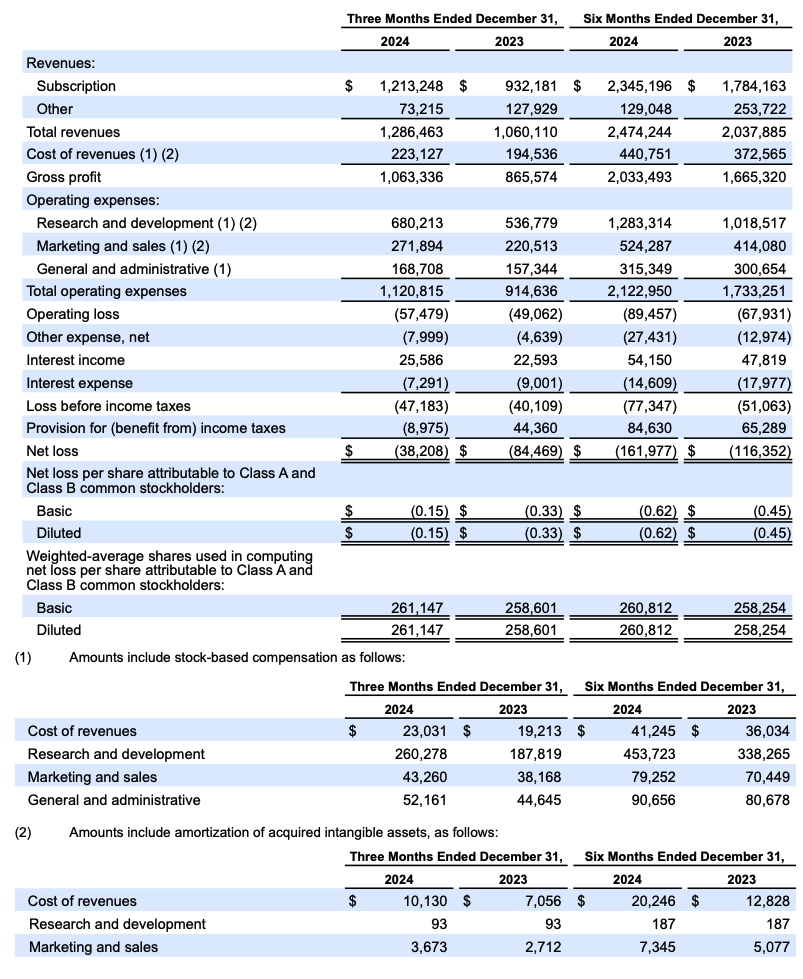

Condensed consolidated statements of operations

(U.S. $ and shares in thousands, except per share data)

(unaudited)

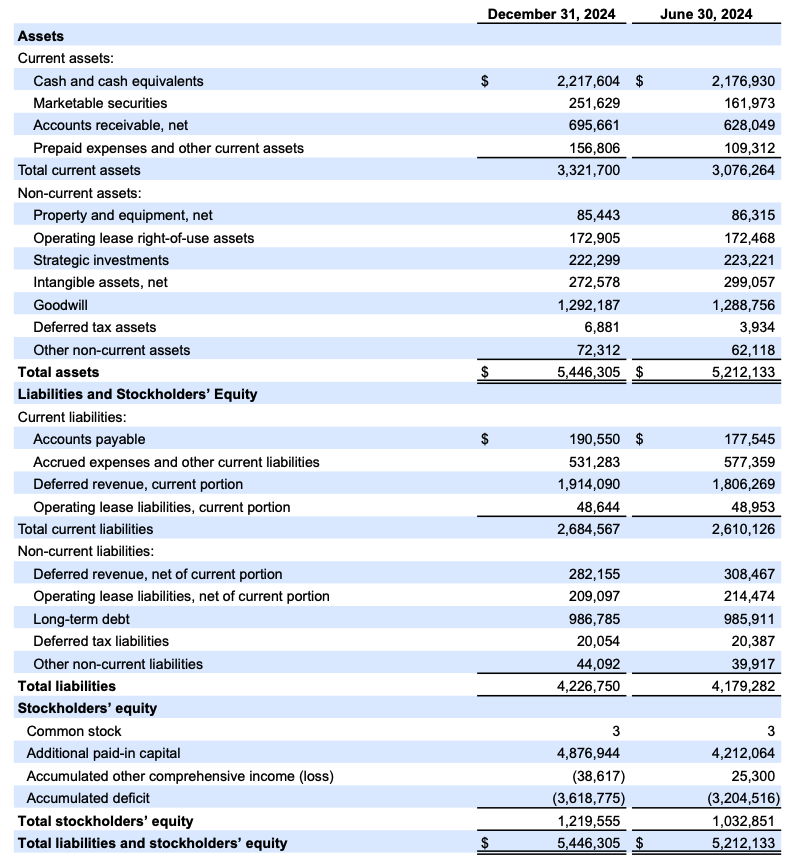

Condensed consolidated balance sheets

(U.S. $ in thousands)

(unaudited)

