It’s been a milestone quarter for the Atlassian history books.

Today, Atlassian is a cloud-majority company. We have over 300,000 customers using our Cloud products and have seen a 3x increase in paid seats in the cloud since we announced the end-of-support for our Server products three and a half years ago. As we watched our dashboard tracking paid Server users reach zero, we reflected on how daunting this mountain appeared when we first drew up plans to sunset our Server offerings.

And while this milestone is just that – one significant moment amongst many across our multi-year journey – we are chuffed with our accomplishments. Overall, we migrated more paid seats to the cloud than we had initially projected, underscoring the innovation we’ve been shipping and our customers’ desire to make the switch. We’ve also consistently seen lower-than-expected churn from our Server base, which speaks to the mission-critical role our products play and value they deliver. As we look ahead, we have an even larger opportunity in the cloud than we had originally believed. We’ll continue to execute against our roadmap to pave the path for our Data Center customers to realize the innovation that can only be found in the Atlassian cloud.

However, this quarter will be marked by more than a momentous cloud milestone. After an incredible 23 years, Scott Farquhar has made the decision to step down as co-CEO. Scott’s last day as co-CEO will be August 31, 2024. He will remain active as a Board member and assume a special advisor role.

The contribution Scott has made in founding and building Atlassian is impossible to quantify, but can best be illustrated by the tens of thousands of jobs created, the hundreds of thousands of customers supported, and the millions of daily users around the world whose lives are improved by Atlassian’s software. Atlassian paved the way for other Australian technology companies and continues to do so today.

Scott steps away to spend more time with his young family, improve the world via philanthropy, and help further the technology industry globally. Rest assured, there will be many moments of thanks and celebration of the incredible impact Scott has made in the coming months.

Mike will continue to lead as CEO as Atlassian pursues its mission to unleash the potential of every team and capitalize on its strengths in the AI era.

Atlassian in the era of AI

Atlassian in the era of AI

By combining the transformative power of AI with our 20+ years of data and insights into how teams plan, track, and deliver work, we can increase the velocity at which teams move work forward. And because we lead with R&D (as opposed to marketing or pricing), we focus on shipping high-quality features that drive user adoption by delivering value from day one.

of note:

Last quarter, following the general availability (GA) announcement of Atlassian Intelligence, we said we’d be shipping new AI features at a healthy clip. In March we shipped the capability to create automation rules in Jira using natural language, powered by Atlassian Intelligence. With a simple description of what to automate, users can quickly create automation rules and let Atlassian Intelligence take care of the intricate process of formulating these rules.

We also continued to thread Atlassian Intelligence throughout Jira Service Management to help teams deliver exceptional employee support. By rolling out advancements to the Virtual Agent as well as AI-powered summaries and agent recommendations, we’re making it dead simple for 1) employees to self-serve and get help fast; and 2) support agents to provide help faster. In addition, the new AI-powered service desk configuration capabilities make it even easier for teams beyond IT (e.g., HR, facilities, legal) to configure service desks tailored to their needs.

We’re already seeing many of our customers benefit from the power of AI and virtual agent capabilities. FanDuel Group, a driving force in a multi-billion dollar gaming industry, cut tickets that require human intervention by 85%. Similarly, OVO Energy, a renewable energy leader with 4 million customers, is resolving 23% of all support requests in less than 5 seconds.

Atlassian Intelligence has helped our DevOps practices by reducing context-switching. We leveraged the virtual agent to create an AI-powered Developer Assistant to streamline support for developers in Slack; this means they can get help without having to leave their favorite tools. Alongside AI answers and issue summaries, harnessing Atlassian Intelligence to reduce distractions has led to a boost in our developer experience.

– Martin Brignall, Developer Tooling Specialist at OVO Energy

Our approach has translated to over 30,000 customers enabling Atlassian Intelligence, with monthly active users (MAU) increasing 3x since launching into GA in December 2023. And the early feedback we’re hearing demonstrates the value these customers are realizing. Weekly users of Atlassian Intelligence in Confluence tell us they’re saving over 45 minutes a week on average, and 77% of users report saving time using AI search functions.

This is just the tip of the iceberg when it comes to the customer impact we can make in the AI space. We have the talent, resources, and platform capabilities to harness the unique data and deep knowledge of teamwork we’ve built over years of helping millions of teams drive mission-critical work forward. We’re eagerly awaiting Team ‘24, where we’ll take the stage and unveil more ways in which we’ll unleash the potential of Atlassian customers through Atlassian Intelligence.

A consistent innovation drumbeat

A consistent innovation drumbeat

We had a busy Q3 shipping an array of innovations to support our customers.

Earlier this quarter, we delivered AI enhancements across Loom for better async video collaboration. Loom was subsequently named one of Fast Company’s Most Innovative Companies in the workplace category. This reinforces our belief that the rise of distributed work will mean async video increasingly becomes a communication mode of choice alongside text, presentations, and worksheets for the next generation of working professionals.

We’re already seeing this culture change play out, with more and more customers choosing to collaborate via Loom in order to reduce real-time meetings.

I prefer Loom for the organization capabilities in the platform and the AI summaries layered on top for the added gained efficiencies. Fifteen meetings [were] eliminated after switching to Loom in the second half of 2023.

– Caroline Hall Prettyman, Senior Manager, HubSpot Strategy, WebStrategies inc.

Turbocharged by new AI capabilities, 23 million videos have been enhanced via Loom AI, boosting viewer engagement by 18%. We’re excited to continue innovating in this space in order to help teams collaborate in richer, more human ways.

We also launched Confluence whiteboards into GA, a dynamic and interactive feature that facilitates ideation and collaboration, turning the in-person team whiteboarding experience into an effortless digital experience. We shipped recent enhancements like dark mode, as well as smart sections, which take the effort out of making updates to Jira issues after planning sessions.

With Confluence whiteboards, customers can avoid adding another tool to their organization, instead consolidating their collaboration tools to where their work is getting done – right in Confluence. One large technology customer is saving $60,000 a year by using Confluence whiteboards instead of competitor tools. To date, over 600,000 Confluence whiteboards have been created, capturing the beginning of millions of bright ideas.

Confluence whiteboards have helped Trust Bank collaborate more effectively across our teams, especially in the discovery and delivery phases of our product development. This has allowed us to visualize and align on development plans and key priorities, raise and identify risks and blockers early, and track progress on key items at a glance.

– Stewart Gray, Agile Coach, Trust Bank

We also are excited to announce we’ve acquired Optic, an API documentation and management tool that makes it easy for developers to publish accurate API documents, avoid breaking changes, and improve the design of their APIs. Adding Optic to Compass will accelerate our ability to empower engineering teams and improve productivity by helping developers find the documentation they need and ship faster. Customers will be better able to keep accurate, useful, and relevant API documentation to improve how they build and operate software.

While our product suite serves customers’ core needs around aligning, planning, and sharing work, our Marketplace extends the product’s capabilities to cover specialized use cases. In Q3, the Atlassian Marketplace surpassed $4 billion in lifetime sales. More than 1,800 Marketplace partners have built more than 5,700 apps and integrations, delivering even more value and innovation to our customers. This is a testament to our philosophy of having an open, extensible, yet flexible foundation.

A landmark quarter for our cloud future

A landmark quarter for our cloud future

We’re proud as punch to showcase our cloud progress to date.

When we announced we’d be sunsetting Server products three and a half years ago, we knew this change would require a big transition for us and for our on-premises customers. But we also knew that it would accelerate our progress in driving the future of teamwork. At the same time, we’ve always maintained cloud migrations would be a multi-year journey and Server’s end-of-support (EOS) would be one milestone on that journey.

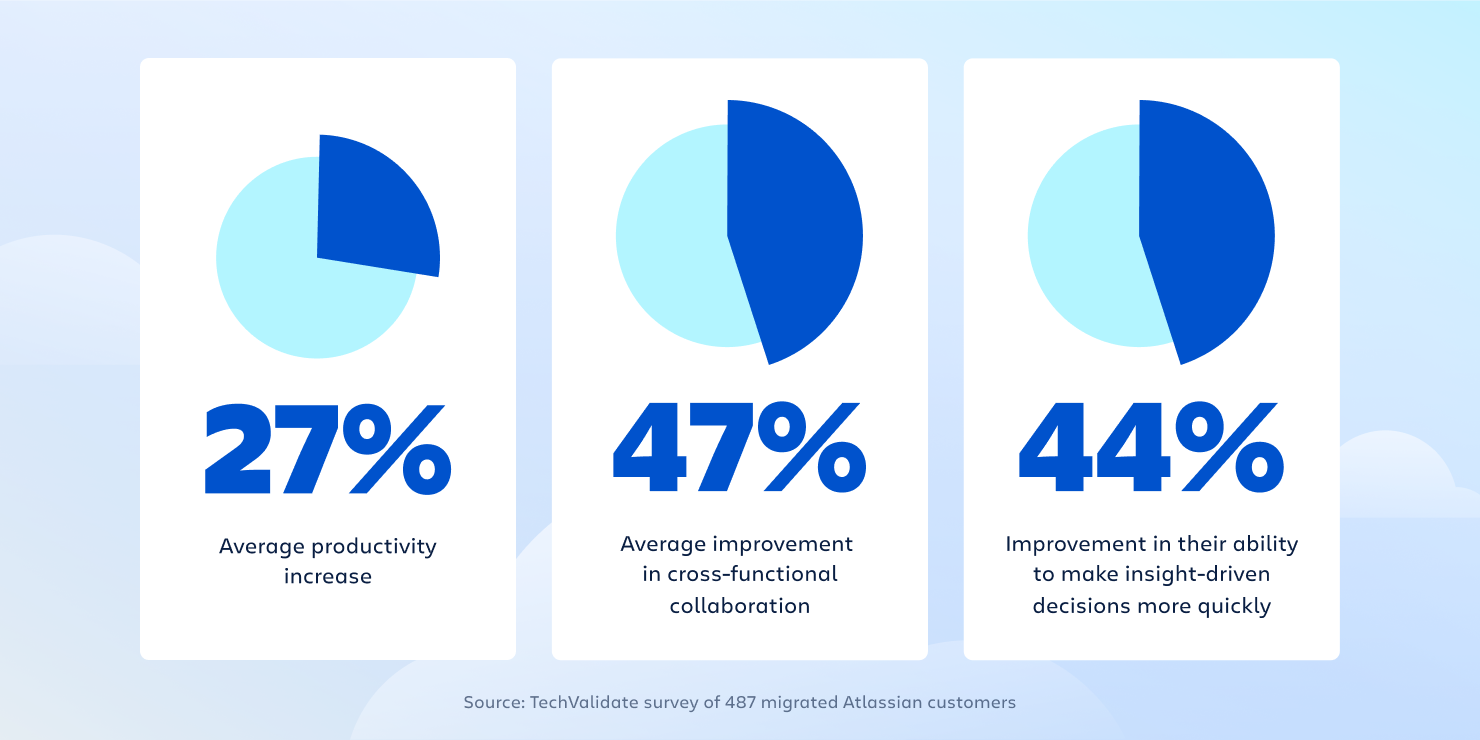

Today, the Atlassian cloud is powering more than 300,000 customers like NASA, Reddit, Rivian, Domino’s Pizza Enterprises Ltd, and Paypal. Our customers now have more paid seats in Cloud products than in on-premises deployments. In fact, 94% of customers who use Jira Software, Confluence, and/or Jira Service Management have a presence in the cloud. What’s more, after migrating to Cloud, our customers are telling us they’re experiencing greater productivity and collaboration:

The program to sunset our Server products has been an overall success. We beat our original expectations in both the number of paid seats migrated to Cloud and in customer churn. These numbers reflect the immense effort of teams right across Atlassian. What’s even more exciting is that we have an even bigger opportunity than we originally believed, as Data Center customers migrate to Cloud in the coming years.

Data Center has proven to be a stepping stone for our customers to ultimately get to the cloud. We’ve already seen strong Data Center to Cloud migration success, and that progress has been building each year. This reflects the deep relationships we’ve built with our largest customers, the significant advancements we’ve made in building enterprise capabilities and innovation, and the strong desire from customers to move to Cloud.