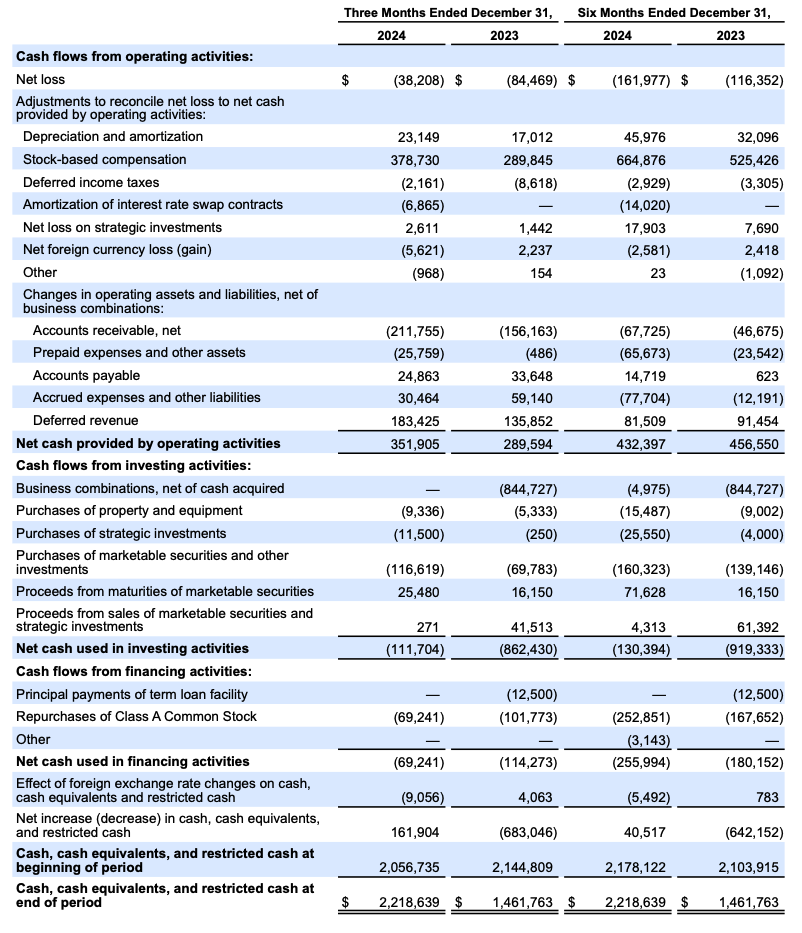

Condensed consolidated statements of cash flows

(U.S. $ in thousands)

(unaudited)

Reconciliation of GAAP to non-GAAP results

(U.S. $ and shares in thousands, except per share data)

(unaudited)

Reconciliation of GAAP to non-GAAP financial targets

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward-looking, including but not limited to risks and uncertainties related to statements about our platform, products, product features, System of Work, AI capabilities, enterprise sales, pricing, customers, Cloud and Data Center migrations, macroeconomic environment, anticipated growth, market potential, business plans and strategic priorities, partnerships, investments, outlook, technology, research and development, leadership transitions, FedRAMP authorization, and future announcements, and our financial targets such as total revenue, Cloud, Data Center, and Marketplace and other revenue and GAAP and non-GAAP financial measures including gross margin, operating margin, and share count.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the SEC) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 10-K and 10-Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

ABOUT NON-GAAP FINANCIAL MEASURES

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit, non-GAAP gross margin, non-GAAP operating income, non-GAAP operating margin, non-GAAP net income, non-GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled non-GAAP measures used by other companies, provide supplemental information regarding our operating performance on a non-GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

• Non-GAAP gross profit and Non-GAAP gross margin. Excludes expenses related to stock-based compensation, and amortization of acquired intangible assets.

• Non-GAAP operating income and non-GAAP operating margin. Excludes expenses related to stock-based compensation, and amortization of acquired intangible assets.

• Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, gain on a non-cash sale of a controlling interest of a subsidiary, and the related income tax adjustments.

• Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our software development, service management and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 300,000 companies of all sizes worldwide – including NASA, BMW, Kiva, Deutsche Bank and Dropbox – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira, Confluence and Jira Service Management at https://atlassian.com.

Investor relations contact: Martin Lam, IR@atlassian.com

Media contact: M-C Maple, press@atlassian.com

1 Gartner, Magic Quadrant for DevOps Platforms, Keith Mann, Thomas Murphy, Bill Holz, George Spafford, et al, 3 September 2024.

2 Gartner, Magic Quadrant for Marketing Work Management Platforms, Michael McCune, Lacretia Marsh, et al., 17 December 2024

Gartner does not endorse any vendor, product or service depicted in its research publications and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

The Gartner content described herein (the “Gartner Content”) represents research opinion or viewpoints published, as part of a syndicated subscription service, by Gartner, Inc. (“Gartner”), and is not a representation of fact. Gartner Content speaks as of its original publication date (and not as of the date of this Shareholder Letter), and the opinions expressed in the Gartner Content are subject to change without notice.

GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally, and MAGIC QUADRANT is a registered trademark of Gartner, Inc. and/or its affiliates and are used herein with permission. All rights reserved.

Forrester does not endorse any company, product, brand, or service included in its research publications and does not advise any person to select the products or services of any company or brand based on the ratings included in such publications. Information is based on the best available resources. Opinions reflect judgment at the time and are subject to change. For more information, read about Forrester’s objectivity here .