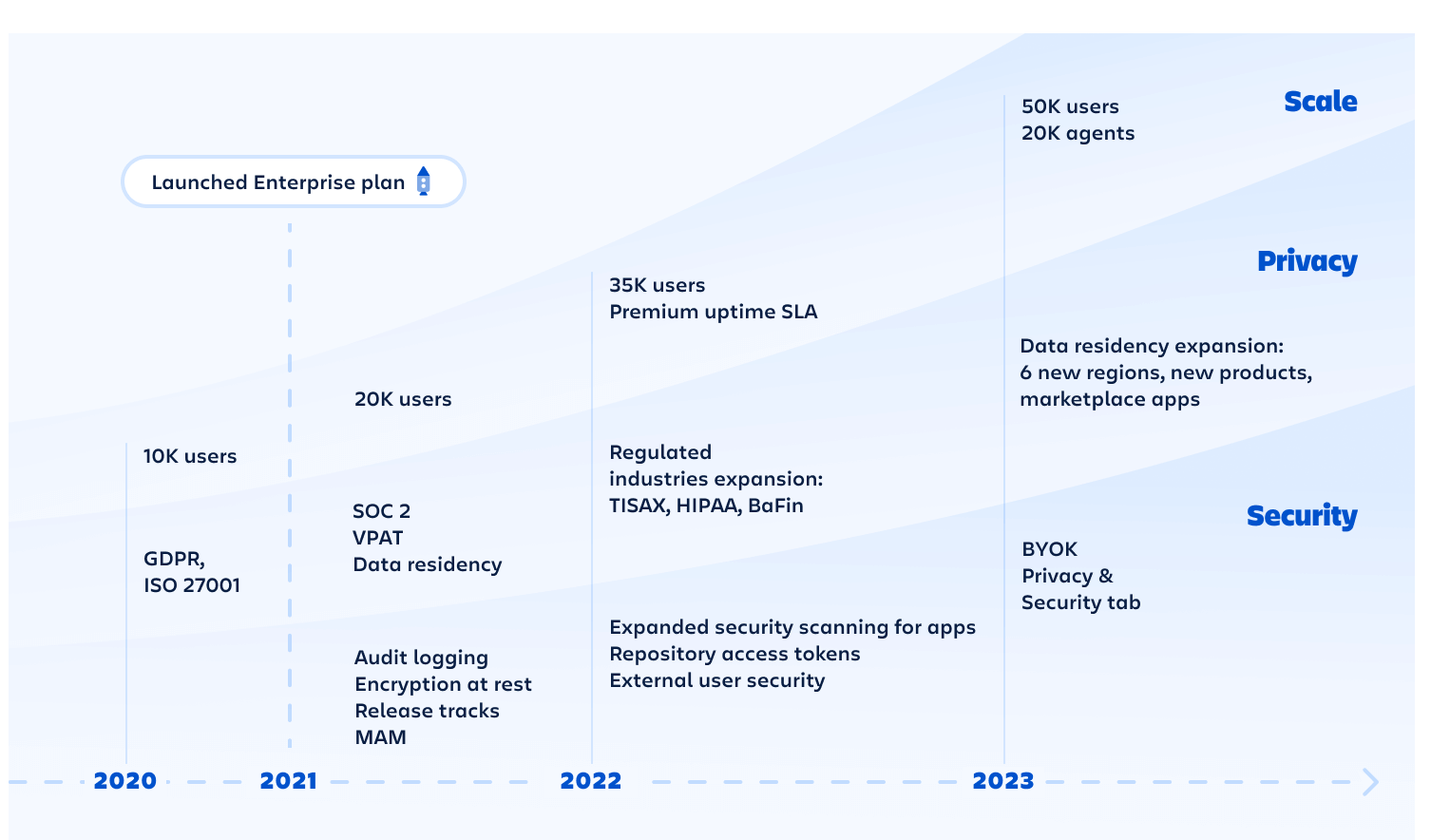

In order to pave the way for our Data Center customers, we’ve been laser-focused on advancing our enterprise-grade cloud platform. We’ve been consistently increasing the scale of our Cloud products, meeting critical regulatory compliance standards, and enhancing data governance.

Steady delivery on our cloud roadmap

Each quarter, we’ve shipped new capabilities, and we’ve seen customers from highly regulated industries make the move to Cloud thereafter. A few examples:

- Healthcare: Castlight and CHC Healthcare

- Financial Services: EMC Insurance, EQ Bank and Finoa

- Government: UK Driver & Vehicle Licensing Agency

- Highly regulated regions: The European Union, where customers like Software AG and Voith reside.

And on the heels of announcing our Canada data residency option last quarter, we added multiple new regions in Q3 that will unlock Cloud for even more customers including the United Kingdom, Japan, Switzerland, India, and South Korea.

Once customers experience Cloud, the value is clear. With the additions of platform features like automation, Atlassian Analytics, and Atlassian Intelligence, customers are getting more bang for their buck, and their teams are able to work faster and smarter, together.

As our largest customers migrate from Data Center to Cloud, we’ve had the opportunity to engage more deeply, build strategic relationships, and open the door to conversations with customers who want to do more with us. That might be consolidating tools onto the Atlasian platform, adding more products to address their challenges, or upgrading to higher-level editions to take advantage of more advanced capabilities.

One such success story is the State of Utah, a customer whose vision is to be a technology leader that delivers value and simplifies the lives of Utah residents.

The state of Utah

Several teams across the state government were already using Atlassian tools, including Trello, Jira Software, Bitbucket, Confluence, and Atlassian Access. Trello had become particularly popular as an intuitive project management tool that anyone could learn fast. As it spread quickly and organically, the IT team utilized Atlassian Access and reinforced to leadership the need for a more centralized, secure, cloud-based ecosystem.

IT was able to convince leadership to migrate and consolidate on Atlassian’s cloud platform. Not only would they save money, but it would also reduce the IT team’s pain points, allowing them to be more strategic by giving them just one platform to manage.

Today, the State of Utah relies on an integrated ecosystem of Enterprise edition tools to serve its constituents:

- Jira Software for continuous integration and continuous delivery (CI/CD)

- Bitbucket for securely storing code

- Trello for non-technical project management

- Confluence for knowledge management

- Atlassian Access for single sign-on and enterprise-grade identity management

The State of Utah has been able to unlock efficiency and effectiveness in the cloud to transform the way they work. Prior to Jira, they were using 14 different project management systems. But a move to Jira Cloud meant a speed up provisioning, improved collaboration and project management, and more transparency into projects across the State of Utah.

This example is not an uncommon one. As we work with Data Center customers on their journey to Cloud, these conversations are happening more frequently. Atlassian is heads-down and focused on execution so we can help customers realize their full potential, which will ultimately be unleashed in the cloud.

More to come at Team ’24

We’re excited to be hosting our flagship user event, Team ’24, in Las Vegas next week. This will be a three-day live event, April 30 – May 2, where we unveil plenty of new product features, along with breakout sessions, interactive labs, hands-on training, and networking opportunities for our customers.

We’ll also be holding our Investor Day at Team ’24 on May 1st, with a live stream option for those who can’t make it to Vegas. We hope to see you there!

– Mike and Scott

Financial Highlights

Strong migrations and enterprise sales execution drove revenue, gross profit, and operating income ahead of our expectations.

We delivered record billings and surpassed $1 billion in subscription revenue driven by growth in our Cloud and Data Center businesses. Strong customer retention drove record migrations as we ended support for our Server offerings, resulting in better-than-expected Data Center and Marketplace revenue. Gross profit and operating income benefited from revenue outperformance and disciplined cost management.

We continue to execute well against our long-term objectives of consistently delivering differentiated value and innovation to customers, making meaningful progress on our cloud roadmap, and building new capabilities to better serve enterprise customers. The strong migrations to Data Center this quarter demonstrate not only customer commitment to the Atlassian platform but also the significant opportunity we have to deliver sustained, long-term Cloud revenue growth in the future.

Highlights for Q3’24 include:

All growth comparisons below relate to the corresponding period of last year, unless otherwise noted.

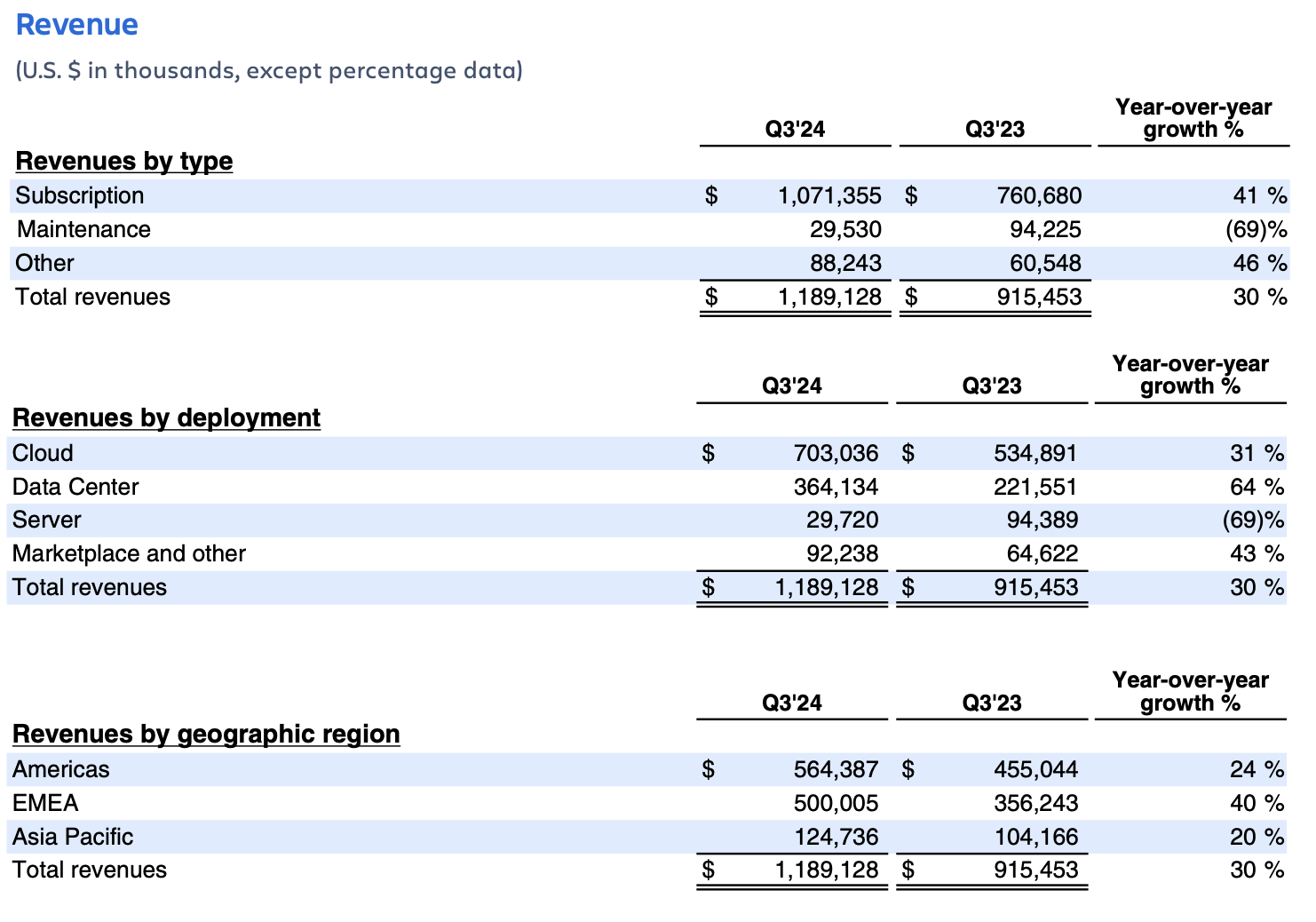

- Revenue of $1,189 million increased 30%, driven by growth in our Cloud and Data Center offerings.

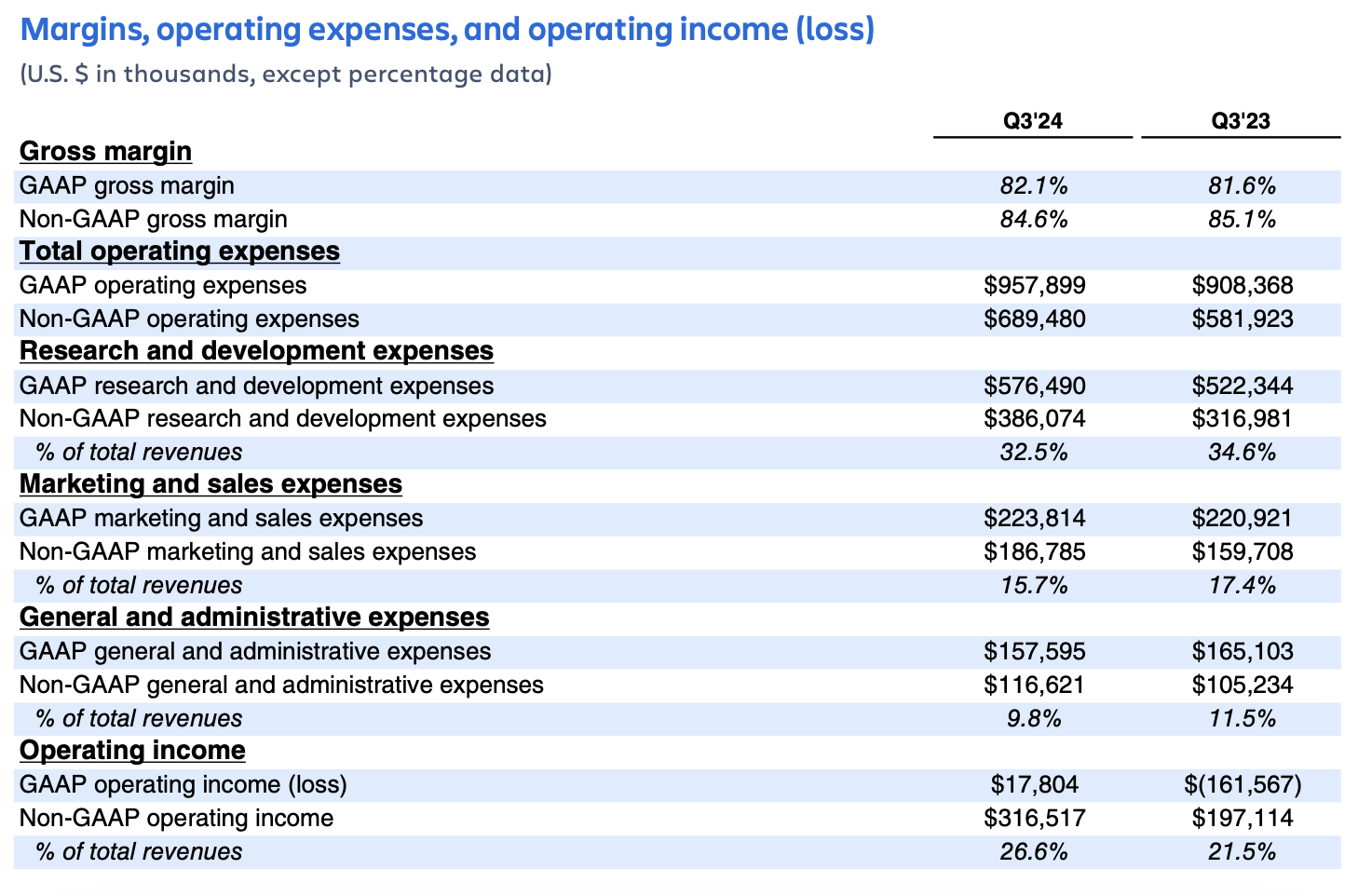

- GAAP gross margin of 82% and non-GAAP gross margin of 85% were flat.

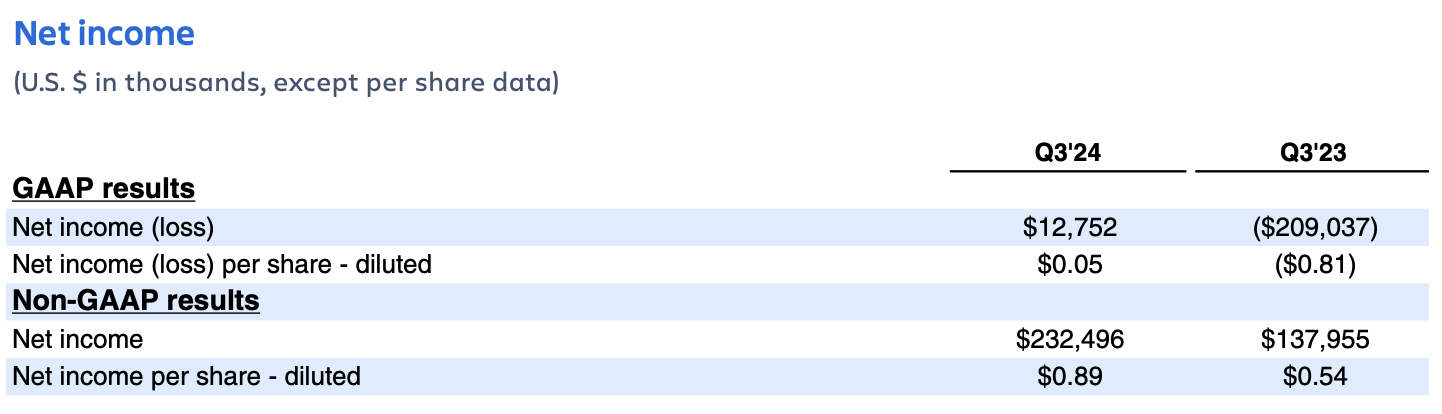

- GAAP operating income was $18 million and GAAP operating margin of 1% increased approximately 19 percentage points. Non-GAAP operating income was $317 million and non-GAAP operating margin of 27% increased approximately 5 percentage points driven by greater operating leverage.

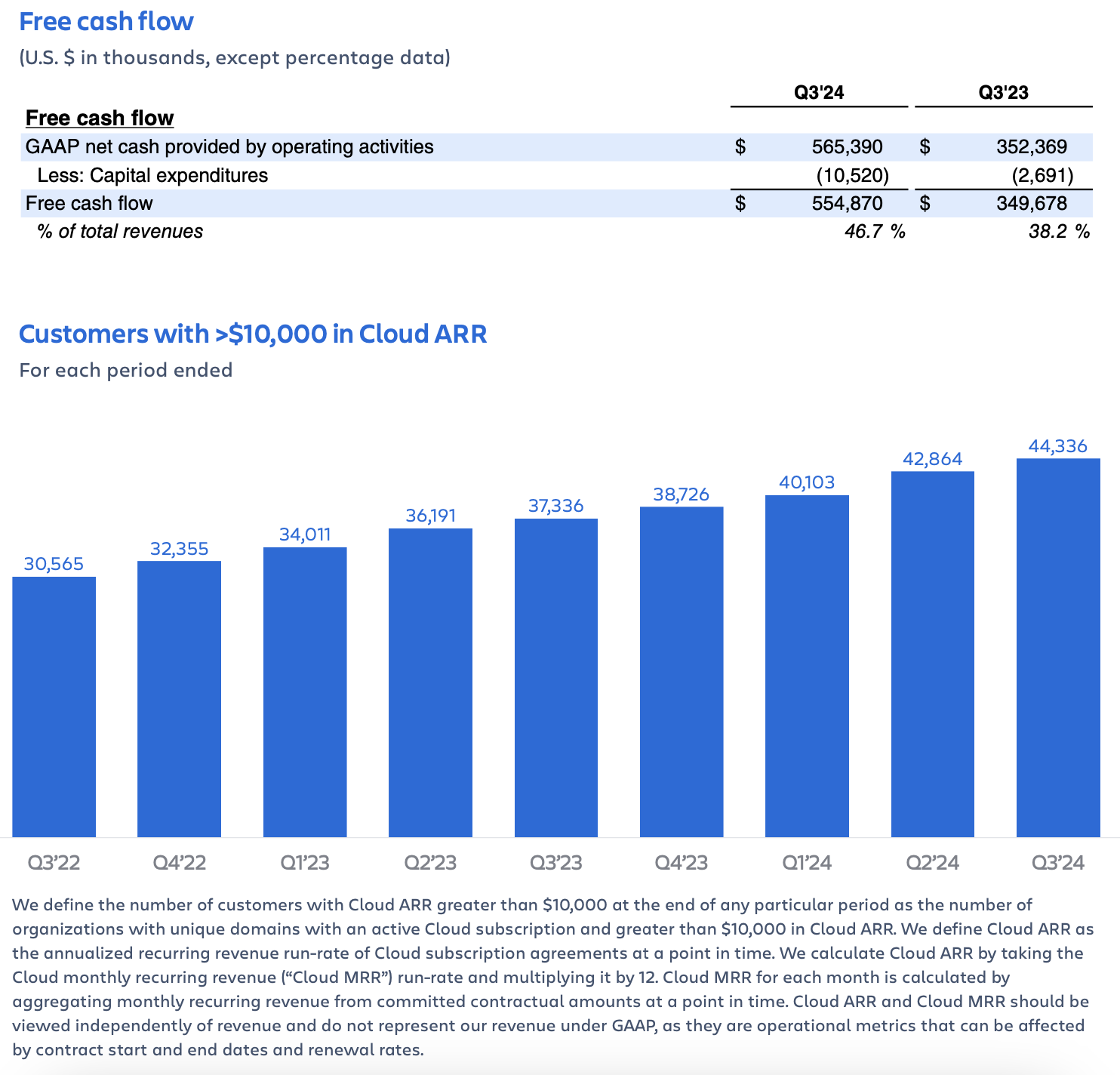

- Operating cash flow of $565 million increased 60% driven primarily by strong collections on record billings. Free cash flow of $555 million increased 59%.

Revenue growth in Q3 was driven by subscription revenue, which grew 41%.

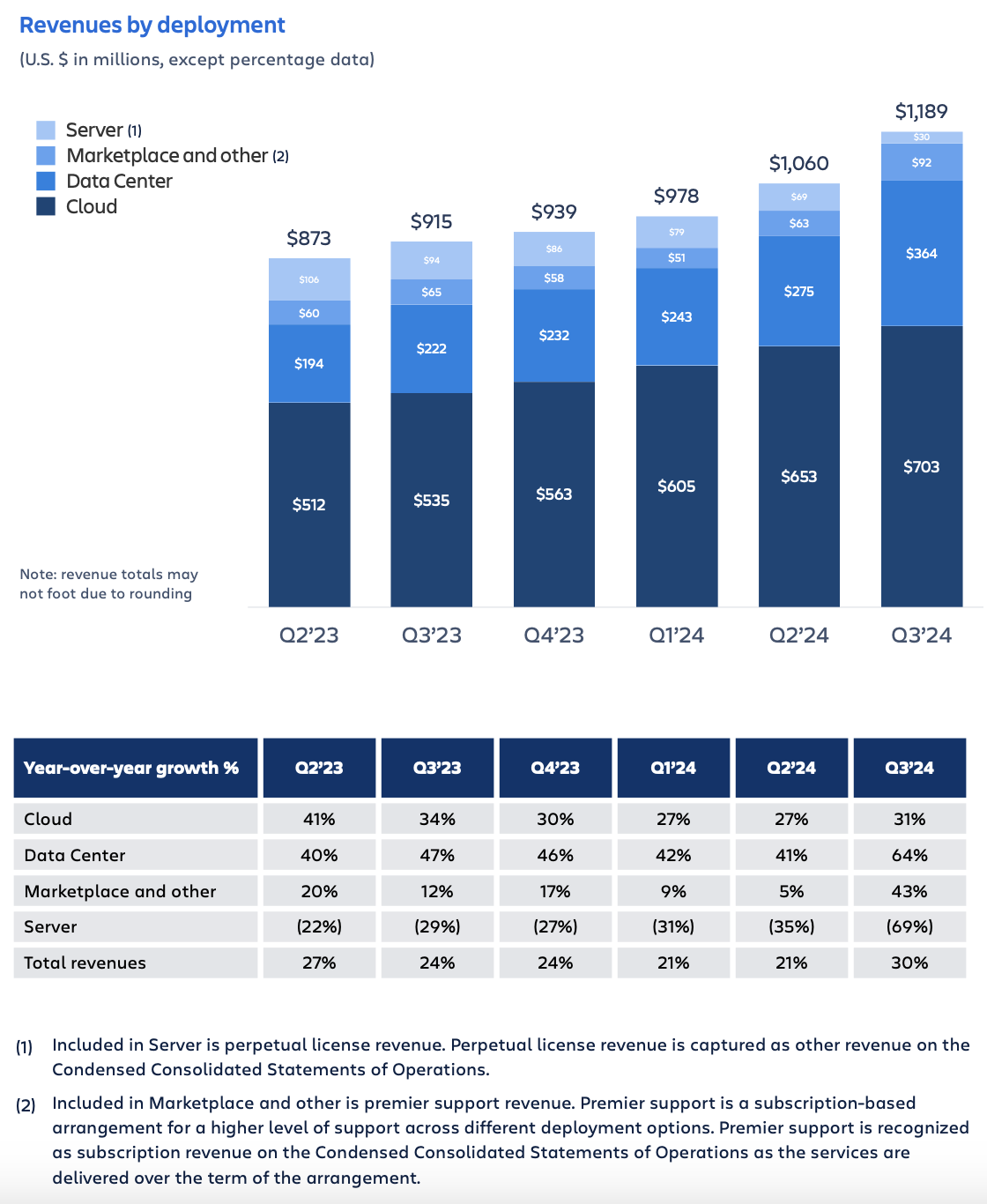

Cloud revenue growth was in line with our expectations and grew 31% driven by paid seat expansion in existing customers, migrations from both Server and Data Center, and cross-sell of additional products. Prior quarter trends on the primary revenue growth drivers persisted in Q3, consistent with our expectations. Paid seat expansion remains challenged, with continued softness in SMB offset by relative strength in our enterprise customer segment. Trends around migrations, cross-sell of additional products, adoption of higher-value editions, and customer retention remained stable.

Data Center revenue growth of 64% significantly exceeded our expectations driven by record migrations from Server, as well as strong expansion from existing customers. The impact of Server to Data Center migrations, net the impact from Data Center to Cloud migrations, benefited Data Center growth by approximately 36 points. The outperformance in migrations was driven by better-than-expected customer retention following the end-of-support for our Server offerings in February, underscoring the high-value nature of our products. As expected, most of those customers migrated to Data Center. Revenue growth also benefited from customers purchasing additional seats ahead of price changes implemented during the quarter. The contribution to Data Center revenue growth from the outperformance on migrations and customer purchasing in front of the price change was approximately 19 points and 8 points, respectively.

Marketplace and other revenue growth of 43% also significantly exceeded our expectations, driven by customer purchasing of third-party apps in our Marketplace in conjunction with their Data Center subscriptions. This event-driven purchasing drove approximately 32 points of Marketplace and other revenue growth. As a reminder, revenue from sales of Marketplace apps is recognized in full at the time of sale.

From a regional perspective, the outperformance in Data Center and related Marketplace app sales were primarily driven by partners in EMEA.

Lastly, deferred revenue increased 40% year-over-year to $2.0 billion driven by continued growth in annual and multi-year agreements, which reflects increasing customer commitment to the Atlassian platform and roadmap.

GAAP operating expenses increased 5% year-over-year driven by higher employment costs, including bonus and stock-based compensation expenses. As a reminder, we incurred $98 million of restructuring charges in Q3’23. Headcount at the end of Q3’24 was 11,902, an increase of 479 from Q2’24 driven primarily by hiring in R&D and sales to drive key strategic priorities such as cloud migrations, serving enterprise customers, delivering innovative customer value across our product portfolio, and AI.

Non-GAAP operating expenses increased 18% year-over-year and were slightly lower than expected driven by savings in discretionary spending.

GAAP operating margin of 1% and non-GAAP operating margin of 27% benefited year-over-year from increased operating leverage. The outperformance on Data Center and Marketplace revenue in the quarter benefited GAAP and non-GAAP operating margins by over 5 points.

Total Revenue

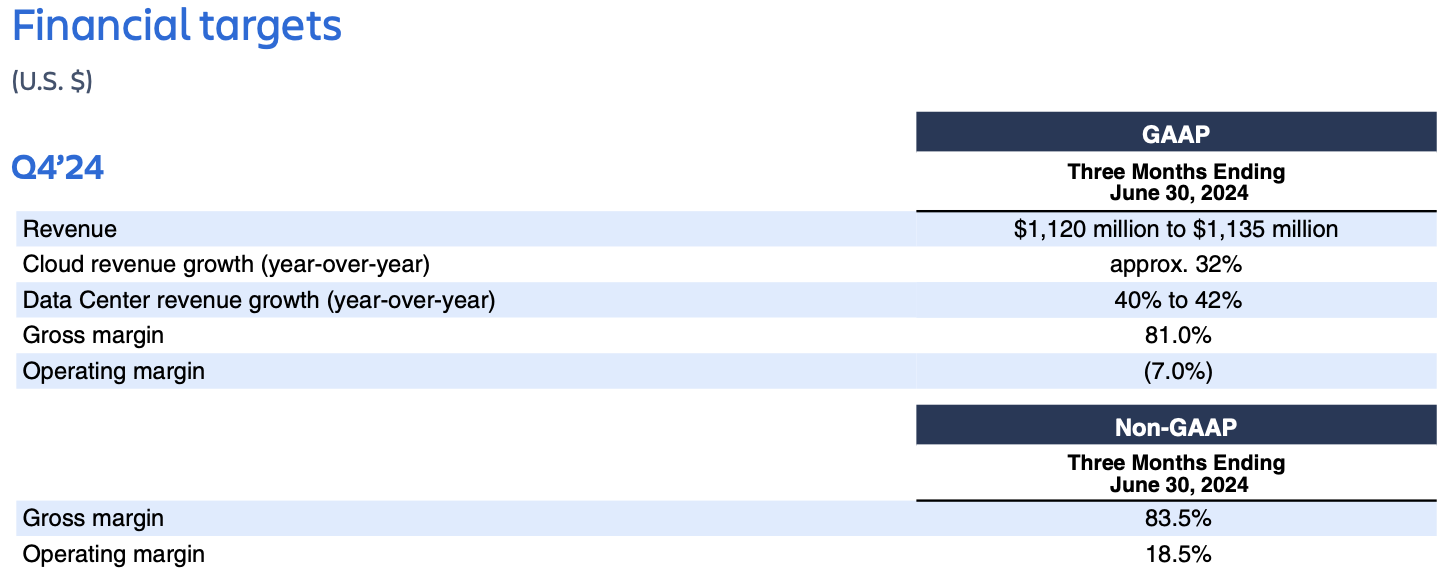

For Q4’24, we expect total company revenue to be in the range of $1,120 million to $1,135 million. This guidance implies full year FY24 revenue growth of approximately 23% and assumes neither improvement nor deterioration in macroeconomic conditions. Further detail and expected trends are provided below:

SUBSCRIPTION REVENUE

Cloud revenue

We expect Q4’24 Cloud revenue growth of approximately 32% year-over-year, of which migrations will drive approximately 10 points. Our guidance assumes current trends across all core growth drivers persist into Q4 and that the rate of paid seat expansion in our SMB customer segment will remain challenged.

Data Center revenue

We expect Q4’24 Data Center revenue growth to be in the range of 40% to 42% year-over-year. Our guidance assumes revenue recognition from the outperformance on Q3 billings (a benefit of approximately 15 points to Data Center revenue growth in Q4), limited migrations from Server post end-of-support, and continued migrations to Cloud enabled by delivery of enterprise-grade platform capabilities and value.

MAINTENANCE REVENUE

We will no longer recognize Server revenue and therefore expect Server revenue to be zero in Q4’24.

OTHER REVENUE

We expect Other revenue, which is primarily comprised of Marketplace revenue, to be roughly flat year-over-year in Q4’24, driven by continued sales mix shift to Cloud apps.

As a reminder, there is a lower Marketplace take rate on third-party Cloud apps relative to Data Center apps to incentivize further Cloud app development.

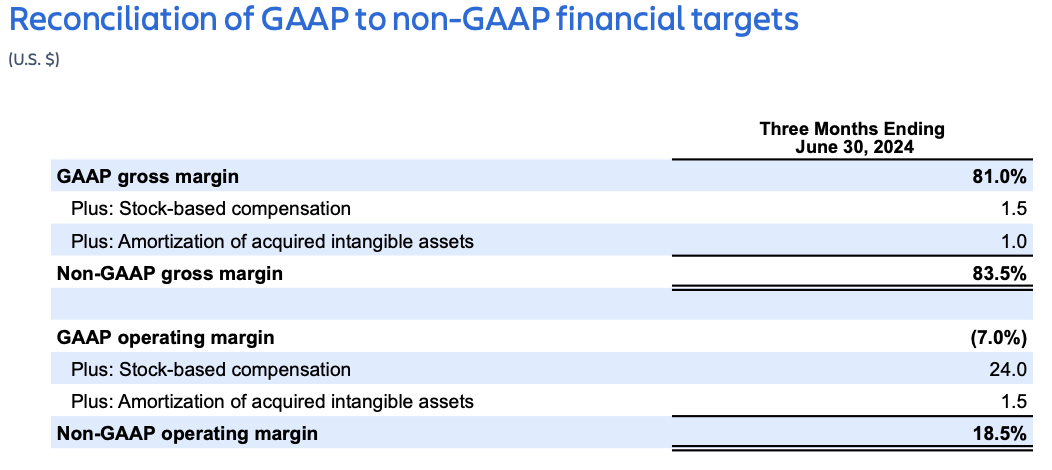

Gross margin

We expect GAAP gross margin to be approximately 81.0% and non-GAAP gross margin to be approximately 83.5% in Q4’24. Our guidance assumes gross margins continue to decrease year-over-year driven by revenue mix shift to Cloud.

Operating margin

We expect GAAP operating margin to be approximately (7.0%) and non-GAAP operating margin to be approximately 18.5% in Q4’24. Operating expense growth will be driven by our continued investments in key strategic priorities to deliver long-term growth. Additionally, our flagship user conference, Team ’24, takes place in Q4, which drives quarter-to-quarter seasonality in operating expenses.

SHARE COUNT

We continue to expect diluted share count to increase by less than 2% in FY24.

FORWARD-LOOKING STATEMENTS

This shareholder letter contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, which statements involve substantial risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intend,” “could,” “should,” “estimate,” or “continue,” and similar expressions or variations, but these words are not the exclusive means for identifying such statements. All statements other than statements of historical fact could be deemed forward-looking, including risks and uncertainties related to statements about our products, product features, including AI capabilities, customers, Atlassian Platform, Atlassian Marketplace, Cloud and Data Center migrations, macroeconomic environment, anticipated growth, outlook, technology, potential benefits and synergies from Loom and other acquisitions, our Team Anywhere program, hiring capabilities, and other key strategic areas, and our financial targets such as total revenue, Cloud and Data Denter revenue and GAAP and non-GAAP financial measures including gross margin and operating margin.

We undertake no obligation to update any forward-looking statements made in this shareholder letter to reflect events or circumstances after the date of this shareholder letter or to reflect new information or the occurrence of unanticipated events, except as required by law.

The achievement or success of the matters covered by such forward-looking statements involves known and unknown risks, uncertainties and assumptions. If any such risks or uncertainties materialize or if any of the assumptions prove incorrect, our results could differ materially from the results expressed or implied by the forward-looking statements we make. You should not rely upon forward-looking statements as predictions of future events. Forward-looking statements represent our management’s beliefs and assumptions only as of the date such statements are made.

Further information on these and other factors that could affect our financial results is included in filings we make with the Securities and Exchange Commission (the “SEC”) from time to time, including the section titled “Risk Factors” in our most recently filed Forms 10-K and 10-Q. These documents are available on the SEC Filings section of the Investor Relations section of our website at: https://investors.atlassian.com.

ABOUT NON-GAAP FINANCIAL MEASURES

In addition to the measures presented in our condensed consolidated financial statements, we regularly review other measures that are not presented in accordance with GAAP, defined as non-GAAP financial measures by the SEC, to evaluate our business, measure our performance, identify trends, prepare financial forecasts and make strategic decisions. The key measures we consider are non-GAAP gross profit and non-GAAP gross margin, non-GAAP operating income and non-GAAP operating margin, non-GAAP net income, non-GAAP net income per diluted share and free cash flow (collectively, the “Non-GAAP Financial Measures”). These Non-GAAP Financial Measures, which may be different from similarly titled nonGAAP measures used by other companies, provide supplemental information regarding our operating performance on a non-GAAP basis that excludes certain gains, losses and charges of a non-cash nature or that occur relatively infrequently and/or that management considers to be unrelated to our core operations. Management believes that tracking and presenting these Non-GAAP Financial Measures provides management, our board of directors, investors and the analyst community with the ability to better evaluate matters such as: our ongoing core operations, including comparisons between periods and against other companies in our industry; our ability to generate cash to service our debt and fund our operations; and the underlying business trends that are affecting our performance.

Our Non-GAAP Financial Measures include:

• Non-GAAP gross profit and Non-GAAP gross margin. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, and restructuring charges.

• Non-GAAP operating income and non-GAAP operating margin. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, and restructuring charges.

• Non-GAAP net income and non-GAAP net income per diluted share. Excludes expenses related to stock-based compensation, amortization of acquired intangible assets, restructuring charges, gain on a non-cash sale of a controlling interest of a subsidiary, and the related income tax adjustments.

• Free cash flow. Free cash flow is defined as net cash provided by operating activities less capital expenditures, which consists of purchases of property and equipment.

We understand that although these Non-GAAP Financial Measures are frequently used by investors and the analyst community in their evaluation of our financial performance, these measures have limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. We compensate for such limitations by reconciling these Non-GAAP Financial Measures to the most comparable GAAP financial measures. We encourage you to review the tables in this shareholder letter titled “Reconciliation of GAAP to Non-GAAP Results” and “Reconciliation of GAAP to Non-GAAP Financial Targets” that present such reconciliations.

ABOUT ATLASSIAN

Atlassian unleashes the potential of every team. Our agile & DevOps, IT service management and work management software helps teams organize, discuss, and complete shared work. The majority of the Fortune 500 and over 300,000 companies of all size worldwide – including NASA, Audi, Kiva, Deutsche Bank and Dropbox – rely on our solutions to help their teams work better together and deliver quality results on time. Learn more about our products, including Jira Software, Confluence and Jira Service Management at atlassian.com.

Investor relations contact: Martin Lam, IR@aforman

Media contact: M-C Maple, press@atlassian.com